U.S. Review

The Economy’s Momentum Continues to Wane

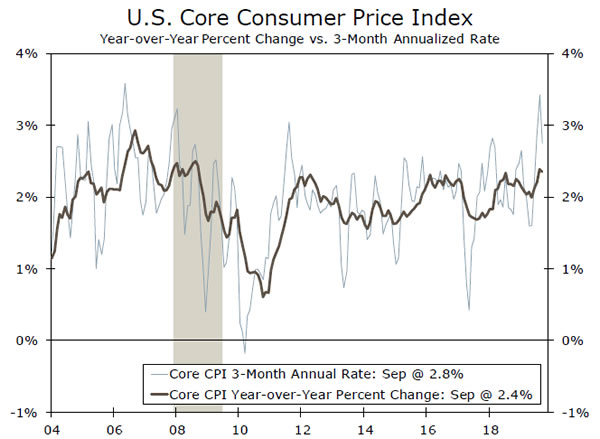

- Consumer price inflation eased up in September. On a year-ago basis the trend remains firm, but the weaker print for September reduces the risk of inflation breaking meaningfully higher and threatening the Fed’s easing bias.

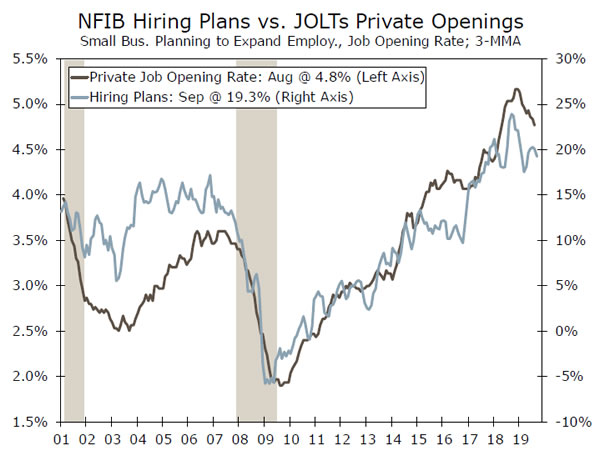

- The inflation side of the Fed’s mandate remains under control, but job openings for August hinted at a crack in the labor market. Openings fell for a third straight month and are down 7.5% since January.

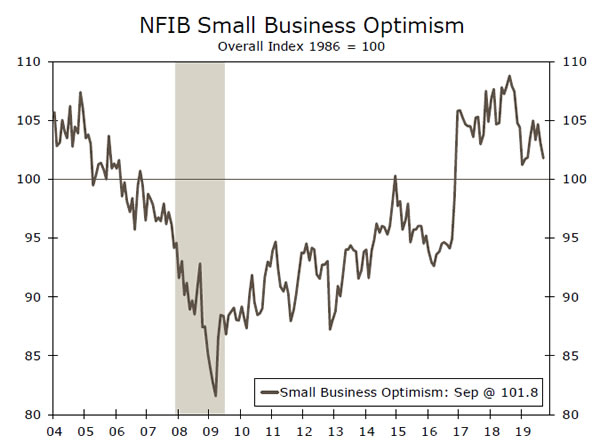

- Optimism among small businesses eroded a bit more in September, with the NFIB index falling to 101.8. Fewer businesses expected higher sales or to hire more workers.

The Economy’s Momentum Continues to Wane

Further signs that the economy is losing some momentum piled up this week. Confidence among small businesses continues to fade, inflation softened and, perhaps most worryingly, businesses are less interested in hiring.

Optimism among small businesses took another leg down in September, with fewer businesses reporting that they expected sales and the economy to improve. At 101.8, the NFIB small business index is not quite as low as it was at the start of the year following the stock market’s sharp selloff and the longest government shutdown on record. However, optimism has clearly faded, with the index down from 108.8 in August 2018.

The trade war has not been limited to large multi-national corporations; 30% of small businesses reported tariffs are having a negative effect on their business. At the same time, “mumblings about a coming recession” were more frequent among respondents, according to the report. With the outlook dimming, hiring plans fell to more than a two-year low in September.

