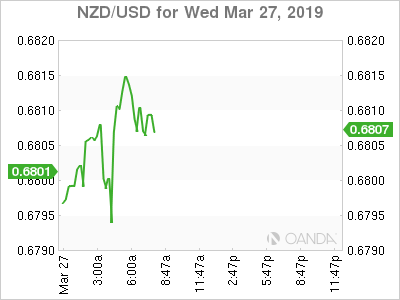

Steady news from across the globe painted a downbeat outlook for global growth. In New Zealand, the RBNZ downgraded their forward guidance from neutral to dovish. ECB’s Draghi noted that risks to the euro zone’s economic outlook remain tilted to the downside. Most investors are targeting China to rebound, but a Bloomberg surveys now show that expectations are for the PBOC to ease less aggressively this year, with the earliest cut next quarter and two more in the second half. Currencies struggled for direction, with the exception of the kiwi, which sold off immediately following the bank’s dovish statement.

- EUR – Draghi keeps dovish hand

- Brexit – MPs to vote on Brexit options

- NZD – RBNZ joins the dove camp

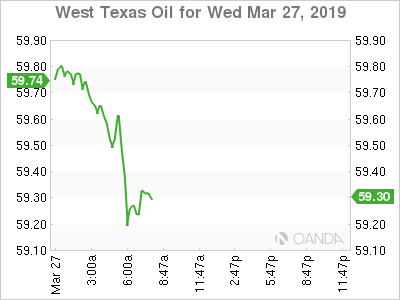

- Oil – Inventory data eyed

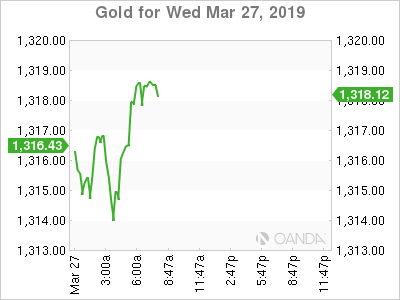

- Gold – rises on safe-haven flows

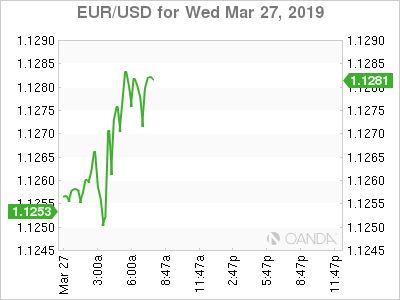

EUR

The euro was little changed following mixed confidence data and dovish reiterations from ECB Chief Draghi and Chief Economist Praet. Confidence data slightly improved in France and declined in Italy, not necessarily pointing to a strong rebound for the Eurozone. Draghi reiterated risks to the euro zone’s economic outlook remain tilted to the downside and a pickup in inflation is delayed, warranting their current accommodative stance that includes negative rates. Praet noted that the natural interest rate to be structurally low for a while.

The German bund fell another 4 basis points, deeper into negative territory at -0.061%. Germany’s bund auction had a negative yield for the first since 2016.

Brexit

Today Parliament has control of the Brexit process and they will try to outline how they want to move forward. Motions will be voted on that will focus on the Brexit process and what relationship the UK wants to have with the EU. We still can’t rule out most potential outcomes, but the general consensus remains, we will not see a no-deal Brexit. May’s deal is gaining some momentum, and that may end up being the best option for Conservative hardliners. It appears that she could win over more votes if she promises to step down for a successful meaningful third vote.

NZD

The RBNZ dovish statement should not have come as a surprise. GDP matched its slowest growth since 2015 and inflation was just below their midpoint target. The second sentence of the interest rate statement summed up everything perfectly, “weaker global economic outlook and reduced momentum in domestic spending, the more likely direction of our next OCR move is down.”

The kiwi fell the most in seven weeks following the decision, down 1.6% to the greenback. The RBNZ fell in line with their peers adopting a very dovish stance.

Oil

West Texas Intermediate crude continues to respect the $60 a barrel level ahead of the EIA’s weekly crude inventory data. Last week’s EIA release saw a surprising near 10-million-barrel draw, current expectations are for this week’s reading is for a near 1 million drop in crude supplies. Late yesterday, the American Petroleum Institute report showed stockpiles climbed 1.93 million barrels.

Oil prices were earlier supported by Russian energy minister Novak’s comments that Russia is poised to reach their production cut pledge of 228,000 barrels per day. OPEC and friends are also considering having a meeting of Joint Ministerial Monitoring Committee in Jeddah, Saudi Arabia on May 19th. While the production cuts have worked to stabilize prices, we could see Russia become less supportive to keep the cuts for an extended time.

One developing story for US shale oil is the growing risks of contamination as the complex infrastructure has oil travel from Texas to North Dakota and eventually all the way to Asia. Two refiners for South Korea have rejected some cargoes over contamination. Further quality issues could see further costs to updating pipelines and that could cause major disruptions.

Oil is likely to be unable to break out much higher unless US production has some headwinds. Current expectations are for US crude exports to rise to a record 5 million barrels by late 2020, a near 70% jump from current levels.

Gold

Gold prices are slightly higher, but still showing no signs of breaking out. Falling Treasury yields, and a gloomier outlook have provided a bid for the precious metal, but gains are capped on optimism for the US and China to reach a trade deal in the next couple of months and high expectations the UK will not have to deal with a hard exit.

{kind=link}