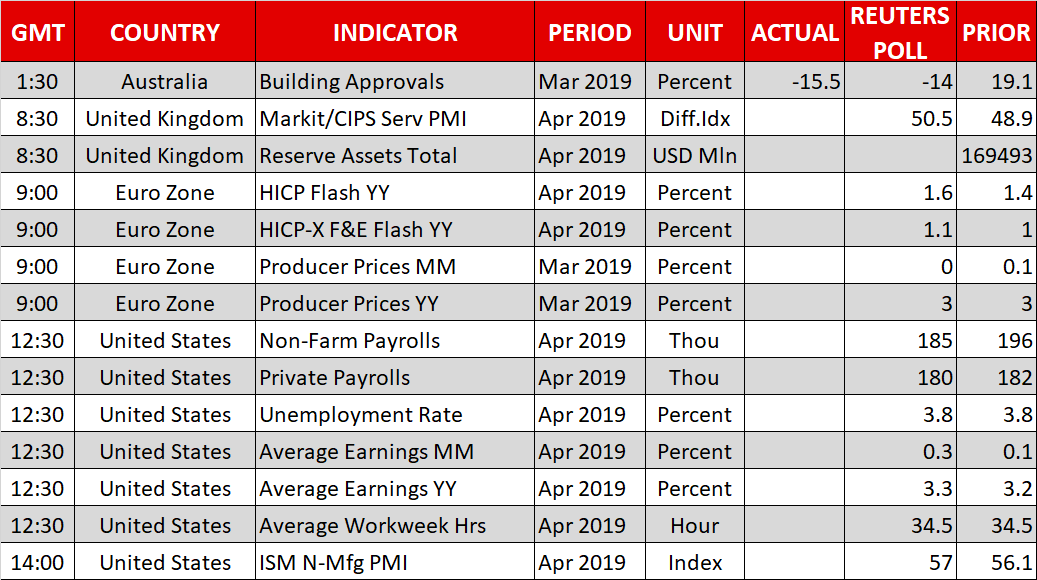

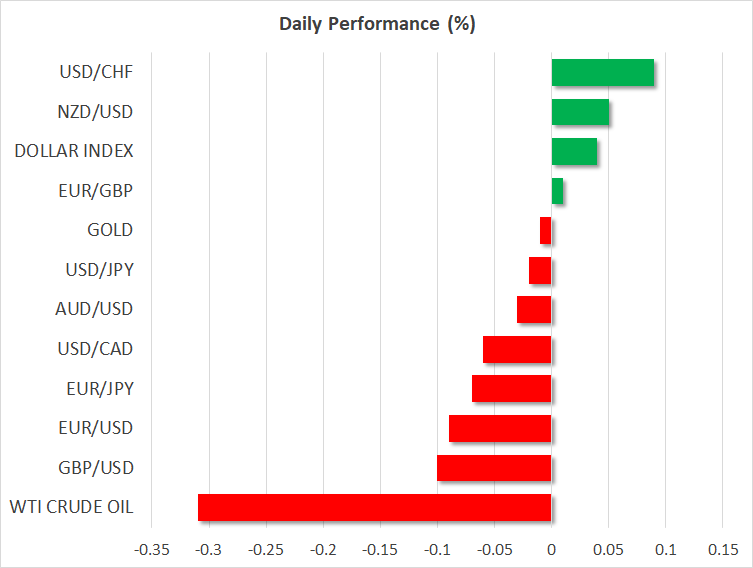

- US dollar extends gains ahead of today’s nonfarm payrolls report

- Aussie hits 4-month low as odds rise of RBA rate cut next week

- Oil prices slump on oversupply concerns as US output continues to surge

Dollar stands tall ahead of NFP report

There was little to hold back the US dollar on Friday as recent solid US data and a not-so-dovish Fed have lessened the odds of a rate cut before the year-end. Investors sharply adjusted their rate cut bets following the FOMC policy meeting on Wednesday when Fed Chairman Jerome Powell said the current weak patch in inflation was likely due to transitory factors. The yields on US Treasury notes jumped higher after Powell’s remarks, providing the dollar with strong near-term support.

Going into today’s all-important nonfarm payrolls report, the median forecast is that the US economy added 185k jobs in April. However, even if the payrolls number beats expectations, it would need to be backed by an equally strong average earnings figure. Average hourly earnings growth has been stuck between 3.2%-3.4% since late last year and is expected to have edged up to 3.3% in April. Any signs that wage growth is moderating could see much of this week’s moves in the currency and bond markets being reversed, with investors once again pricing in a higher chance of a rate cut by the Fed.

For now, though, the greenback is trading comfortably near 2-year highs, with the dollar index rising to 97.88 ahead of the European open.

Aussie and kiwi on the slide in anticipation of dovish RBA and RBNZ meetings

The Australian and New Zealand dollars remained on the backfoot on Friday as traders continued to speculate that central banks in Australia and New Zealand could cut rates as early as their respective policy meetings next week.

Inflation in both countries eased more than expected in the first quarter, while in Australia, there was more poor data this morning. Building approvals slumped by 15.5% month-on-month in March and the AIG services PMI fell deeper into contractionary territory. The aussie hit a 4-month low of $0.6983 after the data, though the kiwi managed to erase its losses to stand flat at $0.6616.

The Reserve Bank of Australia and the Reserve Bank of New Zealand will announce their latest policy decisions next Tuesday and Wednesday, respectively, with investors not ruling out surprise rate cuts.

Bullish dollar weighs on euro and pound

The euro was trading far below its peak of $1.1264 touched prior to Wednesday’s Fed decision as encouraging Eurozone GDP numbers were outshone by the relatively upbeat tone of Powell’s press conference.

The single currency’s best chance of regaining some positive momentum is today’s flash CPI readings for April. A small uptick in Eurozone inflation, especially in core CPI, would provide further evidence that the worst is over for the bloc’s economy.

Sterling has also been drifting lower since the Fed meeting, though it’s held above $1.30 as its declines have been more limited due to rumours that the UK government could agree to accept a customs union plan with the EU in order to win Labour’s backing for the Brexit deal. With both the Conservatives and Labour suffering heavy losses overnight in local elections in England and Northern Ireland, Britain’s two main parties might now be more pressed to find a solution to the Brexit impasse for fear of being punished further by voters.

There was also support for the pound from yesterday’s Bank of England policy meeting when Governor Mark Carney warned markets that the probability of a rate hike in the coming months was greater than that implied by the markets. The immediate focus for the pound now is the services PMI coming out of the UK later today.

Oil under pressure from soaring US production

Outside of forex markets, oil was a notable mover as prices fell sharply yesterday amid fresh fears of oversupply. US crude stocks jumped by a massive 9.9 million barrels last week and output hit a new record high of 12.3 million barrels per day. There’s also reports that Saudi Arabia could raise output in June. Rising production from the US has helped ease some of the supply constraints from OPEC’s output restrictions as well as from sanctions on Venezuelan and Iranian exports.

WTI oil recovered slightly from yesterday’s one-month low of $60.95 per barrel, while Brent crude was also off its lows to trade around $70.35 a barrel.