Declining job openings echoes the waning optimism among small businesses. Job openings fell for a third straight month and are down 7.5% since January. The pullback is nearly on par with the 2015-16 mid-cycle slowdown, when a drop in job openings presaged a moderation in hiring. However, at the nadir of that period, in October 2016, the global outlook was beginning to firm and both ISM indices had already turned around. With no end to the trade war in sight and global growth still floundering, a turnaround seems at least some ways off. As such, the pullback in job openings is more troubling today and suggests a further slowdown in hiring is in the offing.

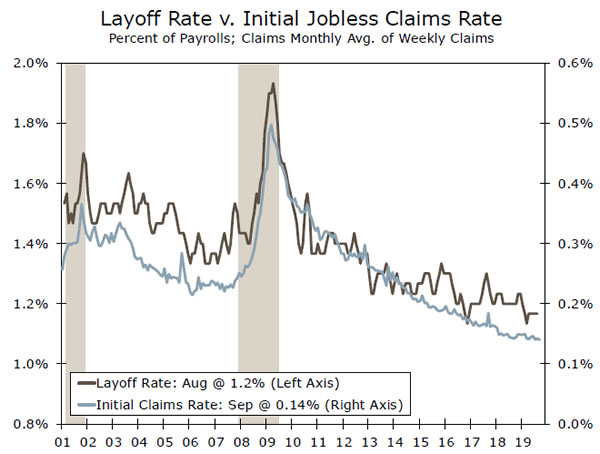

The good news is that layoffs as measured by the Job Openings and Turnover Survey as well as initial jobless claims remain historically low. Jobless claims fell by 10K this week, keeping the four-week average around 210-215K. Yet separations are only part of the net hiring equation. Before laying off existing workers, businesses tend to stop bringing on new workers, so openings and hiring plans can provide earlier signs of stress in the labor market. For example, ahead of the last downturn, job openings peaked in March 2007, whereas initial jobless claims did not begin to move up until October, seven months later.

Reluctance by firms to bring on new workers points to a moderation in income and consumer spending growth. Consumers received a bit of a reprieve on that front in September, however, with the CPI unchanged. Overall prices are up a moderate 1.7% year-over-year, thanks to a drop in energy prices.

Core inflation also eased up from a torrid pace this summer, as prices rose 0.1% in September, compared to 0.3% in each of the prior three months. Nevertheless, core CPI is still up 2.4% over the past year, matching the fastest one-year change this expansion. That pace is unlikely to deter most Fed officials from their easing bias, however, given that weaker prospects for U.S. and global growth are expected to weigh on inflation in the coming months and offset the temporary boost from tariffs.

U.S. Outlook

Retail Sales • Wednesday

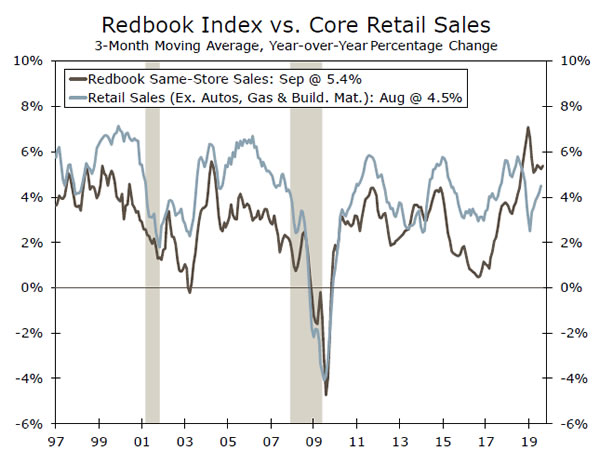

All eyes will be on the September retail sales report on Wednesday, as analysts take the latest pulse of the U.S. economy. At a time when most economic discussions have been dominated by recession risks, the U.S. consumer is one facet that has continued to perform. Consumer confidence measures remain elevated but have moderated recently, while concern over the impact of tariffs has been spontaneously mentioned by consumers in recent surveys. High frequency data, such as the Johnson Redbook Index for same store sales, suggest sales remained strong last month. While households certainly have the means to spend, our concern of late lies more in their continued willingness to do so. We expect sales rose 0.2% in September. A miss to the downside could be evidence of the trade war decidedly weakening confidence, and thereby spending. An upward surprise, however, may calm fears that weakness in manufacturing is spilling into consumer spending.

