Markets will get back into full gear next week as traders return from their festive breaks and the economic data start rolling again. The spotlight will be on the nonfarm payrolls report in the United States, but key indicators out of the Eurozone, China, Canada and Japan should also attract attention. With the trade optimism setting the market mood at the end of 2019 and the start of 2020, there’s a risk the incoming data may not support the brightening picture that many investors have embraced lately, setting the stage for a possible correction.

Aussie eyes domestic and Chinese data as rally loses steam

The Australian dollar managed to reverse its huge losses from the third quarter to end 2019 only slightly in the red against its US counterpart. But the impressive rally since October is already showing signs of exhaustion and if next week’s data prove uninspiring, the sell-off could deepen.

Looking at the domestic releases, they will consist of the AIG manufacturing index for December on Monday, November building approvals on Wednesday, the trade balance on Thursday, and retail sales numbers for November on Friday.

Australia’s reliance on China for its exports means aussie traders will also be watching Chinese price gauges due on Thursday. The consumer price index (CPI) in China jumped to the highest in eight years in November but markets largely ignored the spike as it was mainly down to soaring pork prices and a bigger concern is the continued weakness in producer prices. The producer price index (PPI) edged up only marginally in November to -1.4% year-on-year, reflecting weak demand for factory goods.

The US and China agreed a ‘phase one’ trade deal in December and any pickup in the PPI in the coming months could be attributed to this, though it would be too soon for it to impact the December reading.

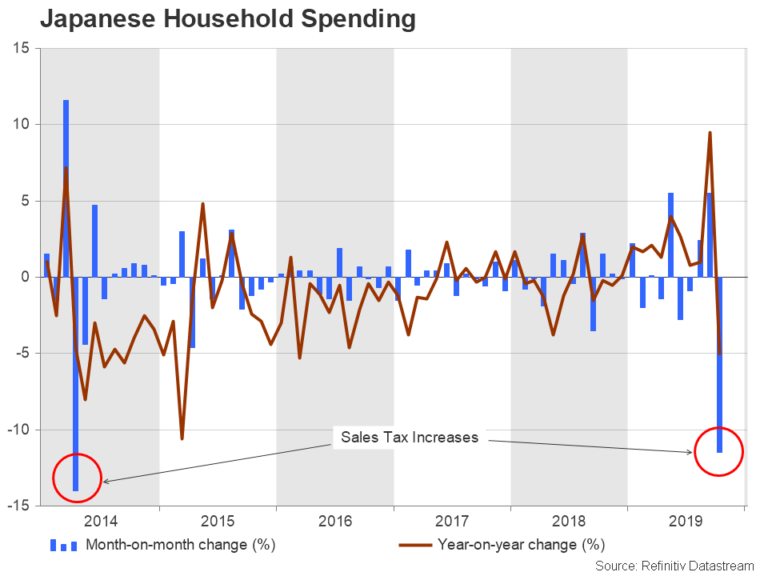

A rebound in Japanese consumption?

Consumer spending slumped in Japan in October as the sales tax went up from 8% to 10%. The drop in household spending was almost as bad as in 2014 when the sales tax was last hiked, triggering a recession. However, although the broader impact on the economy is not anticipated to be as severe as it was in 2014, growth remains under pressure from the trade frictions that have had a devastating effect on manufacturers globally, particularly the car industry.

Hence, it will be crucial for consumption to bounce back quickly to prevent Japan’s economy from slipping into recession. The household spending numbers for November are due on Friday, and before that, the latest wage growth figures will be watched on Wednesday.

But as is typical for Japanese data, the reaction in the yen is expected to be limited, as until the Bank of Japan signals it is ready to beef up its already massive stimulus program, nothing will change in terms of the outlook for monetary policy.

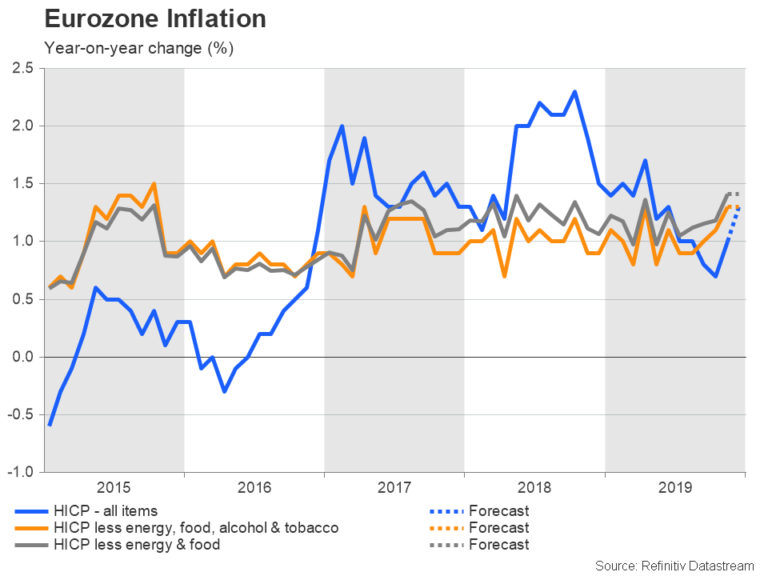

Eurozone inflation to tick higher

The euro closed 2019 on a more positive tone than how it began and despite ending the year nowhere year its starting point, there are signs that the long drawn out downtrend has finally bottomed out. Easing trade tensions, which in turn have put a dent in the US dollar, are one of the factors bolstering the single currency but there have also been some tepid signs of green shoots in the Eurozone economy.

