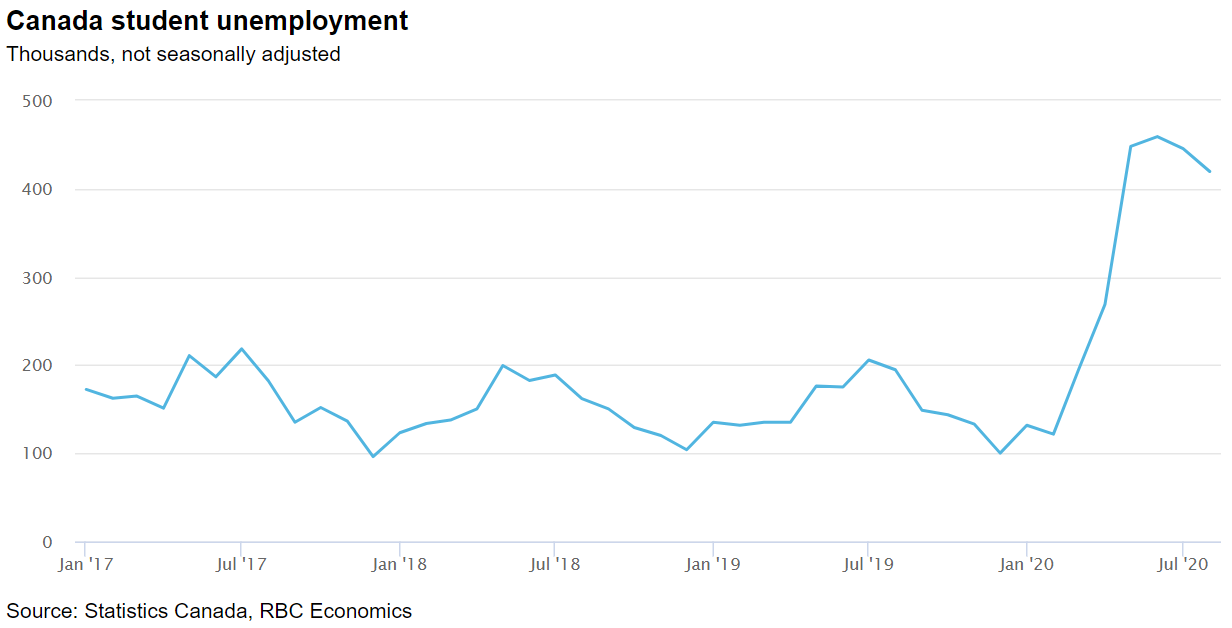

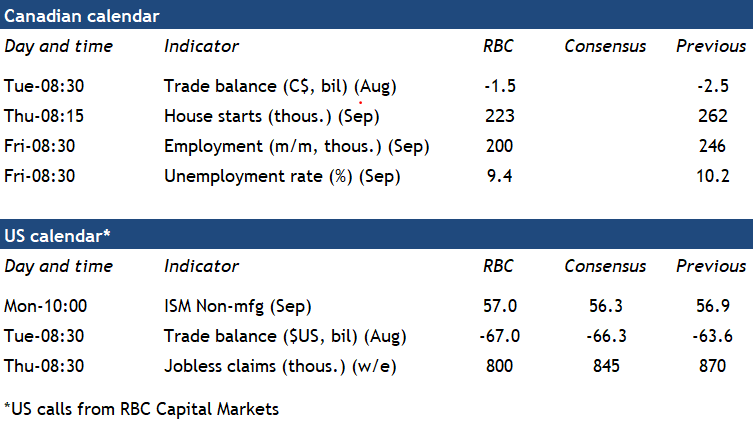

We expect next week’s Canadian labour report to show a 200k increase in employment – the smallest gain in 5 months. Still, the increase will bring the cumulative job recovery to 2.1 million, or 70% of the 3 million jobs lost in March and April. The unemployment rate is expected to dial down to 9.4%, in part reflecting a sizeable number of unemployed students returning to school in September. The summer jobs market was, predictably, very bleak this year. The number of unemployed (but not yet graduated) students was 225k higher this August than a year earlier. As these students head back to school in September and a portion of them stop looking for work, the pool of unemployed workers will shrink as well.

The easing in the pace of labour market recovery echoes the slowing pace of economic activity with Statistics Canada estimating GDP growth continued to slow in August. The hours worked data in the monthly labour market report will provide an early read on how much the slowing momentum spilled into September. The split between part-time and full-time employment as well as temporary vs. permanent layoffs will offer meaningful clues on the underlying health of the recovery. To be sure, the labour market is still very weak. Many workers are still out of jobs, especially in services industries like accommodation and food services, where jobs losses still totaled 260k in August relative to February. The recent resurgence of COVID-19 infections in some provinces may lead to additional containment measures (Quebec has already done so in some cities) leaving the more vulnerable industries at higher risk heading into the final quarter of 2020.

Week ahead data watch:

We expect the Canadian trade deficit improved to -$1.5 billion in August. We are expecting a 2% increase in exports despite an expected 3% pullback in auto manufacturing production after a surge in July.

- After a blazing summer for residential building activity, September’s housing starts next Thursday will be watched closely for evidence that the momentum was sustained into fall. The past week’s August permit data suggests that it likely will, although not at the outsized pace seen in July.

- This past week saw COVID-19 case count rising to unprecedented levels in parts of Canada, prompting the re-introduction of some containment measures in Ontario and Quebec. So far governments have been hesitant to re-impose more stringent lockdowns similar to the ones in spring, and we continue to assume any response this time around will be more targeted and varied by region. But that could yet change quickly if conditions continue to deteriorate.

- US services PMI rose sharply to 55 in August (from 50 in July), as new orders/sales grew from rising demand amid further reopening of businesses. September’s report is expected to show these trends continued.

{kind=link}