U.S. Review

OK Monty, Let’s Go With Door# 1, Door #2 AND Door #3

- Lawmakers and the administration made breakthroughs this week on deals to avoid the Dec. 15 tariffs, likely pass the USMCA and avert a government shutdown next week. The USTR confirmed that Sunday’s tariffs will not go into effect and the 15% tariff on approximately $120B will decrease to 7.5%.

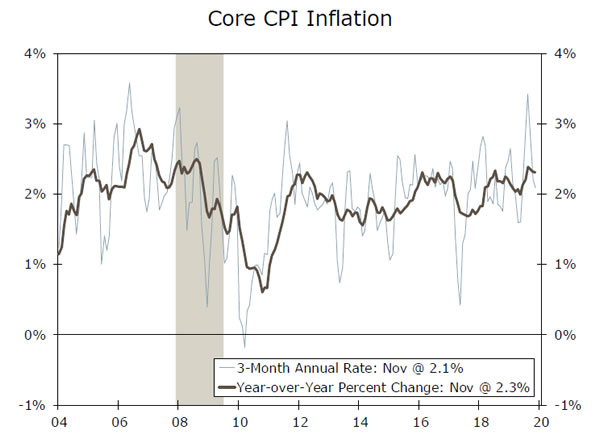

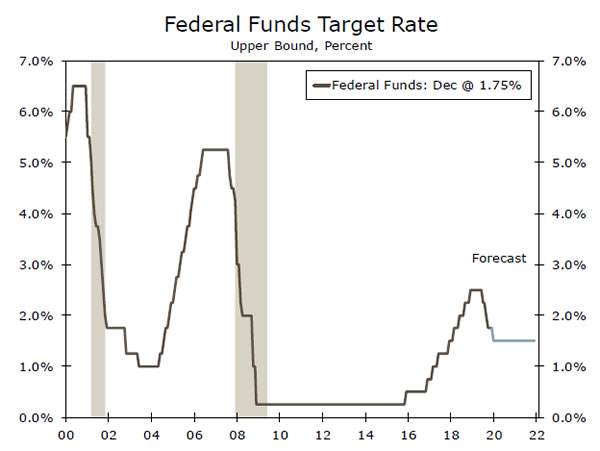

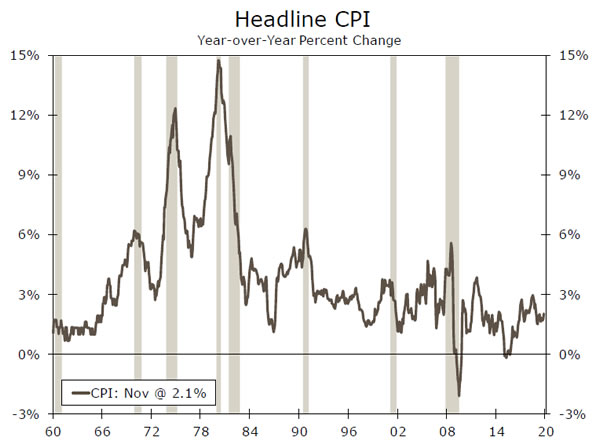

- The FOMC left rates unchanged this week and reiterated that it would need to see a material change in the outlook to adjust rates from here. The inflation data this week showed no signs of a significant change with the core CPI remaining at 2.3% year-over-year, while retail sales growth continued to moderate after a hot pace this summer.

Let’s Make a Deal, or Three

Wheeling and dealing was pervasive in Washington this week. First, lawmakers are said to have reached a deal to fund the government ahead of next week’s deadline, averting another government shutdown. Second, a long-sought Phase I trade deal between the United States and China crossed the finish line this morning. The Office of the U.S. Trade Representative released the details, which avoided the additional tariffs on $156B in imports of Chinese goods that were set to go into effect on Sunday and scaled back the 15% tariff on about $120B to 7.5% in exchange for more agricultural purchases. The 25% tariff on approximately $250B of imports from China remains and the deal still did not fully address some of the fundamental issues that sparked the trade war. The finalization of the deal points to some upside for our current forecast.