Previous: 0.4% Wells Fargo: 0.2% Consensus: 0.3% (Month-over-Month)

Housing Starts • Thursday

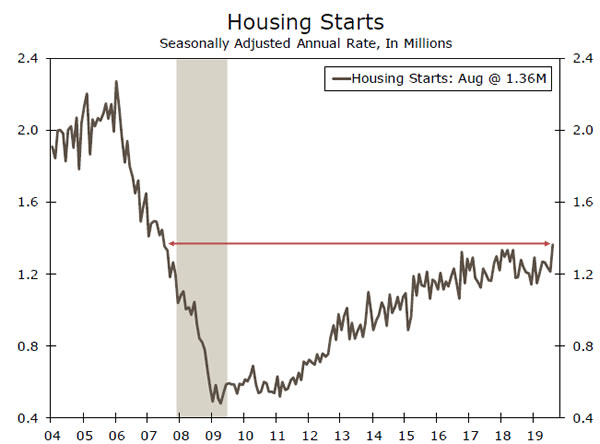

Housing starts is another area likely to grab market attention next week. After dragging on GDP growth for six consecutive quarters, residential construction is finally poised to boost growth in the third quarter. Total housing starts jumped 12.3% to a 1.36 million-unit pace in August, the highest since June 2007. Optimism is also higher. The National Association of Homebuilders (NAHB) Housing Market Index rose to 68 in September, an 11-month high. The increase was due to an improvement in builders’ assessments of current sales, boosted by the sharp decline in mortgage rates and the tight labor market. Stronger optimism should lead to increased construction, but a surge is unlikely as builders remain cautious. Trade policy uncertainty and stock market volatility are likely holding back homebuilders, who are wary of a sudden pullback in demand. Still, the stronger sales pace and improving confidence should feed through to stronger construction later this year.

Previous: 1,364K Wells Fargo: 1,306K Consensus: 1,320K

Industrial Production • Thursday

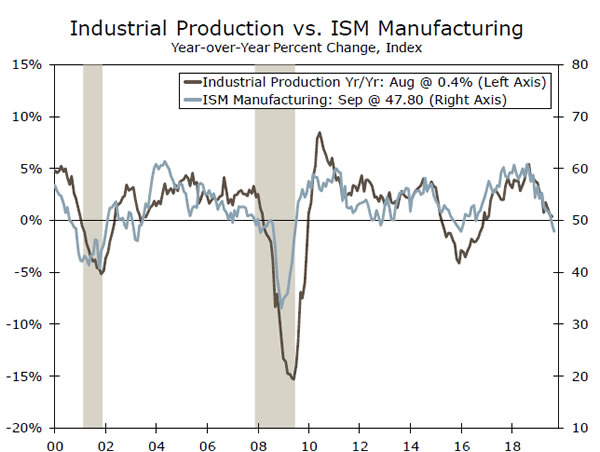

Later on Thursday, attention will turn to the latest read on industrial production (IP). The manufacturing sector continues to struggle in the face of trade uncertainty and weak global growth. Survey data suggest a weak read for September IP is likely in store. Last week, the ISM manufacturing index flashed signs of recession, sliding further into negative territory in September to the worst reading since 2009.

The attack on Saudi Arabian oil facilities should not have had a large impact on mining output, as WTI oil prices quickly stabilized after surging to $60+ per barrel. However, we wouldn’t be surprised to see an effect from the General Motors (GM) employee strike—where roughly 48,000 workers have been on strike since September 16. It has the potential to show up in two places—motor vehicle & parts and consumer autos—and will likely weigh on IP.

Previous: 0.6% Wells Fargo: -0.4% Consensus: -0.2% (Month-over-Month)

Global Review

Light at the End of the Brexit Tunnel?

- The Brexit rollercoaster carried on up and down the track over the course of the week, with a full pendulum swing from dashed hopes for a deal to a surge in optimism. The two sides appear to have moved substantially closer to reaching a deal, but we caution that any deal is still subject to the approval of U.K. and E.U. Parliaments, which is hardly a sure thing.

- There were limited releases from key international economies this week. U.K. activity figures suggest the economy avoided technical recession in Q3, while German activity figures confirmed what we already knew: the manufacturing sector is in the doldrums.

