U.S. Review

Coronavirus Won’t Move the Fed

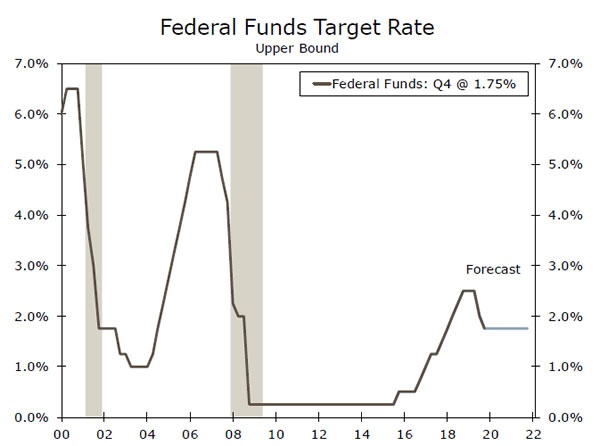

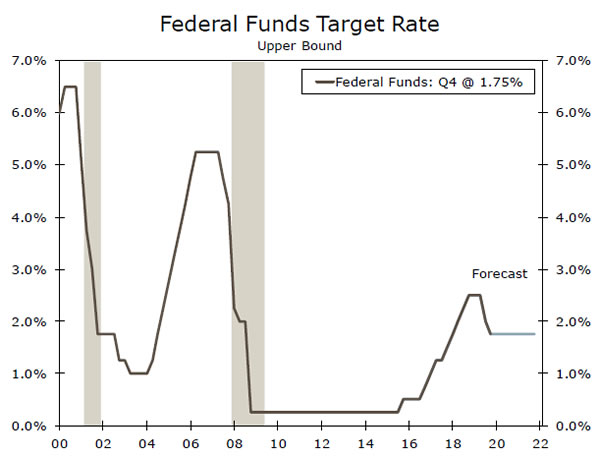

- Minutes from the January 28-29 FOMC meeting indicate the coronavirus will not push the Fed to cut interest rates, and for the most part housing and manufacturing survey data this week supported that view.

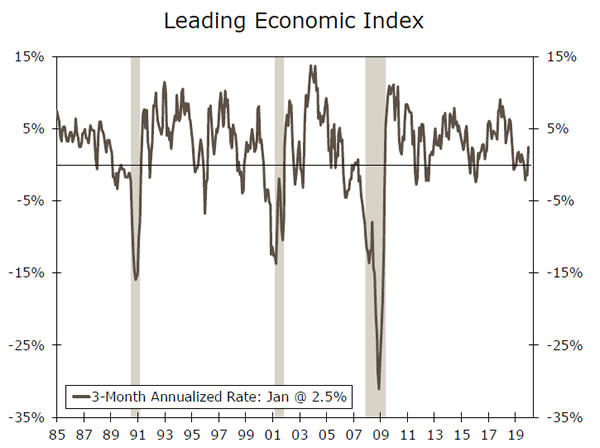

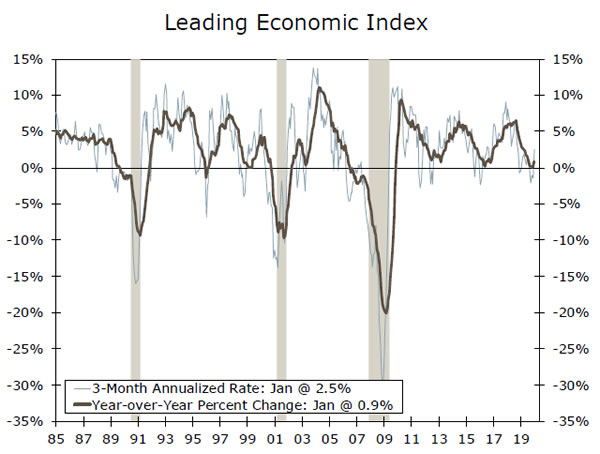

- The Leading Economic Index jumped 0.8% to an all-time high—easing some concerns generated by its dip into negative year-over-year territory the prior month—while the Philly Fed Index exceeded expectations by jumping to 36.7 and the Empire Manufacturing Survey beat consensus by rising to 12.9.