Third, the passage of USMCA, the successor to NAFTA, looks more assured. House Democrats this week endorsed an updated version of the bill that looks likely to pass the Senate once taken up in 2020. The upcoming passage will remove a source of some uncertainty for affected industries, particularly autos. However, since the deal tweaks rather than overhauls NAFTA, we see it having little effect on growth beyond offering some clarity on policy that will allow businesses to proceed with some investment decisions.

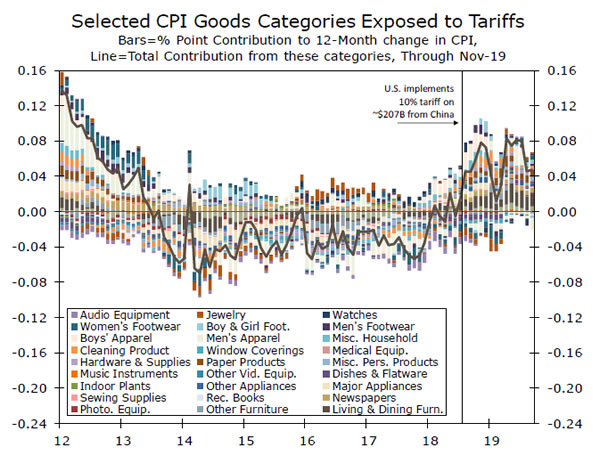

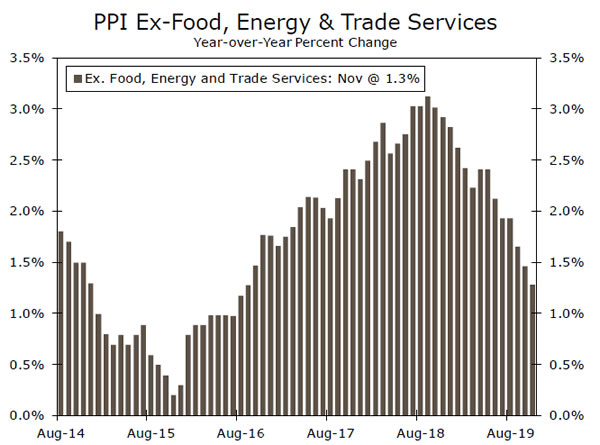

As we anticipated, the tariffs that have gone into effect thus far have had minimal impact on inflation. The CPI goods categories that most align with the tariffs implemented to date have added only 0.05 percentage points to inflation over the past year, which is about 0.1 points more than their contribution in the five years before the new tariffs went into place (when those categories where on average a drag on inflation). Looking at all core consumer goods, prices were unchanged in November after declining the prior two months. Driving core inflation higher, however, was a pickup in core services. The underlying trend in inflation remains fairly steady. Overall consumer price inflation ticked up to a 2.1% year-over-year pace in November, but the core index was stable at 2.3%. The producer price index suggest that domestic inflation pressures remain generally tame. The index was unchanged in November, held down by a drop in services. Our preferred measure of core PPI inflation, which excludes food, energy and trade services (measured in margins), was also flat on the month, but has slipped to 1.3% year-over-year—a three-year low—as input costs have eased.

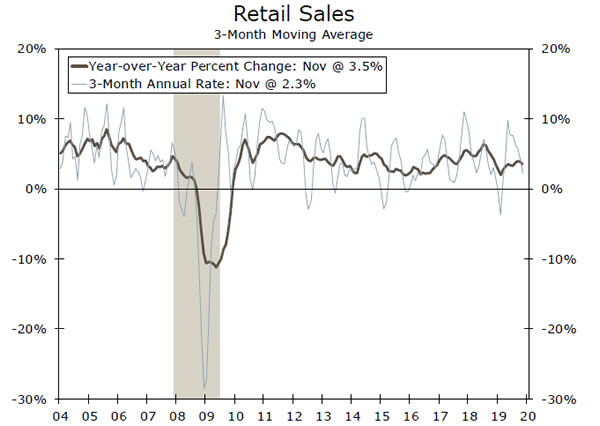

In FOMC Chair Powell’s press conference this week, he noted he would need to see a “significant” and “persistent” increase in inflation before it would be likely that the committee would raise rates again. While we expect the core PCE deflator, which has been running unusually cool relative to core CPI, to move back up to 2% this spring, this week’s inflation data continue to show few signs of the trend in inflation breaking meaningfully higher anytime soon. Retail sales increased 0.2% in November. Holiday sales look off to a slow start, with our measure increasing 0.13% last month. We expect to see some pickup in December, however, given the stillsolid spending positions of households.