The Brexit Rollercoaster Rolls On

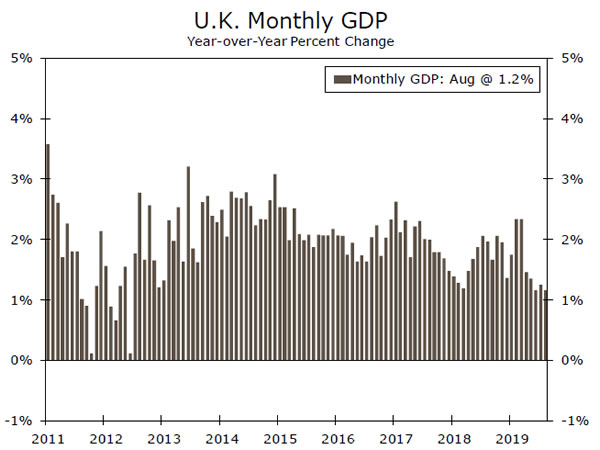

The past week has been something of a rollercoaster for Brexit developments. Early in the week, the E.U. and U.K. seemed to have given up all hope on reaching a deal. Indeed, a top E.U. official was quoted in the earlier part of the week as saying the only two options were a no-deal Brexit or an extension of the October 31 deadline. Just when all hope seemed lost, headlines emerged late Thursday that a breakthrough had been reached and the two sides saw a path toward a deal. It is not exactly clear at this point what was agreed upon as the two sides are still hashing out the details. However, while we do not necessarily doubt that the U.K. and E.U. have reached an agreement, we are concerned that any deal is still subject to approval from U.K. and E.U. Parliaments, with the former arguably presenting the biggest hurdle. Until we have more concrete details, we remain of the view that Brexit will merely be punted yet again, with the two sides likely to end up extending the current October 31 deadline by perhaps three months to January 31. A snap general election is likely to take place around late November or early December, and could dictate the Brexit trajectory as we head into 2020. That said, there is still a non-zero risk of a no-deal Brexit on October 31, and even if the deadline is extended until January, the risk of no-deal will simply be prolonged. Meanwhile, this week’s U.K. data were mixed. GDP unexpectedly fell 0.1% on a sequential basis in August, but prior months’ data were revised higher. The net result implies GDP growth of around 0.2%-0.3% on a sequential basis in Q3, suggesting that the U.K. economy probably avoided a technical recession. Industrial output fell 0.6% during the month, led by a 0.7% decline in manufacturing output.

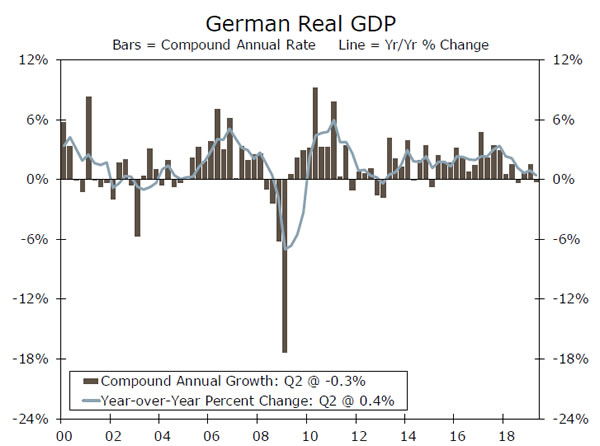

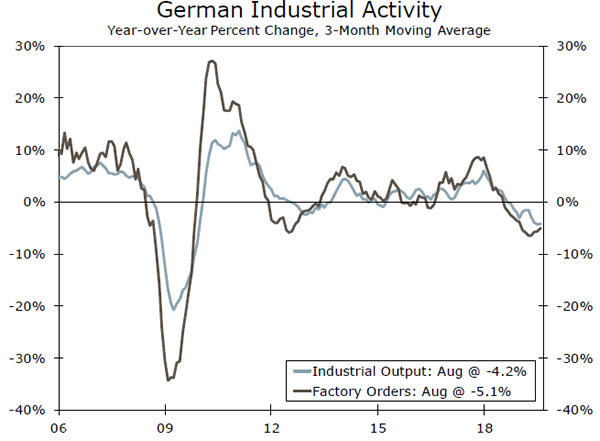

This week’s data from the Eurozone were mixed, but generally confirmed what we already knew: the economy is flagging. German factory orders declined 0.6% on a sequential basis in August, a bit more than expected, although industrial output edged higher by 0.3%. Still, on balance, as the middle chart shows, German industrial activity is clearly still in the doldrums, and it is very likely that the German economy fell into technical recession in Q3. That said, the labor market has not yet shown material signs of deterioration, with consumer spending still holding up. This interplay between floundering industrial output and the services sector will be important to watch to assess where the German, and broader Eurozone, economy goes from here.

