An upside surprise but inflation remains well contained

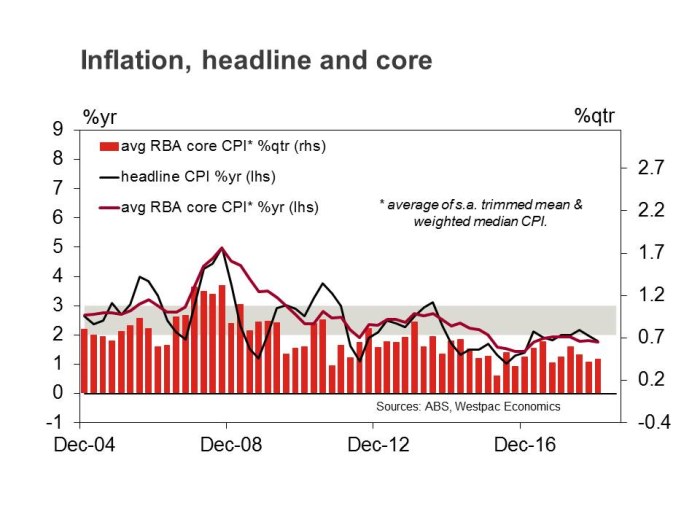

The December Quarter CPI printed 0.5%qtr, compared to the market median of 0.4% and Westpac’s forecast for 0.3%. At two decimal places, the rise in the CPI was 0.53%qtr, so a hard 0.5%. With base effects, the annual rate has eased back to 1.8%yr compared to 1.9%yr in Q3, 2.1%yr in Q2 and 1.9% in Q1. But with another sub 0.6% print, the six month annualised pace is down to 1.2%yr (using seasonally adjusted data – raw CPI six month annualised is 2.0%yr but this incorporates a seasonally stronger pace in H2). Inflation continues to bump along just at, or just under, the bottom of the RBA’s target band.

Following the December quarter 2017 CPI, we argued that searching for inflation in the Australian economy has been as fruitless as Vladimir and Estragon’s wait for Godot. While this report does suggest we have at least found a bottom in the disinflationary pulse, it is still too early to call an inflationary pulse is underway and there are some hints in the December 2018 report that the current scenario has much longer to run.

The average of the core measures, which are seasonally adjusted and exclude extreme moves, rose 0.4%qtr meeting market expectations. In the quarter, the trimmed mean gained 0.43% while the weighted median lifted 0.36%. The annual pace of the average of the core measures printed 1.8%yr which is the same as the September quarter print.

Incorporating revisions, the six month annualised growth in core inflation is 1.8%yr which is well below the bottom of the RBA target band and the slowest pace June 2016.

A small number of upside surprises but nothing that changes the fundamental picture

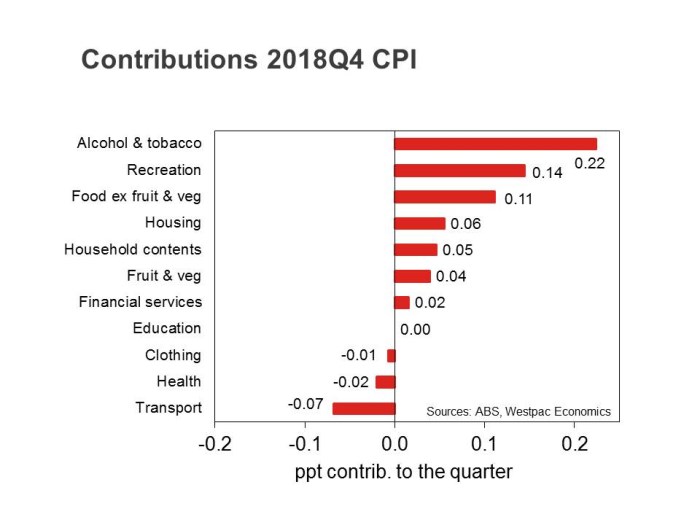

Some standouts in the quarter – on the positive side there was a stronger rise in alcohol & tobacco (3.2% vs 2.8% expected), a surprising rise in utilities (0.1% vs –0.3% expected), a smaller fall in auto fuel (–2.5 vs –4.2% expected), a surprising jump in household contents & services (0.5% vs –0.5% expected) and a stronger bump in holiday travel (2.6% vs 1.6% expected all due to strong domestic holiday prices). On the downside, food rose just 0.9% (1.2% expected) due to a smaller than expected rise in fresh fruit & vegetables, clothing & footwear fell –0.2% (a small rise was expected). Everything else came in close to expectations or just slightly stronger.

We think is worth noting the continued modest gains for housing expenditure. Housing costs overall rose as expected (0.2%) rents rose 0.2% (we thought they would be flat), dwelling prices rose just 0.4% (as we expected) while utilities rose 0.1% vs our –0.3% expected. The surprise in utilities was the jump in electricity prices that outweighed the normal seasonal fall in gas prices.

There remains a number of near term negative risks for both rents and dwelling purchase costs in NSW and Victoria. Given that rents and dwelling purchases are worth around 15% of the CPI on their own, this is significant for headline inflation, and even more so for core, where their weight is somewhat higher.

Tradables fell 0.3% in the December quarter. The tradable goods component fell –0.1% due to automotive fuel (-2.5%), audio, visual & comp equipment (-3.3%) and wine (-1.9%). The tradable services component fell 0.7% due to international holiday travel & accommodation (-0.8%).

Non-tradables component rose 0.9% in the December quarter. The non-tradable goods component rose 1.5%, due to the excise tax increase for tobacco (9.4%). The non-tradable services component rose 0.6%, due to domestic holiday travel & accommodation (6.2%).

Low inflation remains embedded in the economy

For the first time in two years inflation forecasters have underestimated the quarterly rise in the CPI. Does this signal a turnaround and the return of a more sustainable inflationary pulse? We don’t think so. While there are some isolated inflationary pressures; tobacco prices are clear standouts as well as embryonic indicators that the disinflationary pulse in retail, particularly in the household goods & services and domestic holidays & travel, may be ending. But, we are still seeing weakness in clothing and footwear while the moderation in housing costs (rents and dwelling purchases in particular) is a significant offset. We are, however, watching the surprising bump in electricity prices to see if this continues.

As housing has a significant group weighting in the CPI (15%) it has a meaningful impact on the estimates of both inflation and core inflation. As such, with core inflation below the bottom of the RBA’s target band we can find little to suggest any risk of a meaningful acceleration.