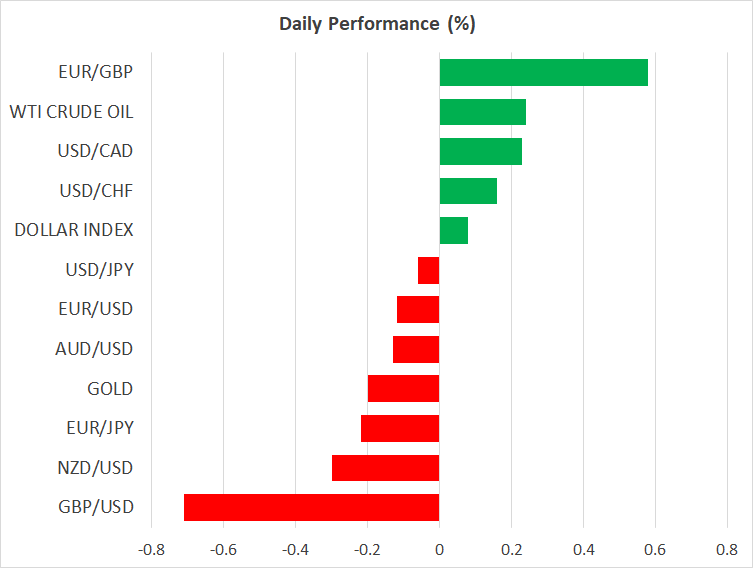

- Euro jumps after ECB fails to over-deliver on stimulus package

- Stocks bounce as Mnuchin hails progress in stimulus talks, but fall back

- Oil breaks higher, unscathed by recent negative developments

- Brexit will continue to dominate ahead of Sunday ‘deadline’

ECB firepower fails to impress markets, euro spikes

Those looking for a euro-killing stimulus package by the European Central Bank were left disappointed yesterday, with policymakers delivering exactly as much ‘juice’ as markets anticipated. The Bank expanded its QE program by €500bn, in a move calibrated to keep the yields on sovereign bonds at rock bottom levels and hence encourage governments to continue their lavish spending spree as they fight the pandemic.

The euro rose since the €500bn move was already well signaled and priced in. What’s striking is that there was zero reaction when President Lagarde stressed that they are monitoring the exchange rate “very carefully”, which suggests that jawboning alone is no longer an effective strategy for pushing the euro down. Actions speak louder than words, as the proverb goes.

Looking ahead, the euro’s fortunes now hang on external factors, namely on how the Brexit saga concludes and how big of a stimulus package the US Congress delivers. The Fed meeting next week could also be crucial for euro/dollar.

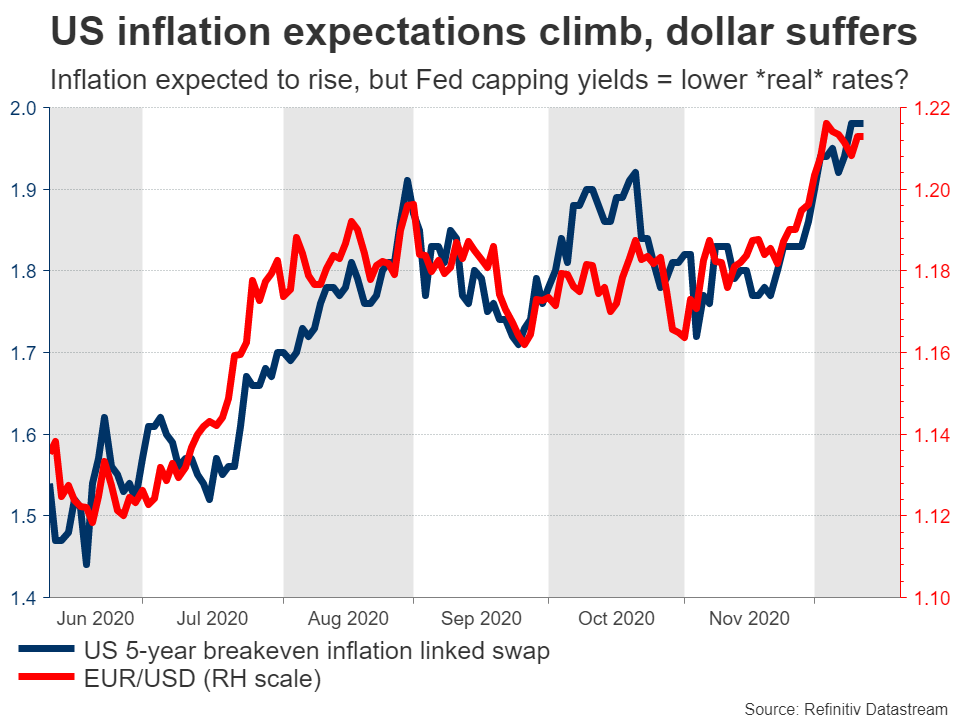

As for next year, whether euro/dollar still has some miles left in the tank will depend mostly on inflation dynamics. Investors hate the dollar right now because US inflation is expected to accelerate faster than other economies, pushing real rates lower as the Fed won’t allow US bond yields to move much higher. This seems quite plausible, but it is only one side of the FX equation. If the euro area continues to struggle economically next year or the global recovery isn’t as smooth as markets envision, this narrative could change quickly.

Stocks struggle for altitude, crude roars

American equity markets erased some early losses to close almost flat yesterday, with a little help from Treasury Secretary Mnuchin, who stated that Congress is ‘making a lot of progress’ in the stimulus talks. The defensive dollar retreated further on the news as risk appetite picked up and the prospect of gigantic deficits weighed.

However, all of this is playing in reverse early on Friday. Futures point to a lower open on Wall Street and the dollar is on the mend, following some alarming Brexit headlines (more below).

What really stands out is crude oil. ‘Black gold’ broke to new highs even despite a steady flow of discouraging news lately, from a huge inventory build-up to OPEC disappointing to new lockdown restrictions across the globe. Crude’s stunning ability to absorb negative news without even flinching likely speaks to a broader shift in sentiment around the oil market, with investors positioning for a bright next year instead of worrying about short-term troubles.

More pain for sterling as Brexit doubts reign

The Brexit guessing game continues to torment the British pound, as markets have started to doubt whether a deal is indeed the most likely eventuality. Prime Minister Johnson warned that the UK should prepare for no deal, while the EU Commission chief apparently told EU leaders that the probability of no deal is higher than that of a deal, sending the pound tumbling.

Admittedly, it is almost impossible to distinguish how much of this is brinkmanship and how much is genuine, but the overall mood seems to be turning sour. The latest ‘deadline’ for determining whether a deal is possible or for abandoning the talks altogether is Sunday, which implies that the pound is likely to open with a substantial gap on Monday – the direction depending on the news.

Overall, both sides have too much to lose by abandoning the talks, but that doesn’t mean it cannot happen. At this stage, this looks like a binary risk for sterling.