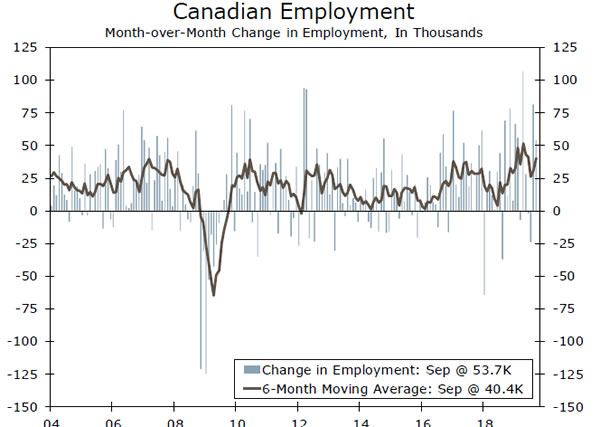

On a more positive note, Canada’s September employment report was strong across the board. Employment rose 53,700 during the month, with all the increase in full-time jobs, while the jobless rate fell to 5.5%. Meanwhile, wage growth unexpectedly firmed to 4.3% year-over-year. The report underscores the resilience of the Canadian economy, which has held relatively firm in the face of global trade uncertainty and slowing growth in the United States. To be sure, Canada has not been immune, as real GDP growth has slowed considerably from the highs, but the ongoing resilience in the labor market shows the underlying health of the economy is solid.

Global Outlook

Eurozone Industrial Output • Monday

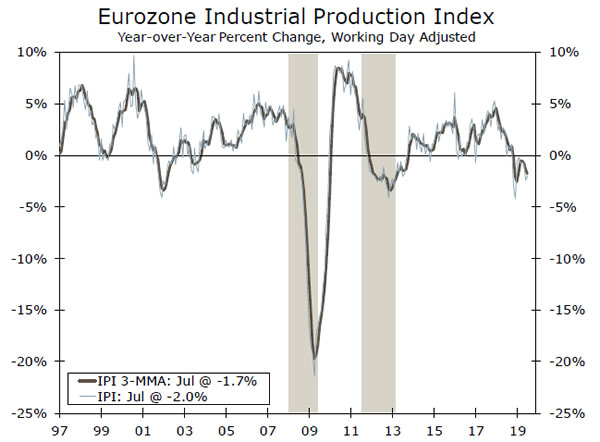

The Eurozone’s industrial sector has been languishing for over a year now, with output declining on a sequential basis in eight of the last 12 months. To be sure, most other large developed economies are coping with similar weakness in industrial activity, but the Eurozone’s (particularly Germany’s) relatively higher reliance on industry as a share of the economy has brought the region to the brink of recession.

The key question, in our view, is whether the industrial slowdown spreads to other areas of the economy. There are initial signs this is happening, as the Eurozone services PMI fell sharply last month, while industrial orders for consumer goods have showed particular weakness recently. We are not yet ready to call time on the Eurozone economic expansion, but the divergence probably cannot last forever. Either the industrial sector needs to recover, or it will likely drag the rest of the economy down with it.

Previous: -0.4% Consensus: 0.3% (Month-over-Month)

U.K. Employment Report • Tuesday

Broadly speaking, the U.K. labor market has been relatively resilient over the past few years in the face of Brexit uncertainty. Employment growth has downshifted modestly since the referendum in 2016 but has generally remained solid, and the unemployment rate has moved down considerably since then. Meanwhile, wage growth has continued to trend higher, perhaps somewhat puzzlingly given subdued productivity and generally below-target inflation.

