U.S. Review

After Strong Initial Rebound, Momentum is Slowing

- The economic recovery continued into July, though the pace is slowing. The consumer has been a bright spot in the recovery so far, but with jobless benefits in flux and no clear path for the long-awaited stimulus bill, the support here could fade.

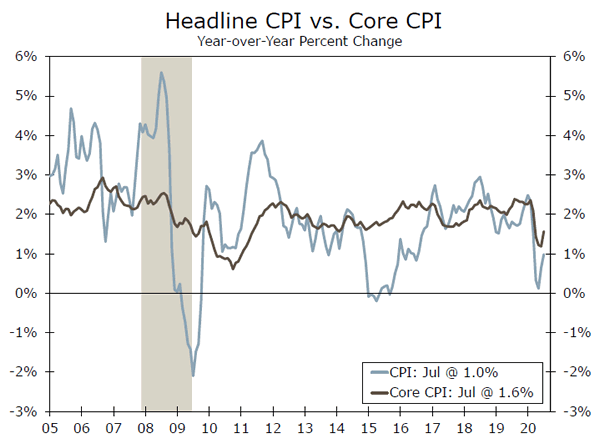

- Consumer prices picked up in July, but weak demand will likely keep a lid on inflation in coming months.

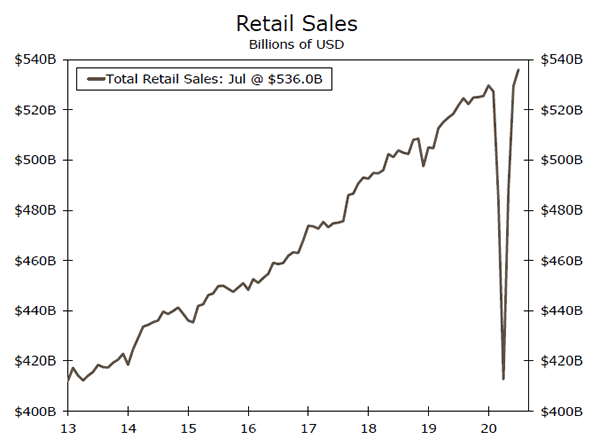

- While retail sales are back above their pre-virus peak, consumer caution was evident in the July data.