U.S. Outlook

Housing Starts & Resales • Tues. & Thurs.

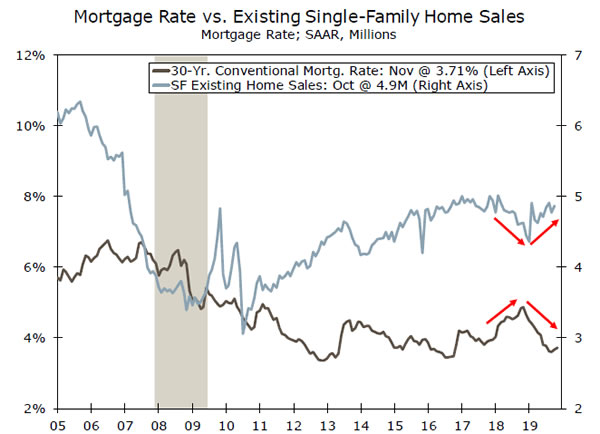

We expect residential activity will continue to modestly accelerate into the new year, and next week we expect new construction and sales of existing homes to post gains in November.

We expect housing starts will rise to a 1,346K-unit pace as lower mortgage rates, firmer demand and rising builder optimism buoy the construction outlook. The National Association of Homebuilders/Wells Fargo Housing Market Index is also published next week on Monday. This forward-looking measure of the singlefamily market continues to augur strength for the housing market— the index is sitting at 70, compared to just 56 during the market turmoil at the end of last year.

Existing home sales should rise to a 5.55 million-unit pace in November, as rising mortgage applications for purchase and pending home sales point to solid demand in the pipeline.

Previous: 1,314K & 5.46M Wells Fargo: 1,346K & 5.55M Consensus: 1,340K & 5.45M

Industrial Production • Tuesday

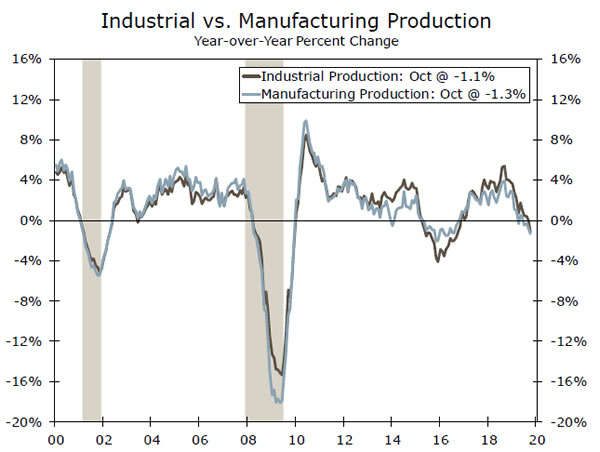

Our slightly above-consensus call for a 1% rise in industrial production in November reflects to a large extent a bounce-back from last month’s ugly -0.8%. The October data were dragged down by the GM strike, but the underlying trend is weak as well. Penciling in our forecast for a monthly gain of around 1% still leaves the level of manufacturing output below where it was last year. A bonafide trade deal with China could lift the industrial sector, but for now we see output continuing to move more or less sideways.

Fresh regional surveys next week will provide some color on manufacturing across the Mid-Atlantic, Northeast and Midwest. The Empire Manufacturing survey prints on Tuesday, along with the Philly Fed survey on Thursday and the Kansas City Fed survey on Friday. Renewed strength should be viewed with caution, however, as the regions have varying exposures to China that do not line up perfectly with the nation as a whole.

