Here are the latest developments in global markets:

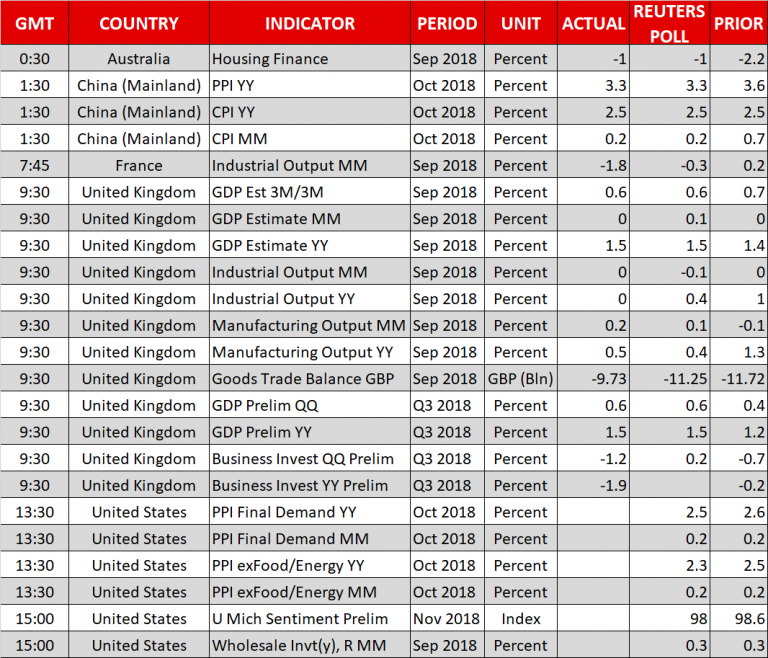

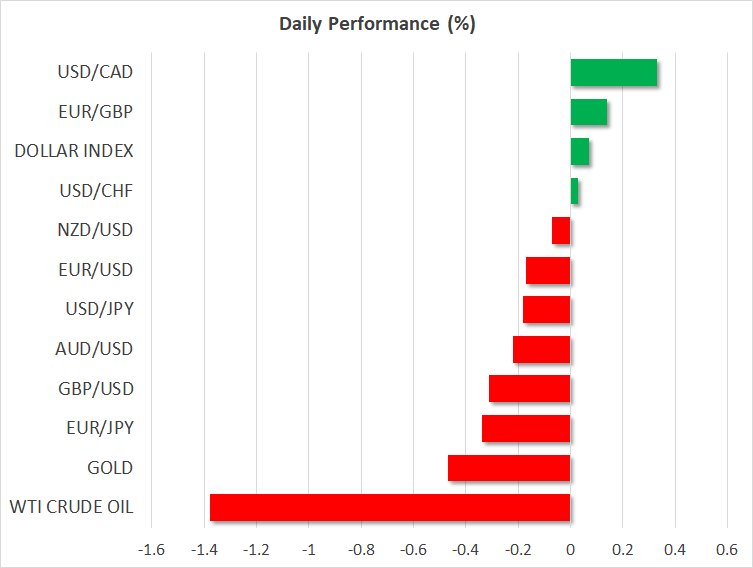

- FOREX: The British economy expanded by 1.5% y/y in the third quarter as expected, preliminary data showed. The UK’s trade deficit narrowed, and the manufacturing output was slightly better than forecast in September. However, the evidence on business investment was disappointing and today’s discouraging Brexit headlines were enough to push pound/dollar straight down to 1.2988 before a reversal to 1.3035 (-0.15%). Particularly, capital expenditures decreased by 1.2% q/q in Q3 compared to a 0.2% expected rise, printing the biggest loss since Q1 2016. On the Brexit front, the DUP’s Brexit Spokesman, Sammy Wilson, reacted harshly to the British PM’s detailed Brexit letter after May seemed to back a different regulation for Northern Ireland than for the rest of the UK under the backstop clause. Wilson threatened to vote down the exit plans in the House of Commons if the proposals remain on the table. Pound/yen retreated by 0.53%, while euro/pound was in positive territory, gaining 0.20%. Meanwhile in the eurozone, concerns over the EU-Italian budget dispute scaled up following the European Commission’s forecasts on the Italian economy, which appeared more pessimistic than Rome’s predictions yesterday, particularly on the size of the public deficit. US tariff threats on EU cars seem to remain alive according to the EU Trade Commissioner, who argued that the US shows little willingness to strike a deal with the EU on the matter. Euro/dollar extended Thursday’s downside to 1.1325 before inched up to 1.1347(-0.11%), to the lowest since November 1. The dollar index was trading flat at 96.78 and dollar/yen slipped to 113.84 (-0.18%) after the Fed kept interest rates steady as expected and remained on course for further monetary tightening. Yet policymakers acknowledged the weakness in business investment, with markets seeing the US-Sino trade war responsible for the shortfall, especially after Moody’s reported on Thursday that the tensions between the sides could fire up in 2019 and global growth may slow in the next two years. Dollar/loonie rallied as high as 1.3197, a level never seen since early September, on the back of tumbling oil prices.

- STOCKS: European stocks followed US and Asian stocks lower on Friday, perhaps weighed by the Fed’s cautious statement on US business investment. The pan-European STOXX 600 and the Euro STOXX 50 were down by 0.55% at 1040 GMT. The German DAX 30 fell by 0.47%, the French CAC 40 declined by 0.80% and the UK’s FTSE 100 retreated by 0.57%. The Italian FTSE MIB was the worst performer, losing 1.20%. Futures tracking the S&P 500, Dow Jones and Nasdaq 100 were flashing red, pointing to a negative open.

