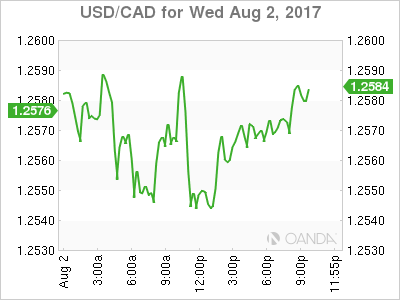

The Canadian dollar is trading lower against the US dollar on Wednesday. The loonie failed to capitalize on the US private payrolls slip and the rise in oil prices after a surprise gasoline demand surge. The Trump Administration has turned its focus on immigration and trade putting pressure on the Canadian currency.

The ADP private payrolls report disappointed in the early North American session by showing a gain of 178,000 jobs instead of the anticipated 187,000. The miss still leaves US employment with a solid gain, but creates some anxiety about the U.S. non farm payrolls (NFP) to be released on Friday. Investors and the U.S. Federal Reserve will be looking more closely at the wage growth numbers than the jobs added, as low inflation could force the central bank to leave interest rates unchanged for the remainder of the year.

The Canadian dollar is still one of the most solid currencies this year and got a boost form the Bank of Canada (BoC) as the central bank hiked rates in July after a short signalling campaign that started in mid June. The Canadian benchmark interest rate sit at 75 basis points with another 25 basis points hike expected in October. The monetary policy gap between the Fed and the BoC should not grow beyond that, but concerns about the Trump administration’s tough stance on trade could spell trouble for Canada ahead of the NAFTA renegotiation talks.

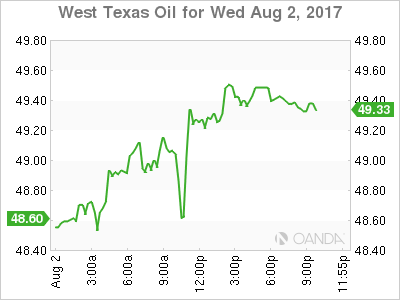

The USD/CAD rose 0.17 percent on Wednesday. The currency pair is trading at 1.2553 with the CAD losing ground to the USD ahead of employment data for both nations on Friday. The USD has climbed back from weekly lows although it is still struggling with non-commodity based currencies. Oil prices failed to lift the loonie against the USD as political risks once again took center stage.

The USD/CAD has gained 0.629 percent in the past five days. Political uncertainty has hurt the USD against most majors, but the CAD due to its close trade relationship has been under pressure. Three quarters of Canadian products are sold to the United States and while the Trump administration has failed to get traction on big policy reforms, trade is something where he could have a big impact. The problem for the market is trying to forecast which kind of impact it will be. With winners and losers on all three NAFTA nations the worst case scenario would be to scrap the deal, but that is still one of the possible outcomes if Trump’s rhetoric is to be believed.

NAFTA renegotiations talks will begin in two weeks. Mexico and the US have said they favour a quick resolution to avoid further politicizing the negotiations with upcoming elections in 2018.

Oil prices rose 1.202 percent in the last 24 hours. West Texas Intermediate is trading at $49.24 after the release of US weekly inventories showed a larger than expected growth in demand. The Energy Information Administration (EIA) reported a lower than forecasted drawdown of crude stocks. Weekly figures dropped 1.5 million barrels instead of the 3.2 million expected. The surprise came in gasoline demand with a record high 9.842 barrels. Given that appetite for gasoline and other energy products was seen as stagnant the rise in demand at the seasonal driving season boosted oil prices.

US producers are signalling in slowdown in rig counts citing profitability concerns and Saudi Arabia is rumoured to be limiting output to US destinations to impact oil pricing through US crude stocks weekly reports. The winners have been Canadian producers that are filing in to cover the gap in demand. The Organization of the Petroleum Exporting Countries (OPEC) and other major producers partnered in a production cut agreement last year which they have extended until March 2018.

Even with this deal diminishing the supply glut there were few signs of rising demand until this week’s EIA report. It remains to be seen if this was an outlier or a part of a larger trend.

Market events to watch this week:

Thursday, August 3

4:30 am GBP Services PMI

7:00 am GBP BOE Inflation Report

7:00 am GBP MPC Official Bank Rate Votes

7:00 am GBP Monetary Policy Summary

7:00 am GBP Official Bank Rate

7:30 am GBP BOE Gov Carney Speaks

8:30 am USD Unemployment Claims

10:00 am USD ISM Non-Manufacturing PMI

9:30 pm AUD RBA Monetary Policy Statement

9:30 pm AUD Retail Sales m/m

Friday, August 4

8:30 am CAD Employment Change

8:30 am CAD Trade Balance

8:30 am USD Average Hourly Earnings m/m

8:30 am USD Non-Farm Employment Change