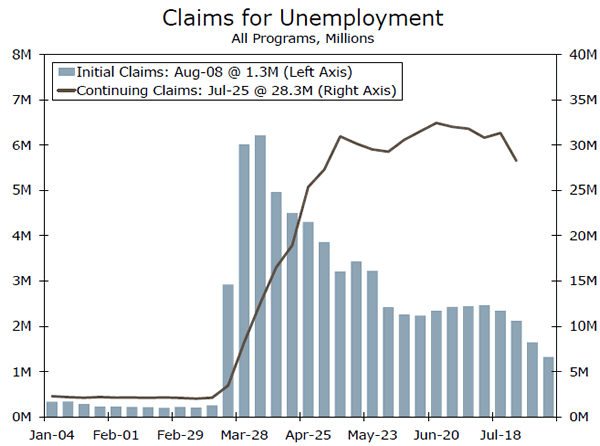

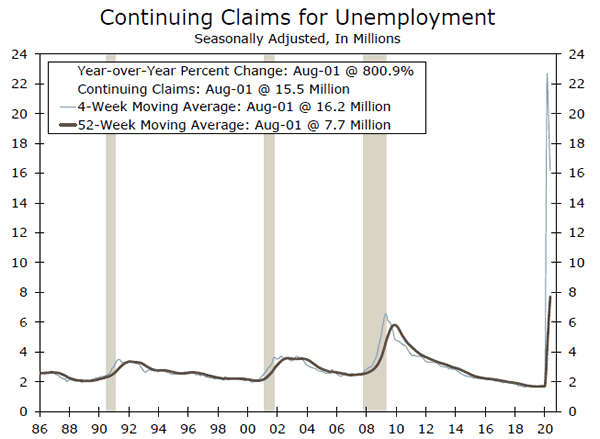

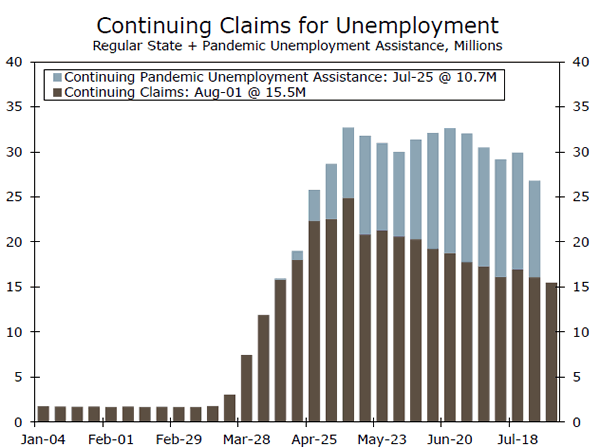

- Initial claims for unemployment came in below 1 million last week for the first time in 20 weeks. This is a marked improvement, but unemployment remains strikingly high.

After Strong Initial Rebound, Momentum is Slowing

Consumer prices jumped 0.6% in July. The rise reflects an unwinding of pandemic-induced price cuts this spring rather than the start of a sustained pickup in inflation. Weak demand is likely to keep a lid on inflation in coming months, as many households are unable or unwilling to spend amid the tenuous jobs situation, questions over the amount and duration of unemployment benefits and continuing risk of the virus.

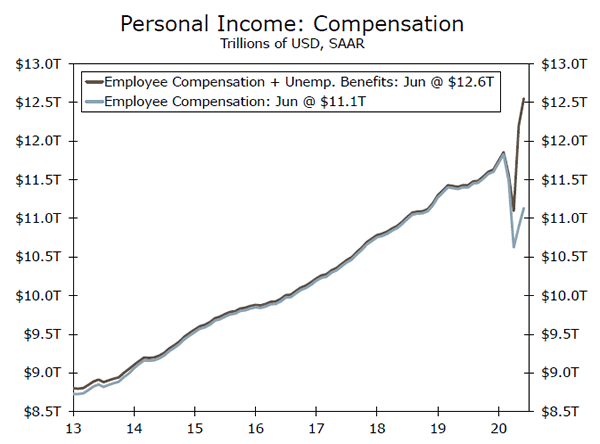

Consumer caution was evident in the July retail sales data, which showed sales up just 1.2% after surging in May and June. Still, retail sales have exhibited the definition of a V-shape recovery in recent months, as consumer demand for goods came roaring back as the economy began to re-open (top chart). But, with the surge being concentrated in recreational goods components, and services consumption still constrained by the virus, the spending rebound may be difficult to hold going forward. This is especially true when considering supplemental unemployment benefits expired at the end of July. The fiscal relief provided to households has more than offset the lost income from wages and salaries in recent months (middle chart). At a high level, this means once the economy re-opened, growth was able to pick up more than otherwise would be possible because consumer incomes did not fall as much as they typically would with the extensive job loss we’ve seen today. Even with President Trump ordering to reinstate the supplemental unemployment benefits at $400 per week, consumers may pull back on consumption in the near-term. The reduction in the benefits, and the expectation for it only to last for four to six weeks (see Topic of the Week for more detail) provides little clarity to unemployed workers and is concerning for the consumer outlook more broadly.

Despite the stand-still between Congress and the White House, another COVID-19 relief package is still possible and would be a source of upside risk to our U.S. outlook. The original stimulus was controversial, due to the fact that, supplemental benefits in 36 states caused unemployed workers to take home more in unemployment benefits on average than they earned when working. This may cause a near-term disincentive to work, but for many, getting a new job isn’t an option today—for every one job opening, there are three unemployed workers. That means much of the labor force remains idled, with wages, their biggest source of income, evaporated. Despite the expiration of supplemental benefits, 963,000 more unemployed workers filed an initial claim for unemployment benefits last week. This marked the first time in twenty weeks that there were less than one million new claims filed, but at just a stone’s throw away from a million, claims remain high (bottom chart) and suggest job growth could be more incremental in the months ahead. The expectation that consumer spending might take a hit due to a reduction in household stimulus could weigh on the broader economic recovery. Since inflation is not a huge worry at present, the Fed can focus on employment and try to prevent spillovers from the labor market. But, fiscal support is crucial for households and likely more effective at this stage rather than further monetary policy easing. Fed speak this week also emphasized the need for more fiscal support to ensure the economic recovery.