Previous: -0.8% Wells Fargo: 1.0% Consensus: 0.8% (Month-over-Month)

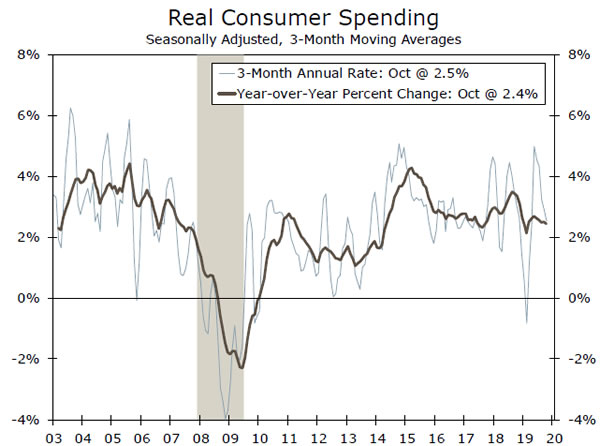

Personal Spending • Friday

We expect personal spending to rise a solid 0.4% in November, but a below-consensus print for retail sales for the same month introduced some downside risk to that forecast.

Still, solid consumer fundamentals should support spending growth through year-end. We expect personal income to post a similarly solid 0.4% rise in November, while consumer sentiment—we also get the final print for the University of Michigan measure on Friday next week (the preliminary reading showed a hefty 2.4-point rise)— remains elevated.

The third and final estimate of Q3 GDP, also released on Friday, should confirm that PCE rose at a 2.9% pace. We are forecasting a slight moderation in growth to 2.1% in Q4, a large reason we have overall GDP growth slowing to 1.5% in Q4 from 2.1%.

Previous: 0.3% Wells Fargo: 0.4% Consensus: 0.4% (Month-over-Month)

Global Review

U.K. General Election in the Spotlight

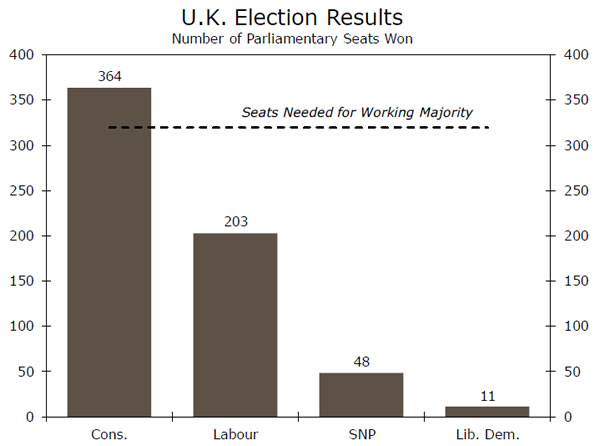

- It was a busy week for international data and events. In the United Kingdom, Conservative Party leader Boris Johnson secured his position as prime minister, winning a comfortable majority in the House of Commons. The pound surged after Johnson’s win, but has since eased a little.

- At the first monetary policy meeting for Christine Lagarde, the European Central Bank held monetary policy steady as expected and made minimal changes to its economic projections. Meanwhile, Sweden’s inflation figures exceeded expectations, as CPIF inflation firmed in November.

ECB Keeps Rates Steady

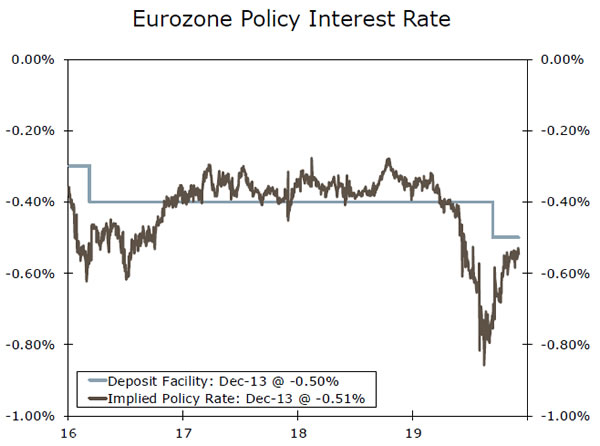

The European Central Bank (ECB) opted to hold rates steady, in line with market expectations, and made minimal changes to its economic projections at its December monetary policy meeting. In the accompanying statement, the ECB reiterated that rates will stay at present levels or lower until it sees the inflation outlook reach a level that is close to, but below 2%. It also stated that the Governing Council will continue its asset purchase program until shortly before it starts raising rates. Following the statement, markets closely watched the subsequent press conference, the first for new ECB President Christine Lagarde. In her comments, she said that downside growth risks still remain but are less pronounced, adding that there are initial signs of stabilization in growth and mildly firmer underlying inflation. Although Lagarde seemed a bit more upbeat on the Eurozone economy, we are not convinced that the economy is fully out of the woods yet, instead looking for a further slowdown in GDP growth in Q4-2019 and perhaps into Q1-2020 as well. Meanwhile, despite the recent tick higher in underlying inflation, inflation expectations remain subdued and the ECB’s inflation target remains a long way off at this point. Accordingly, we still expect the ECB to cut its deposit rate an additional 10 bps to -0.60% in Q1-2020.