The result of this strength in real wage growth has been, for the most part, relatively robust consumer spending growth. However, our concern is that this combination of trends may not be sustainable. If wage growth remains at current levels or picks up further, companies may have to raise prices, and inflation could move higher. In contrast, absent a burst of productivity growth, U.K. firms may see their margins erode over time.

Previous: 31,000 Consensus: 26,000 (Emp. Change 3M/3M)

Canada CPI • Wednesday

Canada’s economy has been among the more resilient of the major developed economies thus far this year. Topline GDP growth has been soft, but the underlying pace of demand in Canada has held up reasonably well, and the labor market looks fairly healthy. Meanwhile, CPI inflation—both headline and core—has hovered right near target for most of the past year or two. Against that backdrop, the Bank of Canada (BoC) has held policy steady for quite some time even as many other large developed countries’ central banks have eased policy.

Looking ahead, however, we expect the BoC to cut rates just once later this year, in December. That reflects the likelihood that slower U.S. economic growth will weigh on Canada’s economy, albeit modestly, while our expectation that the Federal Reserve will cut rates two more times by Q1-2020 also factors into our BoC view.

Previous: 1.9% Wells Fargo: 2.1% Consensus: 2.0% (Year-over-Year)

Point of View

Interest Rate Watch

Treasury Yields Rebound

Treasury yields rose this week amid mixed signals from the European Central Bank on the need for additional asset purchases and some increased optimism about trade talks with China. Early Friday morning, the yield on the 10-year Treasury was up about 20 bps from the prior week and the yield on the 2-year note rose around the same amount. While optimism about trade has been cited for most of the increase, this week’s auction of 10-year and 30-year bonds did not go particularly well, which also pushed yields higher. The lighter interest in bonds came despite better than expected PPI and CPI inflation data.

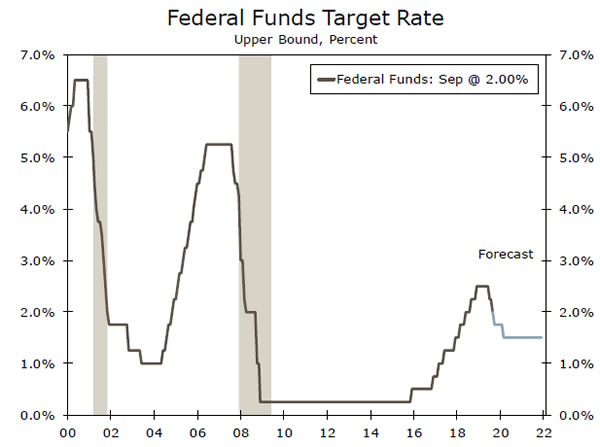

Comments by Fed officials were also supportive of lower rates. Fed Chairman Jerome Powell disclosed that the Federal Reserve would resume bill purchases in order to help stabilize the overnight funding markets. Powell was quick to note that this did not mark the beginning of another round of Quantitative Easing but rather was aimed at simply bringing stability to the short-term funding markets. Banks appear to be using reserves differently in this cycle, requiring the Fed to maintain a larger balance sheet than previously thought. The Fed’s move should help prevent a more significant liquidity crisis that might cause real trouble for the economy from developing. But the Fed also does not want anyone to interpret this move as an easing. Given the rise in yields this week, it appears the market is taking the Fed at its word.

The slightly better than expected inflation reports clear the way for the Fed to cut the federal funds rate by another quarter point at its October 29-30 FOMC meeting. We would expect to see one or two dissents, as FRB Kansas City President Esther George made it clear this week that she does not see anything in the inflation data that would indicate that inflation expectations have shifted toward disinflation or deflation. We continue to look for two more quarter point cuts, as the Fed sees the current environment reminiscent of the late 1990s, when slower growth overseas caused the Fed to cut the federal funds rate three times, a total of 75 bps, which then reignited growth and allowed it to hike rates later in the cycle.

Credit Market Insights

Student Loans Lead Credit Growth

After a solid increase in U.S. consumer credit the previous month, Americans slowed their pace of borrowing in August, led by weaker credit card debt. Total consumer credit increased $17.9B, as revolving credit, which includes credit card borrowing, fell $1.9B. The non-revolving sector, which includes educational and automobile loans, helped offset the decline, increasing $19.8B—the biggest monthly advance since August 2016—compared to a $13.7B increase the previous month. The gain likely reflected the start of a new school year at most universities. More than 44 million Americans have student loan debt and growth in this category continues to be a concern among analysts as one of the country’s most widespread financial burdens.