U.S. Outlook

Housing Starts • Tuesday

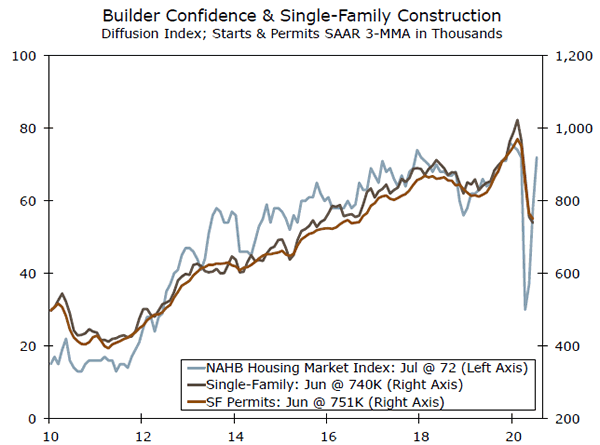

Housing starts picked up pace in June rising 17.3% to an annualized rate of 1,186K. We expect starts continued to improve in July, albeit at a less robust pace.

With buyers coming back, builders have felt confident to ramp up new construction. Single-family starts jumped 17.2% in June and permits rose 11.8%. Both numbers are likely headed higher, but builders are running into some bottlenecks that could limit the extent of gains. Lumber prices have soared to their highest level in years. Spot shortages of materials and labor have also emerged due to the pandemic and related public health measures. More significant headwinds threaten multifamily construction. Many cities are already facing a flood of supply after a cycle’s worth of elevated apartment construction. Meanwhile, demand appears to be waning, as the labor market remains weak and the country’s largest generation ages into its home-buying years.

Previous: 1,186K Wells Fargo: 1,212K Consensus: 1,230K (SAAR)

Initial Jobless Claims • Thursday

As noted in the U.S. Review, initial jobless claims dipped below one million, after 20 weeks in the seven figures. While there is not tremendous significance in passing the million mark, it illustrates continued progress in the labor market recovery which appeared under pressure at the end of July.

In normal times, next week’s report would be watched closely, as it shows the number of initial claims filed in the BLS survey week for the August employment report. Unfortunately, with more than 15 million individuals already claiming unemployment, the number of continuing claims, which lags a week, has become a more useful gauge for the monthly payroll figures. Next week’s report could, however, provide some indication of momentum (or lack thereof) in the labor market recovery. The consensus forecast shows a slight reversal of last week’s progress.

Previous: 963K Consensus: 990K

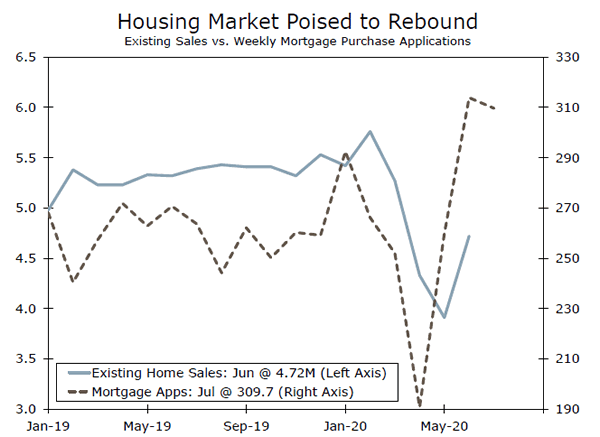

Existing Home Sales • Friday

COVID-19 pushed the spring selling season back, but homebuyers appear poised to make up for lost time. Existing home sales jumped 20.7% month-over-month in June to a 4.72 million-unit pace. While the level of sales remains depressed following a 32.1% cumulative drop over the prior three months, sales likely continued to rebound in July—we expect sales jumped 2.2% on the month. While this would be a deceleration from June, the housing market remains a rare point of strength in this young economic recovery. Even during the lockdown months, demand for homes appeared to remain robust. Online sales platforms reported increased inquiries and weekly mortgage purchase applications started turning around in late April. While shifting preferences and demographics should continue to support the housing market, the sector is not without its headwinds. Low inventories continue to exert upward pressure on prices, while increasing mortgage delinquency and use of forbearance has led to tighter lending standards.