Next week’s data could further add to the evidence of an improving growth picture starting with the final services PMI readings for December and the sentix index for January on Monday. There will be more business surveys on Wednesday with the economic sentiment indicator, which is forecast to have edged up to 101.5 in December. The other important releases are November retail sales and the flash inflation estimates for December on Tuesday.

There was some good news for the European Central Bank last month when both the headline and underlying measures of inflation headed higher. The headline rate is forecast to have risen further, increasing from 1.0% to 1.3% year-on-year in December, but the two core rates are expected to have stayed unchanged.

Also coming under investors’ radar will be industrial data out of Germany. Industrial orders and production figures are due on Wednesday and Thursday, respectively. Both are forecast to show positive growth for November after contracting in October. Any disappointment in these numbers would question whether a recovery is really underway in Europe’s largest economy and possibly undermine the euro’s latest attempt at a rebound.

Last but not least, the ECB will publish the account of its December policy meeting on Thursday.

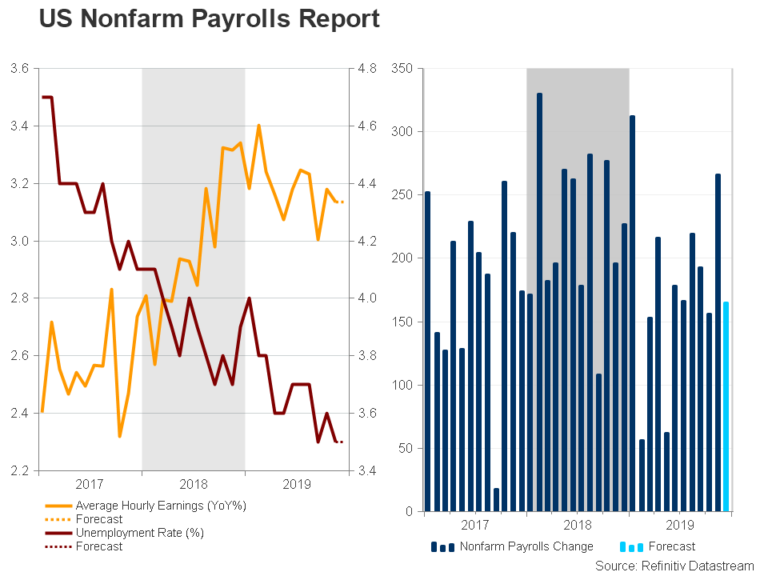

First NFP report of 2020: much to be excited about?

With the US-China trade deal now (temporarily) out of the way, the focus in early 2020 will be on whether the US economy will be able to regain some momentum or if it will be stuck in the slow lane. One thing’s for certain, there will be no shortage of data next week to give investors a fresh glimpse into the health of the economy.

First up are the trade balance and factory orders on Tuesday, both for November, as well as the ISM non-manufacturing PMI. After two consecutive months of declines, factory orders rose by 0.3% m/m in October. They are forecast to maintain a positive trend in November to rise by 0.2%. There could be more upbeat numbers from the ISM non-manufacturing composite. The closely watched barometer for services sentiment and activity has been on a downpath since the end of 2018 but may now finally be stabilizing. The index is expected to have increased from 53.9 to 54.5 in December.

Moving to the highlight of the week, the nonfarms payrolls report for December will hit the markets on Friday, with the headline figure projected to come in at 165k. This would represent a slowdown from November’s 266k print, which had been boosted by one-off factors such as the end of the General Motors strike. The unemployment rate is forecast to have remained at 3.5% and average hourly earnings are also anticipated to have held steady at 3.1% y/y.

Better-than-expected numbers are unlikely to provide much of a boost to the dollar as the Federal Reserve has made it clear it will not be in a rush to raise interest rates if the data starts to improve. On the other hand, any negative surprises could deepen the downside pressure facing the greenback currently, having ended 2019 on the backfoot.

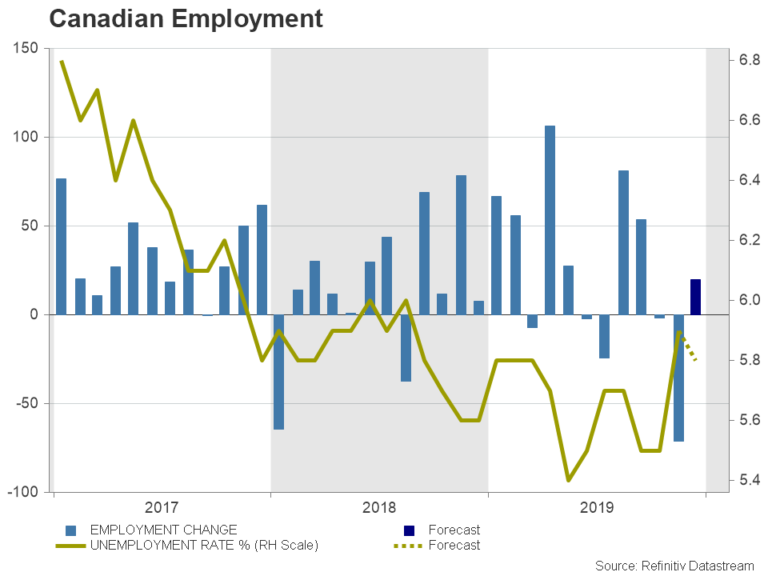

Jobs report in focus in Canada too

While the late 2019 risk rally has been bruising for the US dollar, it’s been a boon for commodity-linked currencies such as the Canadian dollar. The combination of rising risk appetite and higher oil prices have propelled the loonie to 14-month highs and those gains could continue next week if the December employment report, due on Friday, doesn’t disappoint. The Canadian economy is forecast to have added 20k jobs in December, which would be a big improvement on the shockingly hefty 71.2 jobs lost in the prior month.

{kind=link}