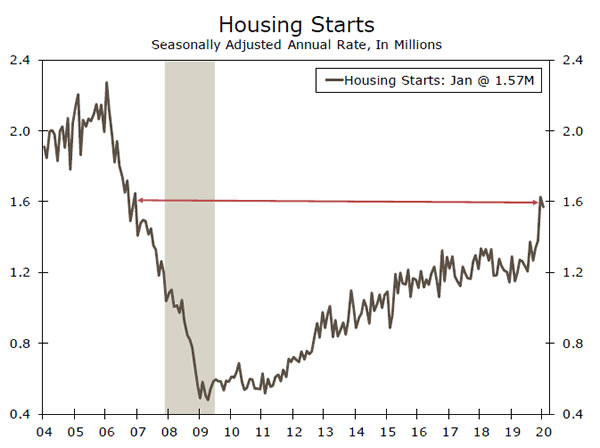

- Housing, meanwhile, continues to exceed expectations. December and January were the two strongest months for housing starts since 2006.

Coronavirus Won’t Move the Fed

Minutes from the January 28-29 FOMC meeting indicate the coronavirus will not push the Fed to cut interest rates. Positive housing and manufacturing survey data this week supported that view.

While trade tensions have receded markedly in recent months, the coronavirus has taken its place as the latest source of uncertainty plaguing businesses and investors. The outbreak has certainly worsened since the meeting—there are now around 76,000 cases in China, 208 in South Korea, 109 in Japan and 15 in the United States. The eight mentions of “coronavirus” in the minutes suggest the Fed, with its goal of sustaining the economic expansion top of mind, was closely monitoring even in late January. Despite the outbreak, the committee viewed the “distribution of risks to the outlook for economic activity as more favorable than at the previous meeting,” while also noting downside risks “remained prominent.” Its conclusion, however, that the virus has yet to cross the “material” threshold warranting a reassessment of the need for additional accommodation is disputed by the bond market. Market positioning now implies close to two cuts in the fed funds rate this year, while the 10-year to 3-month yield curve is inverted. Yet, markets can be fickle. We expect the Fed will remain on hold, a view which has been echoed by post-meeting Fed speakers, including Chair Powell during his congressional testimony last week.

Further supporting this view were the latest forward-looking indicators. The Leading Economic Index (LEI) jumped 0.8% to an all-time high—easing some concerns generated by its dip into negative year-over-year territory the prior month—while the Philly Fed Index exceeded expectations by jumping to 36.7 and the Empire Manufacturing Survey beat consensus by rising to 12.9. For more on the LEI, please see Topic of the Week.

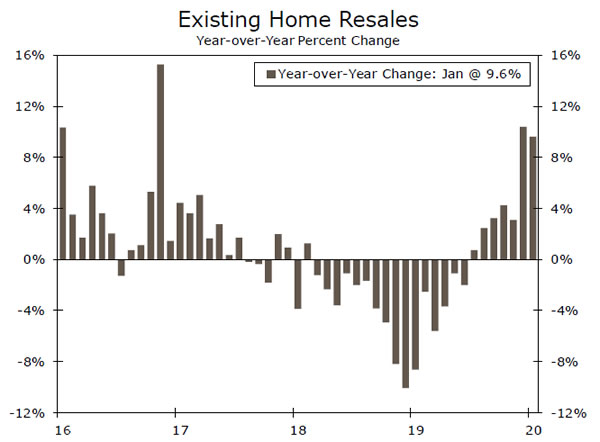

Housing, meanwhile, continues to exceed expectations. Housing starts fell modestly in January, but only because of the incredibly high pace registered in December. Starts in both months were boosted by some of the warmest winter weather on record. Despite the fall, January’s pace was 21% above the total level of starts for 2019, meaning that if housing construction maintains its current pace, we will see some incredibly strong year-over-year numbers in 2020. As normal weather returns, and we expect to see payback this spring from December and January, which were the two strongest housing starts months since 2006. Still, the underlying trend remains very strong—low mortgage rates have improved buying conditions, and consumers increasingly report now is a good time to buy. Sensing this, builders have turned very optimistic, with the NAHB index, a measure of single-family homebuilder sentiment, hanging near a 20-year high in February. Existing home sales fell 1.3% in January, but are up nicely over the year.