Previous: 4.72M Wells Fargo: 5.38M Consensus: 5.40M (SAAR)

Global Review

Global Recovery Persists, Pace Moderates

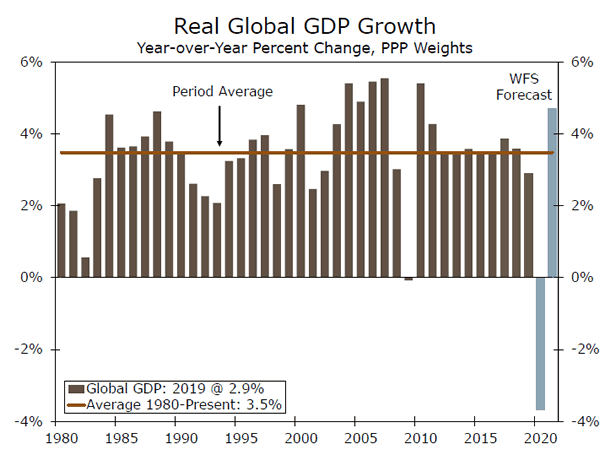

- After a challenging start to 2020 economies around the world are turning the corner, albeit it at varying speeds.

- Eurozone June industrial output showed a large monthly increase, similar to a large gain in retail sales, but Q2 employment fell sharply. In China, July industrial output growth was steady while the fall in retail sales lessened.

- Some economic regions are lagging. U.K. Q2 GDP fell more than 20% quarter-over-quarter, although activity started to improve by the end of Q2. Similarly, the rebound in activity in Mexico and Brazil remains relatively gradual so far.

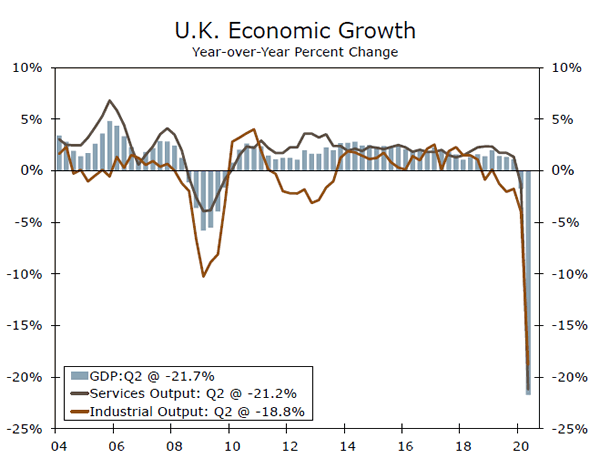

A Severe Economic Slump in the United Kingdom

U.K. second quarter GDP was as bad as feared. The economy shrank 20.4% quarter-over-quarter (not annualized), close to the consensus forecast. Q2 GDP was down 21.7% compared to the same period last year. As might be expected, the release showed broad-based weakness across the economy. Consumer spending slumped 23.1% quarter-over-quarter and business investment fell 31.4%, while exports were down a smaller 11.3%. Meanwhile the industrial and services sectors both recorded large sequential quarterly declines, of 16.9% and 20% respectively.

If there was a silver lining in the GDP details, it was in the 8.7% month-over-month increase reported for June GDP. Services output rose 7.7%, while industrial output rose a slightly larger 9.3%. Although the June increase puts the U.K. on course for renewed growth in the third quarter, in our view the overall economy remains weak enough to make further Bank of England monetary easing more likely than not. We currently expect the central bank to announce a further £100B increase in its asset purchase target in Q4 this year.

