Central banks cut interest rates when fears over an economic downturn are seriously mounting. This is the impression that markets are currently getting from the US as weakening economic data combined with heightening external risks dampen economic projections and hence raise the stakes for a rate reduction. The Federal Open Market Committee, however, announces its policy decision this Wednesday at a crucial time, a week before the G20 summit in Osaka, and policymakers may wisely judge that this is not the right moment to proceed, well not before Washington and Beijing clarify the situation on the trade front anyway.

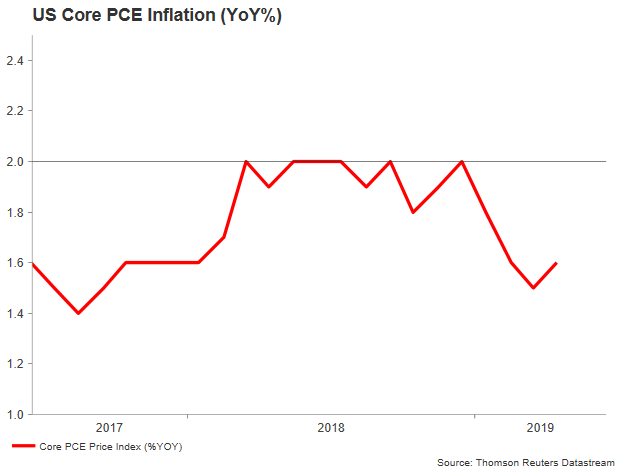

At the start of the current year, the Fed, which delivered four rate hikes in 2018, was confident that further tightening will follow soon, but rolling into the first quarter, economic numbers worsened along with trade tensions, making the Fed somewhat hesitant about future rate hikes. The core PCE index, the Fed’s favorite inflation measure, followed a downtrend after hitting the 2.0% target in March even with tariffs going into effect. The core CPI, another closely watched price indicator, also decelerated, making markets wonder whether the inflation weakness is indeed transitory as Fed chief Powell supports or something more temporary, such as a discouraged domestic demand.

Adding to the worrisome picture was May’s Nonfarm payrolls report. Although the unemployment rate steadied at a 50-year low, workers disappointingly did not see much of the benefit as average hourly earnings slowed for the second consecutive month. New job hiring was not great either but rather disappointing, with the economy creating less than 100k jobs for the second time in four months and previous readings seeing downside revisions.

And if the above are not enough to back a rate cut, the ISM manufacturing PMI slipped unexpectedly to the lowest point since Trump’s election in May, mirroring to an extent the problems caused by the heavy US import tariffs on industrial activities.

James Bullard, the St. Louis Fed president and an FOMC voter in 2019, was the first to call for a downward adjustment in policy since the Fed surprisingly adopted a more patient approach in January. He messaged that the direct effects of the trade war to the US economy are relatively small but the spillovers from the global financial markets could be larger and hence lower rates maybe needed to prevent inflation from falling and generally mitigate a larger-than-expected growth slowdown. While such an opinion is more or less awaited from a dovish policymaker, the Fed chief, Powell, a centrist, did not rule out the scenario when he spoke about monetary issues earlier this month. Instead he said that the Bank was “closely monitoring” the implications of trade developments and would act accordingly to sustain a healthy expansion. More importantly, he refrained from characterizing current interest rates as appropriate and avoided to signal a patient approach as in previous speeches, with markets translating his comments as a change of policy.

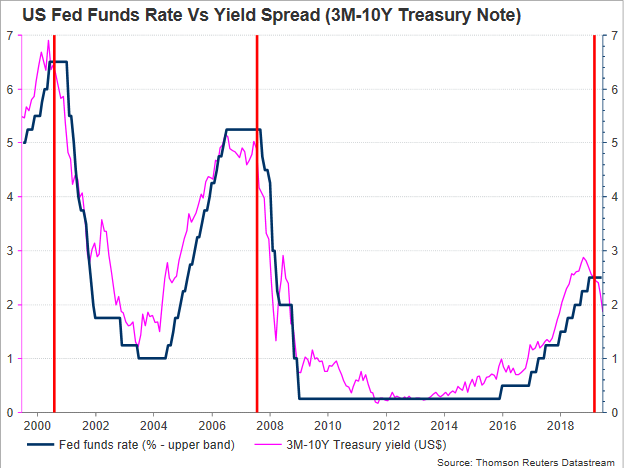

Consequently, treasury yields justifiably plunged and the bets for a rate cut soared, with Fed Funds futures heavily pricing two rate reductions by September. Nevertheless, with the G20 summit getting underway just a week after the FOMC gathering on June 28-29, we don’t expect any change in policy on Wednesday. The Bank will probably await a trade update from Trump and Xi Jinping before taking action. Should the leaders show willingness to move towards a deal, policymakers may delay easing in coming months until the two sides finally secure an agreement. On the other hand, if the summit proves fruitless, increasing doubts about whether and if a trade deal could be reached, a rate cut may come as soon as in July to save the economy from a sharper growth slowdown. It is also worth noting that the spread between the 10-year and 3-month Treasury yields is currently negatively sloped and below the Fed funds rate and such a negative spread was followed by a rate cut in previous years. Besides, with Trump starting his re-election campaign for the 2020 presidential elections later this month, the central bank may face stronger pressure to pull back interest rates in coming months.

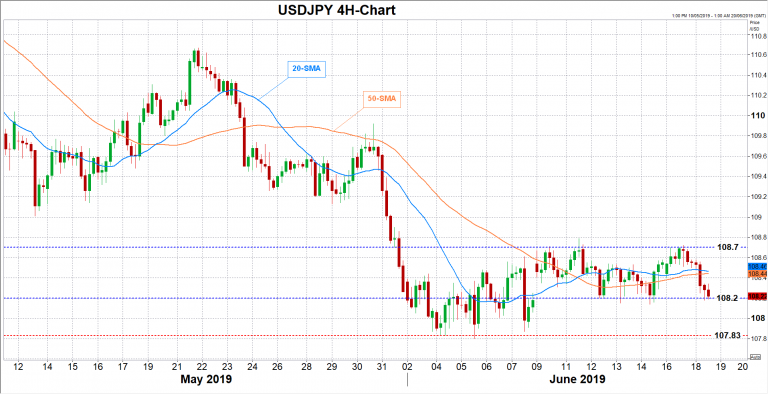

In terms of market reaction, investors and traders will pay special attention on the famous dot plot that displays policymakers’ forecasts for future rate movements, and new economic projections. Should the the Bank keep rates steady but more policymakers take the rate cut side, with the dot plot showing potentially at least two rate cuts this year, USDJPY could break support at 108.20 and retest the 108 round-level before heading to the 107.83 bottom. Losses could also emerge if the Bank delivers a surprising rate cut on Wednesday. Equities could surge in this case.

On the positive scenario, the greenback could rally above its 20- and 50-period simple moving averages (SMA) and up to the 108.70 resistance if the Fed leaves rates the same and repeats the need for patience, hinting that conditions are not as bad as markets believe.

{kind=link}