The FOMC minutes also highlighted some long-term shifts in its thinking. The committee discussed maintaining an inflation target range, but “most” members had concerns that it could be misinterpreted as the Fed being comfortable with inflation below 2%. It plans to continue these deliberations at coming meetings as its part of its ongoing monetary policy review.

U.S. Outlook

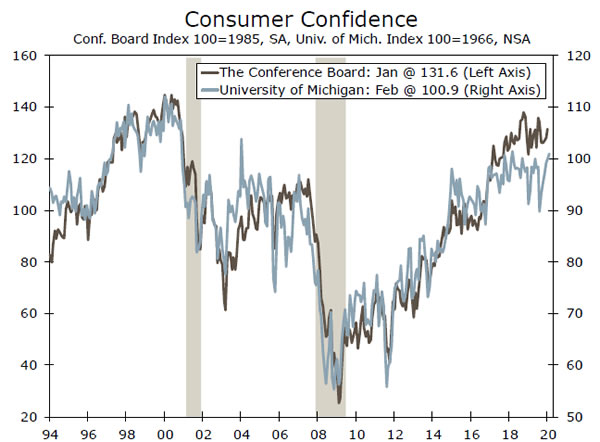

Consumer Confidence • Tuesday

The Conference Board’s consumer confidence index should remain elevated in February. Jobless claims remain low and wages are slowly but steadily rising. Lower gasoline prices, in the most simple of terms, mean more money in consumers’ pockets. Moreover, the stock market continues to climb to all-time highs despite the coronavirus consuming the attention of financial market participants in recent weeks. While the virus presents a risk, we do not expect it to meaningfully weigh on confidence in February.

The preliminary read for February consumer sentiment measured by the University of Michigan showed a 1.1 point rise. The two measures don’t necessarily move together from month-to-month, but they do tend to move in a similar trajectory. We will get the final read for sentiment on Friday, which we expect to be little changed from the preliminary estimate.

Previous: 131.6 Wells Fargo: 132.7 Consensus: 132.1 (Conference Board Index)

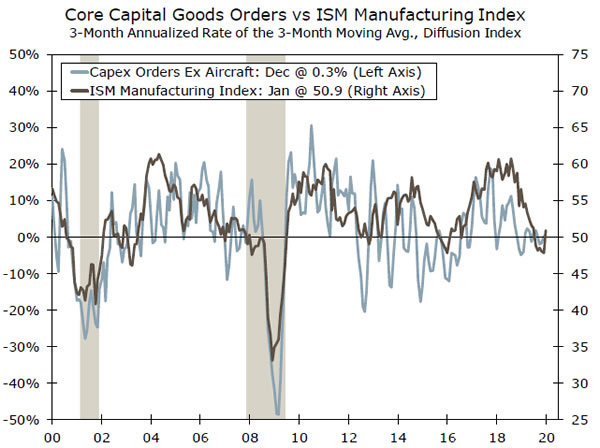

Durable Goods Orders • Thursday

Durable goods orders will likely show a decline in January. For starters, we’ll be looking for some payback from defense orders, which surged 90% in December. Further, we expect civilian aircraft to continue to drag on overall orders, amid Boeing’s ongoing issues. Boeing announced it had no new orders in January after just three new orders in December, when nondefense aircraft orders fell 75%. It halted production of its 737 MAX at the start of January, which may have weighed on orders in the month, but orders of the aircraft have been scarce since it was grounded in March.

Outside of aircraft, private core capital goods orders may be due for some pick-up. The rebound in the ISM manufacturing index, as well as some easing in trade policy uncertainty with the Phase I deal signed, suggest there is some upside for core capital goods orders, though we expect the pace to remain modest in the quarters ahead.