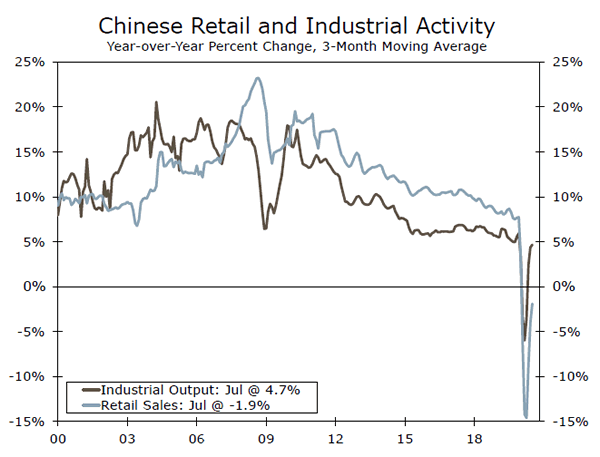

China’s Recovery Continues Into Q3

Chinese economic activity jumped sharply in Q2, and the latest economic figures suggest a further, more moderate, gain could be in store for Q3. Manufacturing continues to lead the way higher, with July industrial output growth steady at 4.8% year-over-year. In contrast, retail activity continues to lag, although July retail sales did show a smaller 1.1% year-over-over decline. Meanwhile, the broader measure of service sector output has been somewhat firmer, rising 3.5% year-over-year in July. So far this year China’s GDP slumped 10% quarter-over-quarter in Q1, before surging back 11.5% in Q2. So long as China can register solid gains in activity in both Q3 and Q4, we believe full-year 2020 GDP is on track for positive growth of 1.6%.

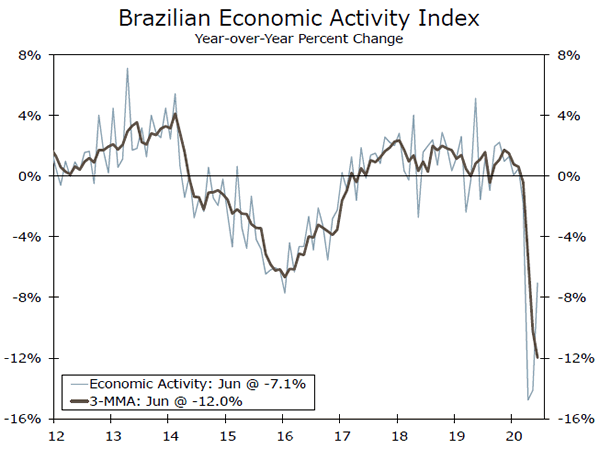

Latin America Still Lagging

In contrast to China, the economies of Latin America still appear to be lagging the global recovery. To be sure this week’s news from Mexico was mildly more encouraging as June industrial output jumped 17.9% month-over-month. However, that increase comes after even larger declines in early 2020, and output is still down 16.9% compared to June last year. Against this soft economic backdrop Mexico’s central bank cut its policy interest rate a further 50 basis points this week, to 4.50%. However, with CPI inflation running above 3% we see little to no scope for further monetary easing from the Mexican central bank. In Brazil, retail sales recorded a second solid monthly increase as June sales rose 8.0% month-over-month. However, the rebound in broader service sector activity has been more gradual. As a result, Brazil’s economic activity index – which is quite closely correlated with overall GDP – rose 4.9% in June, still 7.1% lower than June 2019. In addition, comparing the average level of the economic activity index between Q2 and Q1, Brazil’s GDP looks on course to fall 10% quarter-over-quarter, or more, during Q2 2020.