Boris Johnson Wins by a Landslide

The Conservative Party won a majority of seats (364 out of 650) in the House of Commons and Boris Johnson will remain the prime minister, largely in line with expectations. The main opposition Labour Party under Jeremy Corbyn won only 203 seats, while Scottish National Party and Liberal Democrats won only 48 and 11, respectively. The pound surged after Johnson’s landslide victory, but has since eased a little. For the next steps, the Conservatives will likely ratify the withdrawal agreement and leave the European Union with a deal by January 31, 2020. As we have noted in past reports, this would not mark the end of the Brexit process, but the beginning of longer term E.U.-U.K. trade talks, which should begin in late Q1-2020 or in Q2. The current withdrawal agreement provides a “transition period” of only 11 months, which, in our view, is unlikely to be enough time to finalize a deal. Therefore, we expect both sides to extend deadlines in order to continue conducting trade talks, which could be a downside risk for the U.K. economy.

Sweden’s November Inflation Suggests Riksbank Hike

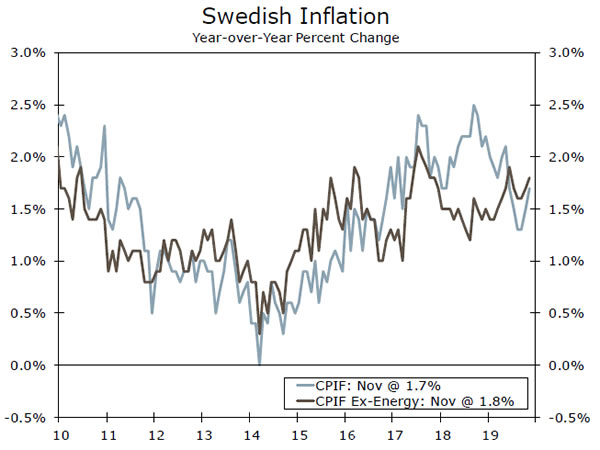

Sweden’s latest inflation report printed higher than expected in November with CPIF inflation rising in line with the Riksbank’s projection to 1.7% year-over-year from 1.5% in the previous month. Although inflation in Sweden remains below the central bank’s 2% target rate, the Riksbank still projects CPIF inflation will pick up further, reaching 2% by the beginning of the new year. Meanwhile, CPIF inflation excluding energy prices quickened to 1.8% year-over-year, also beating consensus estimates (+1.7%). The uptick in November’s inflation data is consistent with our expectation that the central bank will raise its repo rate 25 bps to 0.00% at the December 19 meeting.

Global Outlook

Bank of England Policy Decision • Thursday

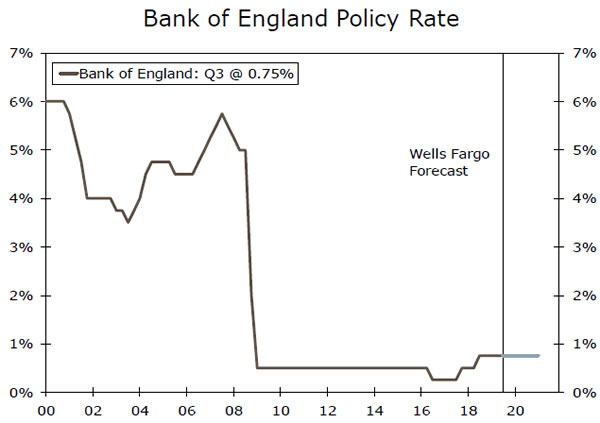

The Bank of England (BoE) announces its latest monetary policy decision next week and is widely expected to hold its bank rate steady at 0.75%. In its November announcement, the BoE held rates steady but two officials unexpectedly voted for a rate cut. The committee’s comments following the announcement suggest it is split on the next monetary policy action.