Previous: 2.4% Wells Fargo: -0.8% Consensus: -1.5% (Month-over-Month)

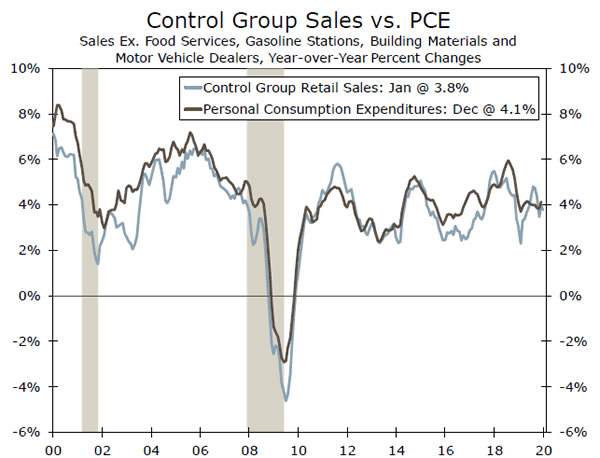

Personal Income & Spending • Friday

We expect consumers spent at a solid pace in January. Consumer confidence remained elevated and already reported data from retailers show goods sales continued to rise at a steady rate. Control group retail sales, however, which exclude volatile components and is utilized in the computation of the BEA’s personal spending estimates, were flat in January, which suggests some downside risk to our estimate of a 0.3% gain. Still, with about two-thirds of consumer spending devoted to services—which is not included in retail sales—we are optimistic for January spending.

As spending has continued, personal income growth has faltered, causing a slight pull-back in the personal saving rate. We expect to see a 0.3% gain in personal income, which should alleviate some of the recent drawdown in savings. Still, at 7.6% in December, the saving rate remains at an elevated level for this stage of the expansion and further exemplifies the health of consumer balance sheets.

Previous: 0.2% & 0.3% Wells Fargo: 0.3% & 0.3% Consensus: 0.3 & 0.3% (Month-over-Month)

Global Review

Japan Underperforms Expectations; Coronavirus Update

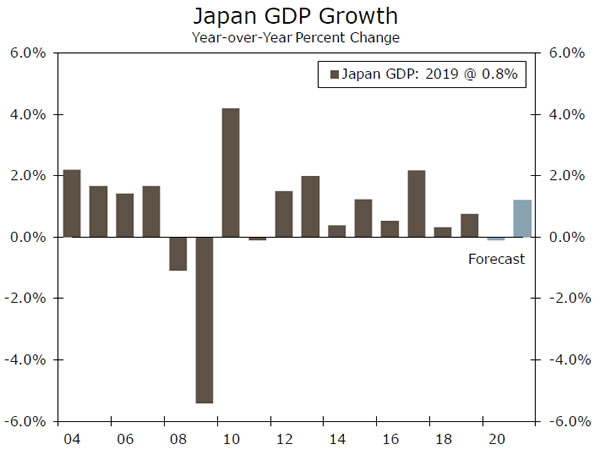

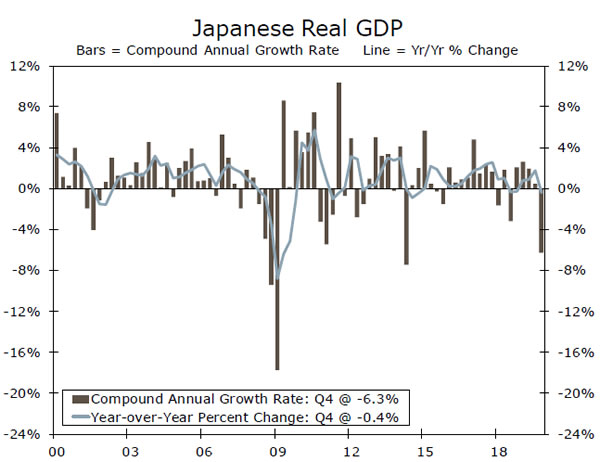

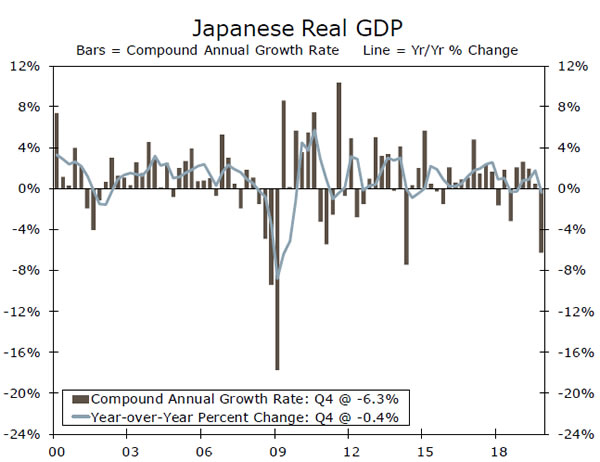

- This week’s Japanese GDP data indicated a significant slowdown in the Japanese economy to close out 2019. Q4 data revealed Japan’s economy contracted 6.3% quarter-overquarter annualized, while other measures of activity contracted notably as well. As a result, we have downgraded our 2020 GDP forecast and now expect the Japanese economy to contract in 2020.