Global Outlook

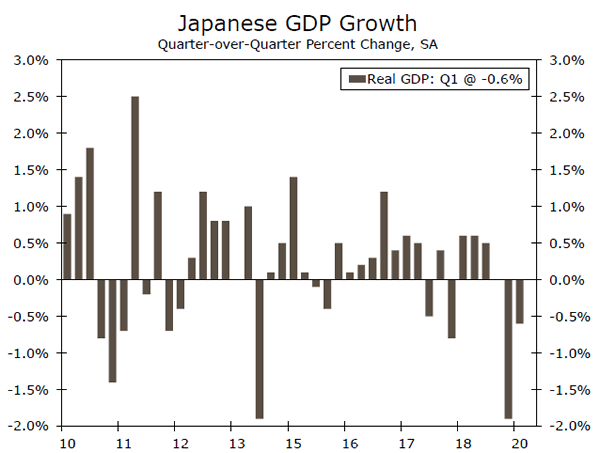

Japan Q2 GDP • Monday

We expect Japan’s economy remained in recession in the second quarter, with GDP forecast to show a third straight decline. Indeed, like most other major countries we expect a large fall in Q2 activity due to the spread of COVID-19 and associated economic lockdown measures. We expect Q2 GDP fell 7.0% quarter-over-quarter (not annualized), while the consensus expects a slightly larger 7.5% decline.

With the consumer only starting to show signs of life June, the consensus projects a 7.8% fall in consumer spending, though declines are also expected in business investment and exports. While we do expect growth to resume in Q3, the softness in the economy in the first half of this year means we expect full-year 2020 GDP to fall 5.5%. Next week’s releases also include the July CPI which is forecast to firm to 0.3% year-over-year. August manufacturing and services PMI are also due.

Previous: -0.6% Wells Fargo: -7.0% Consensus: -7.5% (Quarter-over-Quarter)

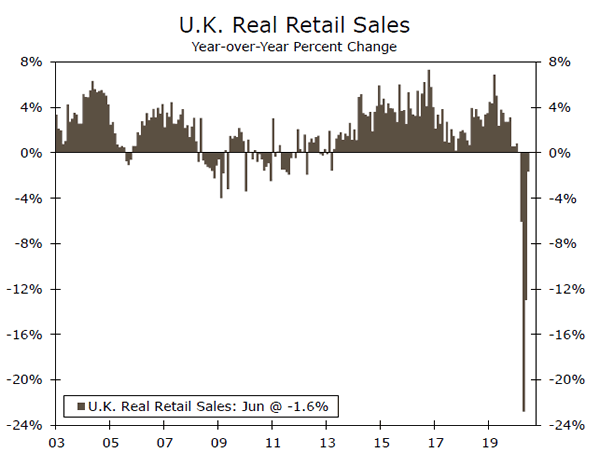

U.K. Retail Sales • Friday

U.K. July retail sales are expected to show a third straight monthly increase, after double digit gains in May and June. The consensus forecast is for retail sales to rise 2.0% month-over-month, which would lift sales back to pre-pandemic levels. We expect sales to rise further in the months ahead, although the pace of increase should remain moderate over the second half of this year after the initial sizeable gains. Weakness in consumer spending was a significant driver of the plunge in second quarter GDP, but the trend in the monthly retail data are consistent with a return to positive growth in consumer spending in the third quarter.

The August PMI figures released next week should also be consistent with a return to positive economic growth in Q3. The manufacturing PMI should rise to 54.0 and the services PMI should rise to 57.0. Both indices are expected to remain above the breakeven 50 level, consistent with a return to positive growth for overall GDP.

Previous: 13.9% Consensus: 2.0% (Month-over-Month)

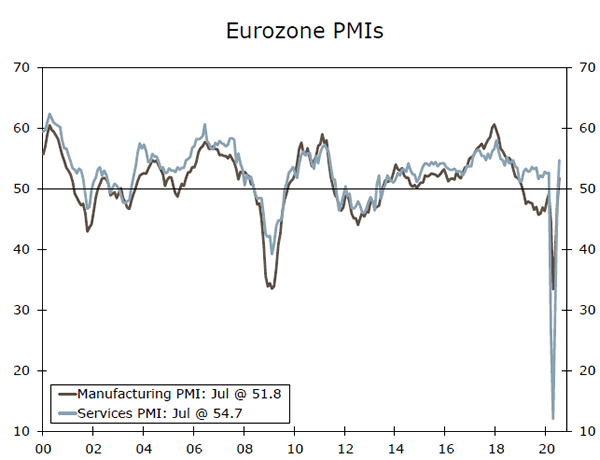

Eurozone PMIs • Friday

The Eurozone August manufacturing and service sector PMIs are among next week’s most significant international economic data. Following a plunge in the purchasing managers indices earlier this year as Eurozone Q2 GDP slumped 12.1% quarter-over-quarter, the PMI surveys reached a significant milestone in July. The manufacturing PMI rose to 51.8 and the services PMI rose to 54.7 – the rise above the breakeven 50 level for both indices suggesting a return to positive economic growth.