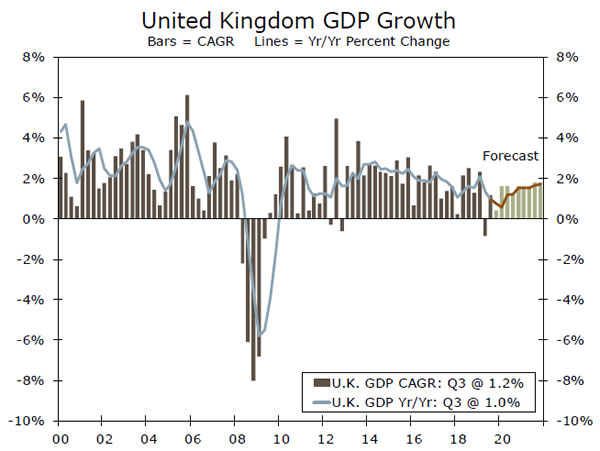

Price pressures eased in October, as U.K.’s headline CPI figure rose just 1.5% year-over-year, dipping to a near three-year low, while core CPI inflation held steady at 1.7% year-over-year, still below the central bank’s 2% target. Meanwhile, U.K. GDP stagnated in October, suggesting a slow start to the fourth quarter. Given the soft inflation and growth figures, combined with some uncertainties on longer-term E.U.-U.K. trade talks now that the Conservative party secured a majority in Parliament, we expect the BoE to remain on hold for the foreseeable future.

Previous: 0.75% Wells Fargo: 0.75% Consensus: 0.75%

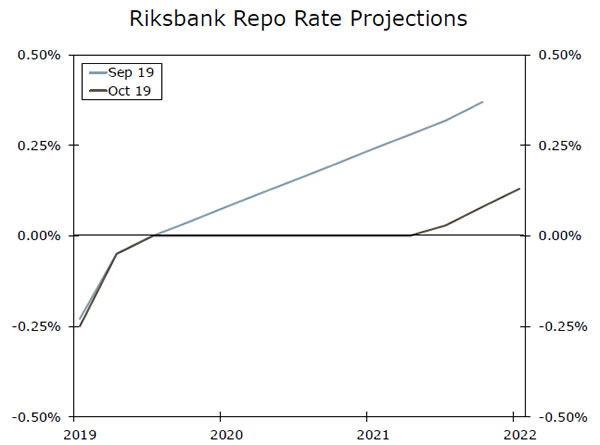

Riksbank Policy Decision • Thursday

The Riksbank caught markets off guard with its surprisingly hawkish announcement in October, still signaling a rate increase in December to bring the key policy rate to 0.00%. The monetary policy minutes suggested that all policymakers supported the forecast path of the repo rate, but one member expressed hesitation about raising rates by the end of the year. Policymakers also noted that the Swedish krona has been unexpectedly weak.

Over the past month, policymakers have highlighted that recent data have been largely in line with the central bank’s expectations, supporting its plan to end negative interest rates by year-end. Given these comments in addition to Sweden’s November inflation report printing better than expected, we think the Riksbank will raise the repo interest rate at its policy meeting next week, but then keep it unchanged for an extended period.

Previous: -0.25% Wells Fargo: 0.00% Consensus: 0.00%

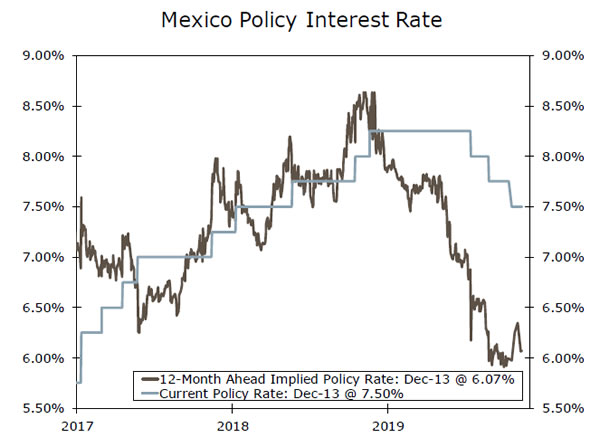

Banxico Policy Decision • Thursday

The Bank of Mexico opted to ease monetary policy at its last meeting in November, cutting its main policy rate another 25 bps to 7.50%. The accompanying policy statement was relatively dovish in our view, signaling additional rate cuts could be coming.