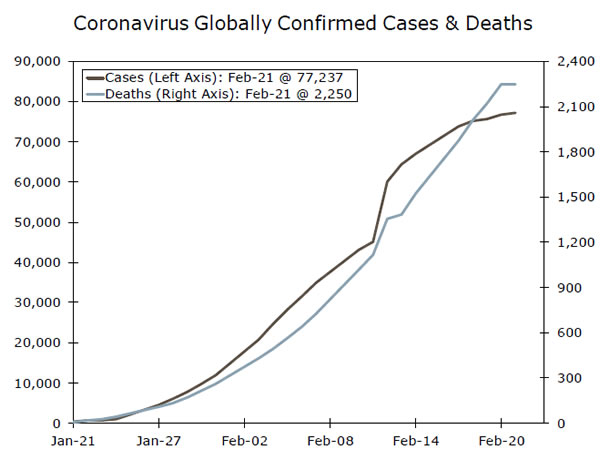

- The coronavirus continues to linger over financial markets, with the most recent update of over 77,000 confirmed cases and over 2,200 fatalities around the world. We still expect the virus to cause additional disruptions to China’s economy.

Japanese Economy Significantly Underperforms

Early this week, data from Japan indicated the economy is likely not as healthy as markets previously assumed. In that context, recent economic data have been disappointing and suggest the economy suffered much more than expected as a result of the tax hike in October. Data this week showed that Japanese real GDP contracted at a 6.3% quarter-over-quarter annualized pace in Q4-2019, much worse than expected, and the sharpest decline since the last consumption tax hike in April 2014. Digging a little deeper into the data, we looked at real private final demand, a better underlying measure of growth that captures private sector consumption and investment adjusted for inventory changes. That measure of output fell at an even more alarming 11.7% quarterover- quarter annualized pace, nearly double the decline in total GDP. While that decline is not as large as the drop in private final demand after the last tax hike in 2014, we also did not see the same firming of growth in the quarters leading into the 2019 tax hike.

We should also add the important caveat that Japan was affected by a devastating typhoon in October as well, which almost certainly added downward pressure to the economy in Q4. Moreover, December data showed another drop in overall Japanese consumption, a sign the economy may not have rebounded as much as expected toward the end of the quarter as the tax and typhoon impact faded. Early evidence suggests Japan’s economy may face challenges again in the current quarter. Japanese exports to China represent around 3% of total Japanese GDP, compared to a similar figure from the U.S. of just 0.5% of GDP, suggesting the Japanese economy could be more significantly affected by the coronavirus outbreak in China. We think Japan may just narrowly dodge recession in Q1, but the economy will probably be close to stagnating during the quarter. Accordingly, we have updated our forecast to reflect our view that we believe Japanese real GDP will decline 0.1% during full-year 2020, a significant downgrade from our prior estimate of positive growth of 0.4%. Our 2021 forecast is now for 1.2% growth, boosted by more favorable base effects from 2020.

Quick Coronavirus Update

The coronavirus continues to influence investor sentiment, with current news flow pulling market participants in multiple directions. As of the most recent update, it seems as if confirmed cases of the virus have started to taper off, especially within China. This news created a bit more positive sentiment within markets, and saw equity markets initially rally as virus concerns subsided. However, later in the week, we received confirmed cases and fatalities in countries outside of China. For instance, this week alone we saw two more confirmed fatalities in Japan, while Korea experienced its first death as a result of the virus. Amidst this news, global equity markets sold-off and other risk sensitive assets came under pressure. As of now, over 77,000 confirmed cases have been reported, while the virus has claimed over 2,200 lives. As a reminder, we believe the virus will have an impact on China’s economy and forecast a notable slowdown to growth in Q1 of this year, while also downgraded our full year 2020 GDP forecast as a result of the coronavirus.