For August, the consensus expects another solid round of readings for the PMI surveys, with the manufacturing index forecast to rise to 52.7 and the services index expected to be broadly steady at 54.6. Aggressive monetary and fiscal stimulus reinforce the outlook for a rebound in activity in the second half of this year. However, given the depth of the economic decline in Q2 in particular, we still expect fullyear 2020 GDP to fall 8.3%.

Previous: 51.8 (Manufacturing) ; 54.7 (Services) Consensus: 52.7; 54.6

Point of View

Interest Rate Watch

Supply & Demand

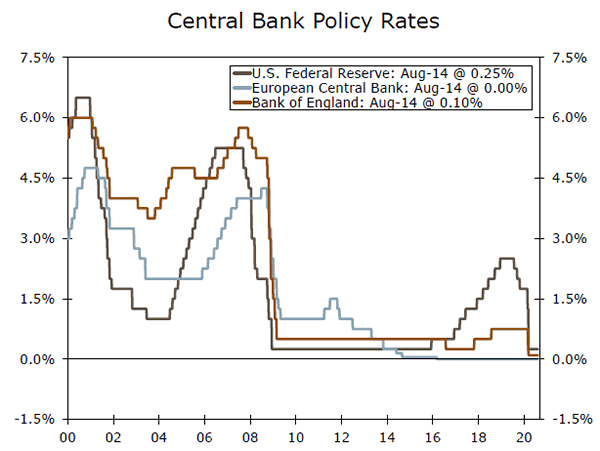

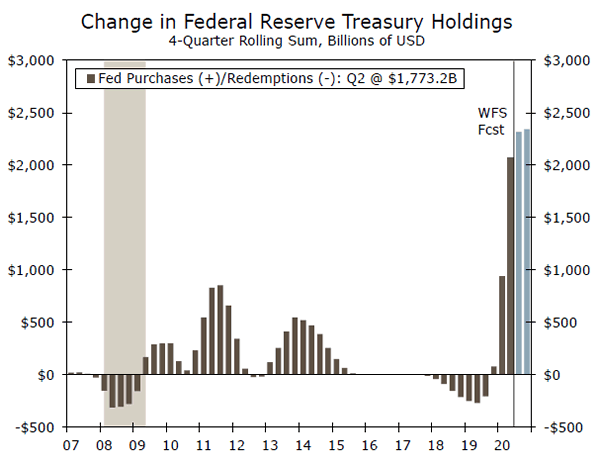

The Federal Reserve has repeatedly made it clear that they are prepared to do whatever is necessary to prevent the current health care and economic crisis from morphing into a financial crisis, which would be much more costly and tougher to ultimately recover from. Along those lines, we saw a trio of Fed speakers this past week urge Congress and the administration to come to some sort of agreement on extending emergency stimulus programs. The lack of an agreement means the Fed is more likely to increase the amount of securities that it is purchasing, which will keep interest rates lower than they would be otherwise. We also expect the Fed to further firm up forward guidance, to assure market participants that the federal funds rate will remain near zero for a least the next couple of years.