Mexico’s November CPI eased to 2.97% year-over-year, while the core CPI eased to 3.65% year-over-year, providing additional rationale for the central bank to lower interest rates further in the months ahead. As the Mexican economy remains subdued, in addition to the dovish signals from policymakers, we expect the central bank to cut rates another 25 bps at next week’s meeting, and continue the easing cycle into the new year. That said, however, we would not be surprised if policymakers moved forward with a 50 bps cut next week given how weak growth and inflation are at present. Currently, markets are pricing in 143 bps of additional easing over the next year by the Bank of Mexico.

Previous: 7.50% Wells Fargo: 7.25% Consensus: 7.25%

Point of View

Interest Rate Watch

Little Drama in FOMC Meeting

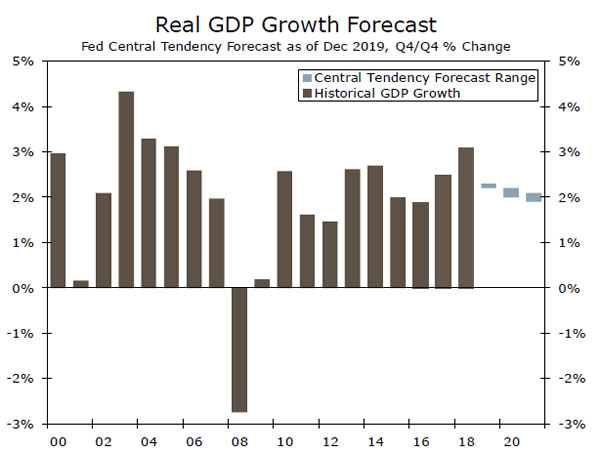

As universally expected, the FOMC decided unanimously at the policy meeting on December 11 to keep its target range for the fed funds rate unchanged at 1.50% to 1.75%. Furthermore, the statement that was released at the conclusion of the meeting was little changed from the last statement, suggesting that the FOMC’s assessment of the economy has remained essentially unchanged over the past six weeks.

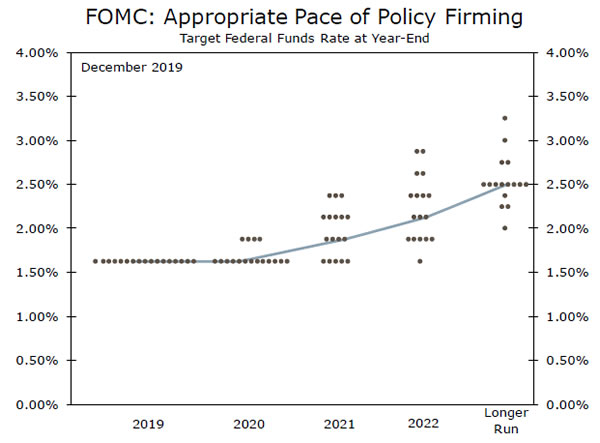

In its Summary of Economic Projections (SEP), the FOMC members’ median GDP growth forecast for 2020 is 2.0% (top chart), which is close to our own projection of 1.8%, and our inflation forecasts are very similar as well. The “dot plot,” which plots individual members’ forecasts of the fed funds rate, shows that most committee members believe the most likely outcome will be to keep the fed funds rate unchanged through the end of next year with only one 25 bps rate hike in 2021 (middle chart).

Our currently published forecast looks for the FOMC to cut rates another 25 bps in the first quarter of 2020. This view was predicated on our assumption, which we had maintained for some time, that a meaningful trade deal would continue to elude U.S and Chinese negotiators. Since financial markets appeared to be priced in for a deal, if a deal was not reached we expected markets would weaken and credit spreads would widen. In that event, in our view, the FOMC would want to offset some of this financial tightening by guiding shortterm interest rates lower.

This morning’s announcement from the Office of the U.S. Trade Representative disclosed that the 15% tariff on approximately $156B of imports from China will not go into effect this Sunday, and the 15% tariff on about $120B will be reduced to 7.5%. With the deal now officially reached, the case for further monetary easing early next year is not as compelling.