Global Outlook

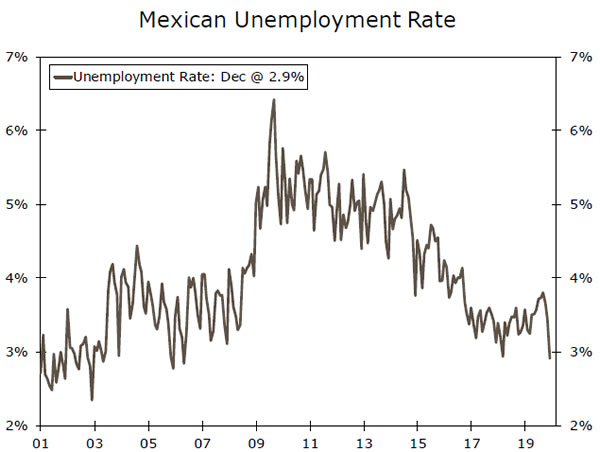

Mexico Unemployment • Thursday

The Mexican economy has been under duress for almost two years, with the most recent GDP figures uninspiring. In fact, the Q4 GDP figures indicated the Mexican economy contracted to close out 2019, which resulted in the Mexican economy contracting for the entire year. In addition, inflation has been trending lower for some time now, providing the central bank a strong incentive and rationale to ease monetary policy rather aggressively. Despite the subdued nature of the Mexican economy, the labor market could be identified as one of the lowly bright spots as the unemployment rate has declined notably over the last few months. As of December, Mexico’s jobless rate stood at 2.91%, while the labor market participation rate has climbed higher. Looking ahead, there is a possibility the unemployment rate begins to tick higher as the economy struggles to gain traction, which in turn, could create yet another vulnerability in the Mexican economy.

Previous: 2.91%

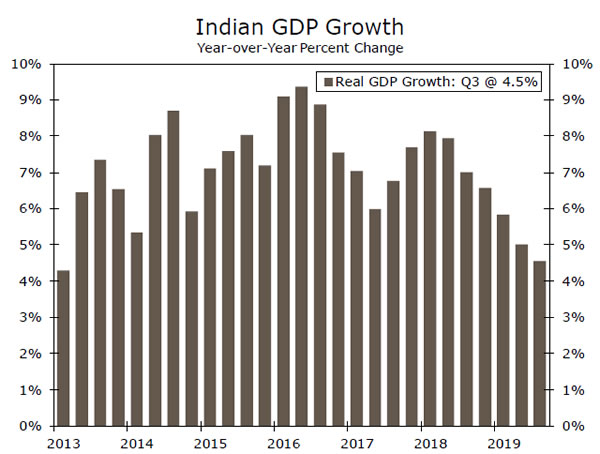

India GDP • Friday

One of the more notable decelerations within the global economy has taken place in India. Historically, India has had one of the fastest growing economies in the world expanding close to 7%; however, over the course of 2019 growth slowed significantly. In Q3, GDP growth softened to 4.5% year-over-year, while Q4 GDP set to be released next week is only expected to rise a modest 4.7%. There are a few reasons that likely explain the slowdown, the first being elevated political risk as it relates to decisions from the Modi administration. Controversial policies have slowed investment into India and business spending, while also raised geopolitical tensions with regional neighbors. In addition, India’s banking sector remains fragile, with multiple state-owned lenders in financial trouble and carrying high levels of non-performing loans on their balance sheets. A weak banking sector has limited the amount of new loans, and in turn, weighed on Indian consumers and the economy.