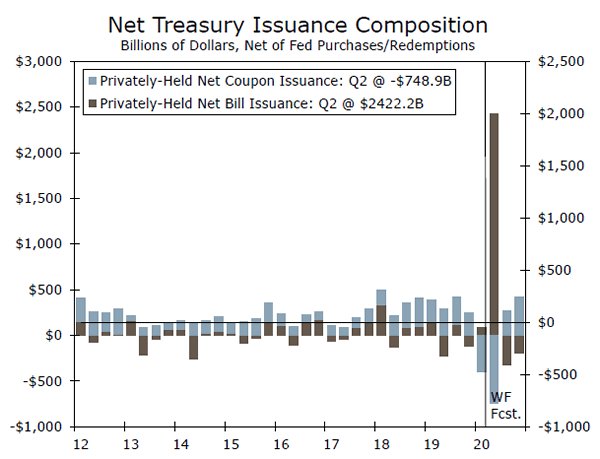

The Fed’s actions are in some sense the easy part and can be done with little to no political influence. The supply of Treasury securities, however, looks somewhat uncertain. With leaders in the House sticking close to their $3.5 trillion proposal, it’s possible that a final deal could be larger than many expect, resulting in even more Treasury issuance. Holding the line on rates, particularly as asset prices and commodity prices firm up, may become a bit more difficult.

This week’s economic reports generally showed economic activity continuing to firm and did not moderate along the lines that the high-frequency data had. The drop in jobless claims below the one million mark and the solid increase in core retail sales and the upward revision to the June data were the biggest standouts pointing to stronger third quarter economic growth. The better than expected economic data strengthen the argument for a smaller relief package. With Congress on summer recess, however, that improvement needs to continue in order for it to meaningful influence negotiations.

The inflation data generally came in higher than expected, although so did productivity growth. The bounce back in the PPI and CPI appears to be just that – a bounce back in many of the components that got crushed earlier, such as auto insurance, airfares and hotel room rates.

Credit Market Insights

Forbearance to the Rescue?

President Trump signed a memorandum on Saturday that extends a student loan relief provision of the CARES Act, originally set to expire on September 30, until the end of the year. The policy orders the Department of Education to continue deferring all federal student loan payments with interest waived until December 31. This is a timely decision, as student debt is an increasing burden for roughly 40 million Americans, with outstanding student debt representing about 11% of total household debt.

The policy has resulted in what would typically be positive developments for student borrowers. Due to loan reclassifications by the Department of Education, we’ve seen nearly a 4% drop in student loans that are 90-plus days delinquent in Q2, which primarily drove the decrease in total household debt delinquencies for the period. The average credit score for all student loan borrowers also improved from March to June, according to the Federal Reserve Bank of New York.

This deferment ultimately frees up some cash for borrowers who may be struggling to pay down their debt. However, given the temporary nature of the memorandum, these developments are at risk to reverse once the policy expires. Remember that forbearance is different from loan forgiveness. Come next year, delinquencies on debt may swing back up, particularly if borrowers remain in a financially vulnerable positions due to the pandemic.

Topic of the Week

No Fiscal Deal, but Executive Orders Galore

Last week, talks between Congressional Democrats and the White House for another round of COVID-19 fiscal relief petered out. At present, both the House and the Senate have left town for August recess, though members are on call to return to Washington D.C. in the event of a major breakthrough.

Against this backdrop, President Trump has attempted to take matters into his own hands through executive orders. First, the president instructed the U.S. Treasury to halt collection of payroll taxes from September 1 through December 31 for workers who earn approximately $100,000 or less per year. Second, emergency federal unemployment benefits were reinstated at $400 per week, down from the previous $600 that lapsed on July 31. Third, the Secretary of Health and Human Services and the Director of the CDC were directed to “consider” whether temporarily halting residential evictions is necessary to prevent the spread of COVID-19. Finally, interest on student loans held by the federal government will be waived through the end of 2020, and payments can be deferred until December 31.

These steps represent more financial support for the economy than would have occurred otherwise. But, they are not as material as initially meets the eye. The payroll tax holiday is a deferral, not an outright cut, so these taxes will still be owed at some point, although President Trump has said he will push Congress for a permanent cut at a later date. The $400 per week in unemployment benefits utilizes an emergency disaster relief unemployment program and we estimate that there is only enough money to last 4-6 weeks given the expected number of claims. Congress holds the keys to a more sweeping and impactful fiscal package, but talks between the two sides remain at a standstill.

{kind=link}