Whether or not the FOMC cuts rates 25 bps early next year is not overly important, in our view. Rather, we think the point to stress about our forecast is our view, which is also reflected in the FOMC’s dot plot, that rates likely will remain low for an extended period of time.

Credit Market Insights

Financial Health of Household Sector

The financial health of the U.S. household sector remains strong. On Thursday, the Federal Reserve Board released its Q3 update of the Financial Accounts of the United States. The extensive report covers the balance sheets of households & nonprofits, businesses and the government.

Total net worth of U.S. households notched another gain in the third quarter, up $573.6 billion. Discounting the fourth quarter of last year, when a selloff in equity markets weighed on net worth, Q3 marked the smallest gain since Q3-2015. Liabilities rose at a faster rate than assets in the quarter, but not to a worrying degree. Household liabilities continue to grow at a moderate rate, but as a share of total assets are at their lowest level since the mid-1980s. Unfortunately, we have not yet received an updated read on the Distributional Financial Accounts, which provide the distribution of U.S. household wealth. Data through the second quarter, however, suggest the gain in net worth has been seen across the income spectrum, and as we have written recently, is helping provide those most hurt by the Great Recession the necessary financial cushion to withstand the next downturn.

Healthy balance sheets paired with rising wages should continue to support consumer spending. Similarly, while low interest rates may increasingly entice consumers to borrow, lower financing costs will likely free up some cash-flow which can ultimately be a tailwind to consumer spending.

Topic of the Week

A Monetary Giant

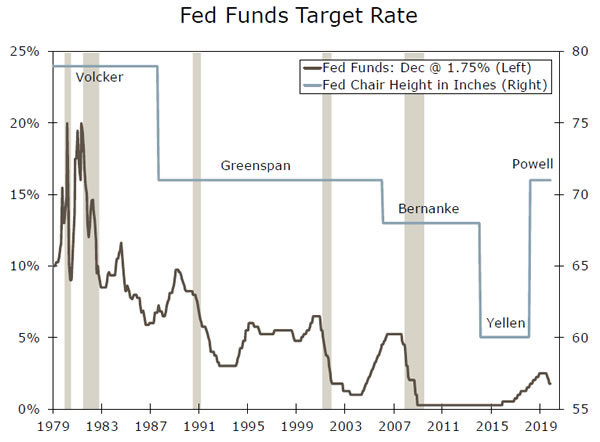

Paul Volcker, who as Chairman of the Federal Reserve from 1979 to 1987 broke the back of inflation in the United States and brought about a new era of monetary policymaking, passed away on Sunday at 92.

Recognizing the pernicious effects of spiraling inflation on the economy, Volcker took unprecedented and immediate action just two months after taking the helm at the Eccles Building by calling a surprise Saturday press conference where he announced a new, more aggressive restriction of money supply growth in order to rein in prices.

In a little more than a year, Volcker’s Fed allowed the fed funds rate to go from around 10% to nearly 20%, or 1,000 bps. The results were swift. The year-over-year rate of CPI inflation peaked in March 1980 at 14.8%, but fell below 3% by 1983. There were significant costs, however. By January 1980, the United States had fallen into a sharp recession as the surge in interest rates curtailed the flow of money through the economy. Volcker was harangued by Democrats, Republicans and the media, but his policy consistency ultimately killed runaway inflation and ushered in an era of relative macroeconomic stability.

Today, interest and inflation rates in the double digits seem as antiquated as smoking a cigar while testifying to the Senate Banking Committee. Indeed, current Fed Chair Powell has had to contend with inflation that is too low. Meanwhile, interest rates, or the compensation that bond investors demand for the risk of inflation, have steadily declined for the past 40 years, as inflation and the volatility of inflation have both dramatically subsided.

We have less benefit of hindsight regarding the efficacy of the Volcker Rule, the post-crisis financial reform that Volcker proposed to the Obama administration, but current Fed officials regularly attest to the strength of the banking system. Where Volcker’s legacy is clearer: sub- 2% inflation has allowed Powell to put more emphasis on the growth side of Fed’s dual mandate, and deliver 75 bps of insurance cuts this year to counteract trade uncertainty without much fear of a breakout in inflation.

{kind=link}