Previous: 4.5% Consensus: 4.7%

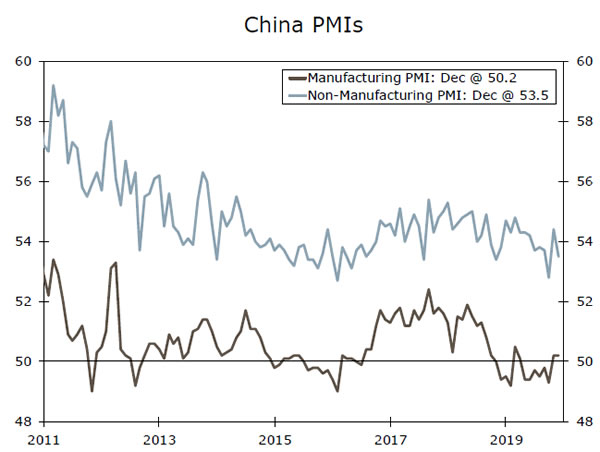

China Manufacturing PMI • Friday

Over the last two years or so, the Chinese economy has faced some serious headwinds. Trade tensions with the United States likely caused some disruption to the economy, while the recent coronavirus originating in Wuhan, China is also expected to have an impact on Chinese economic activity. The manufacturing sector is perhaps the sector to be the most effected as a result of these double headwinds. Increased tariffs have elevated production costs, while the coronavirus has resulted in many manufacturing plants temporary closing in an effort to contain the virus. The Phase I trade deal has improved sentiment towards the manufacturing sector to start the year and has kept the manufacturing PMI in expansion territory. With the coronavirus continuing to result in business closures throughout the country, however, it is likely manufacturing sentiment will soften in February. In fact, we would expect the manufacturing PMI to drop into contraction territory.

Previous: 50.0 Consensus: 47.4

Point of View

Interest Rate Watch

Fed Worried About Stock Market?

The minutes of the policy meeting that the Federal Open Market Committee (FOMC) held on January 28-29 were released this week. In light of the previously-released brief statement and Chairman Powell’s subsequent testimony to Congress, the minutes contained few surprises. The FOMC’s mantra, which was repeated in the minutes, is that the current stance of monetary policy “is likely to remain appropriate for a time.” In short, the Fed is likely to remain on hold for the foreseeable future, which is our view as well (top chart).

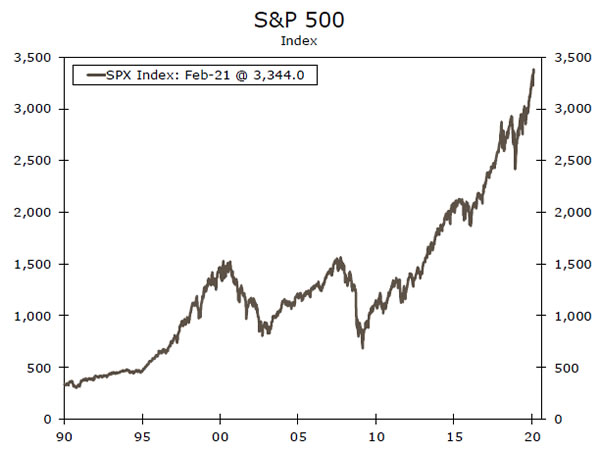

That said, there were two topics that caught our attention. First, most American stock market indices had risen to all-time highs prior to the FOMC meeting (middle chart), and corporate bond spreads had remained quite tight. These developments did not escape the attention of the FOMC. Specifically, there was discussion about how persistently low interest rates may lead to “financial system vulnerabilities, including through increased borrowing, financial leverage, and valuation pressures.” “Many” committee members acknowledged that monetary policy should not be systematically adjusted because of developments in financial markets. Knowledge of their interactions is simply too imprecise to calibrate policy changes. If there is a role for policy, it lies in the macroprudential/ supervisory realm. However, the tone of the minutes suggest at least some members of the FOMC are becoming a bit concerned about some vulnerabilities they perceive may be building up in the financial system.

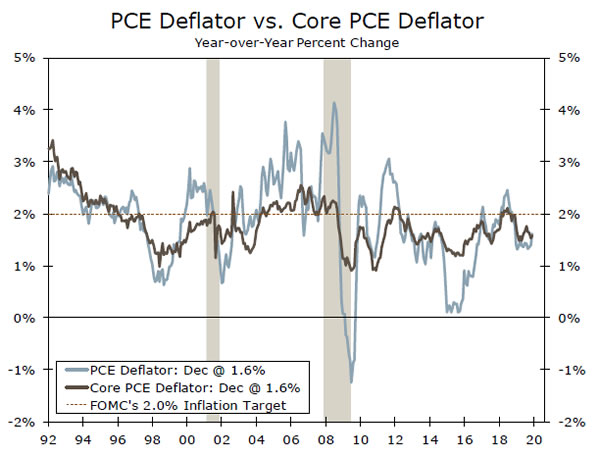

The other topic of note was the strategy review that has been underway at the Fed in recent months. The Fed has had a two percent inflation objective for the past few years, but it has generally undershot this objective (bottom chart). Persistently undershooting the target could depress inflation expectations, thereby making it more difficult to lift inflation back up toward 2 percent. Consequently, the Fed may eventually allow inflation to exceed 2 percent for some time. No decisions have yet to be made. The FOMC anticipates that its strategy review will be completed around mid-year.