- COMMODITIES: Crude prices turned increasingly bearish on Friday as concerns about supply build-ups and a slowing global economy weighed on market sentiment. WTI crude and Brent were heading for the fifth negative weekly close, with the former bridging below $60/barrel to touch a nine-month low at $59.28 (-1.94%) and the latter breaking support at $70 to register 7-month lows at $69.13 (-1.66%). In precious metals, gold remained on the downside, extending losses towards $1219 (-0.32%).

Day ahead: US PPI figures eyed; flash University of Michigan Consumer Confidence Index in focus

In the remainder of the day, the calendar will feature producer prices and wholesale inventories out of the US, while the University of Michigan will deliver initial estimates on the US consumer sentiment.

At 1330 GMT, the US Producer Price Index, another gauge for inflation, is expected to show that the price of overall goods sold by manufacturers has risen by 2.5% y/y in October, slightly less than in September when the gauge showed a growth of 2.6%. In the absence of food and energy, the core PPI is anticipated to ease to 2.3% y/y from 2.5% giving an early sign that inflation pressures might have stalled for the third month before the CPI figures, a more popular inflation measure, come into view next week.

At 1500 GMT, growth in wholesale inventories is said to have expanded by 0.3% on a monthly basis in September, the same as in August, while separately, the preliminary University of Michigan Consumer Sentiment Index is projected to have declined for the third month in November. Particularly, the index is seen lower by 0.6 points at 98 and still below the 8-year high of 102 reached in March. The survey’s sub-indexes measuring inflation expectations have proved market-moving in the past and will thus also be attracting attention. Should the numbers prove that confidence among consumers has lessened by more than analysts think, then the dollar could see selling interest today. Yet with the Fed pledging additional rate hikes in the near future, bearish movements could be curbed.

In energy markets, oil prices might move in the wake of the Baker Hughes oil rigcount at 1800 GMT.

As for scheduled public appearances today, Bank of England chief economist Andy Haldane will be speaking at 1830 GMT. Earlier in the US, New York Fed President, John Williams (permanent voting FOMC member) and the Philadelphia Fed President, Patrick Harker (non-voter) will be commenting at the America’s Workforce Book launch at 1330 GMT and 1345 GMT respectively. Meanwhile, at 1405 GMT, the Fed Vice Chair for Supervision, Randal Quarles (permanent voter) will be speaking on Stress Testing in Washington.

Brexit, trade and the Italian budget story may continue to feed risk-off sentiment during the day.