When looking at the consumer credit report, it is important to note that it is a volatile indicator and therefore the overall trend should be more closely watched rather than the month to month change. With this in mind, the overall report suggests that consumers may be pulling back on borrowing, likely in part due to cooling job growth amid deteriorating global sentiment as well as risks of a worsening trade war. U.S. job openings unexpectedly declined in August to the lowest level since March 2018, while average hourly earnings saw the weakest annual gain in more than a year. In addition, personal spending was softer in August, and PCE is now on track for a sub-3% print in the third quarter.

Topic of the Week

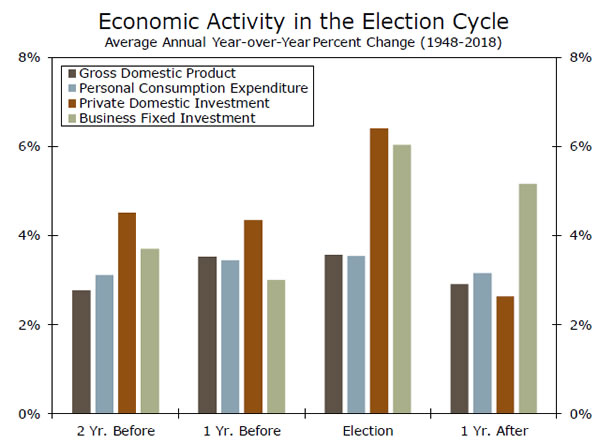

Election Uncertainty and the Economy

The negative effects of uncertainty on economic growth have been in the spotlight over the past year, as questions about trade policy have clouded the economic outlook and pushed some businesses to hold back on capital expenditure and hiring plans. With 2020 looming, it is worth considering the potential impact of uncertainty stemming from this upcoming election cycle. Elections often involve candidates with very different views on government spending, taxation and regulation. These divergent policy paths can make it difficult for consumers and businesses to feel confident about making large purchases or investments. But is this phenomenon significant enough to show up in the aggregate data?

In a recent report, which builds on an early report from 2016, we look at how the economy fared in prior election cycles. On average, it appears that election years are stronger, not weaker, than non-election years (top chart). There does not appear to be a slowdown in spending by businesses or consumers in the run up to the election, nor is there a pop in economic activity after the election. These results hold true when controlling for recessions, which often appear as outliers in the economic data. So what drives this surprising result?

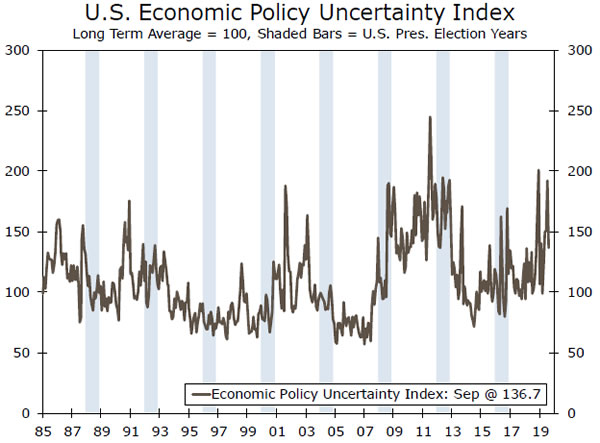

Election-related uncertainty is just one of numerous factors that may affect the economy in a given year. Our recent report delves into statistical implications of this, but essentially it is difficult to separate these other effects from a potential election effect. The lack of this election uncertainty effect could also be understood through trends in economic policy uncertainty. For one, policy uncertainty is not limited to election years and the effects of policy uncertainty might be too diffuse to exhibit a clear pattern across the election cycle. Additionally, while policy uncertainty is not new, it has been increasing over time and has been noticeably higher in the past two decades. While not all of this is due to elections, more competitive and polarizing elections and can lead to more uncertainty. In sum, a review of historical data shows little connection between election uncertainty and economic activity, but this could change if more recent trends become the norm.

{kind=link}