Credit Market Insights

Auto Loans Past Their Prime?

Mortgage finances look stellar, with delinquency rates and debt to disposable income near their lowest levels since at least 2003. Similar metrics for other forms of consumer debt, however, have provided some cause for concern.

Delinquency rates for auto loans, for instance, have been rising fairly consistently over the past three years. The New York Fed’s Q4 Household Debt and Credit report showed the percent of balances 90+ days delinquent reached its highest level since the third quarter of 2011, when the economy was recovering from the Great Recession. This may be concerning if it reflects a broad deterioration in credit quality among households, given auto loans have been a major driver of debt growth over the last decade. Auto loans have accounted for nearly a quarter of household debt growth since Q3-2011. The majority of this auto debt growth, however, has been driven by prime bowers. The share of new loans and leases going to subprime borrowers remains below its long term average. By contrast, the rise in non-current balances has been driven largely by subprime borrowers. This concentration of delinquencies suggests the rise may reflect changes in lending practices at the lower end of the credit spectrum rather than deteriorating credit quality among U.S. households. Rising delinquencies have led to tighter auto lending standards at banks, as evidenced by the Senior Loan Officer Opinion survey, but it is unclear if the same can be said for auto financing companies, which make up a disproportionate share of subprime auto lending.

Topic of the Week

What LEIs Ahead?

The Leading Economic Index (LEI) rebounded in January with a 0.8% rise, which marked the largest monthly increase in more than two years and brought the index to a new high. Further, revisions to December— which had previously shown the first negative year-overyear growth rate since 2009—now show a 0.09% gain. This likely alleviated some concern of a downturn, which has typically been proceeded by a negative year-over-year reading in the index (top chart). Still, the LEI has undeniably lost momentum over the past year.

We are not in the business of making excuses for data and the LEI is certainly suggesting a slowdown in growth. The LEI overweights the manufacturing sector, however, with more than half of the index derived from it, and a decline in manufacturing does not weigh on the broader economy the way it did a generation ago.

In the past year for example, manufacturing faltered amid uncertainty surrounding trade policy and slower global growth, and the U.S. economy continued to expand. Such weakness, however, weighed disproportionately on the LEI. While manufacturing may not be as crucial as it once was, the sector still provides much of the cyclical impulse to the economy, which is why we too include manufacturing indicators in our recession models.

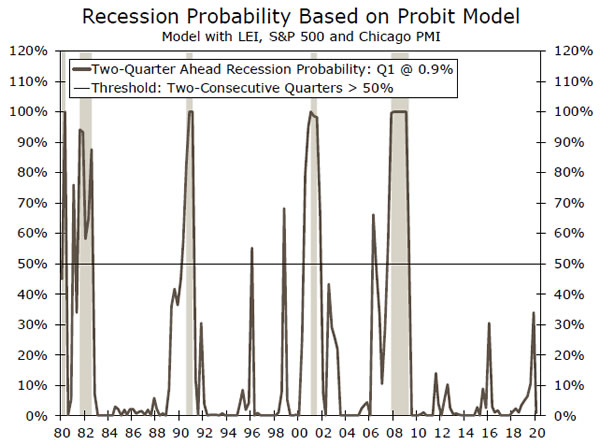

The 0.8% pop in the LEI last month brought our preferred recession probability models down to roughly a 1% probability of recession in the next six months in Q1. That is compared to about a 34% probability in Q4, which was the highest reading since the Great Recession (bottom chart). The lower probability projection in Q1, however, assumes we maintain our current position for the next couple of months, which may be difficult if disruptions from the coronavirus emanating out of China spill over into the U.S. factory sector. That means if the manufacturing sector is adversely effected by the virus, we may again see our recession probability estimates trend higher in coming months.

{kind=link}