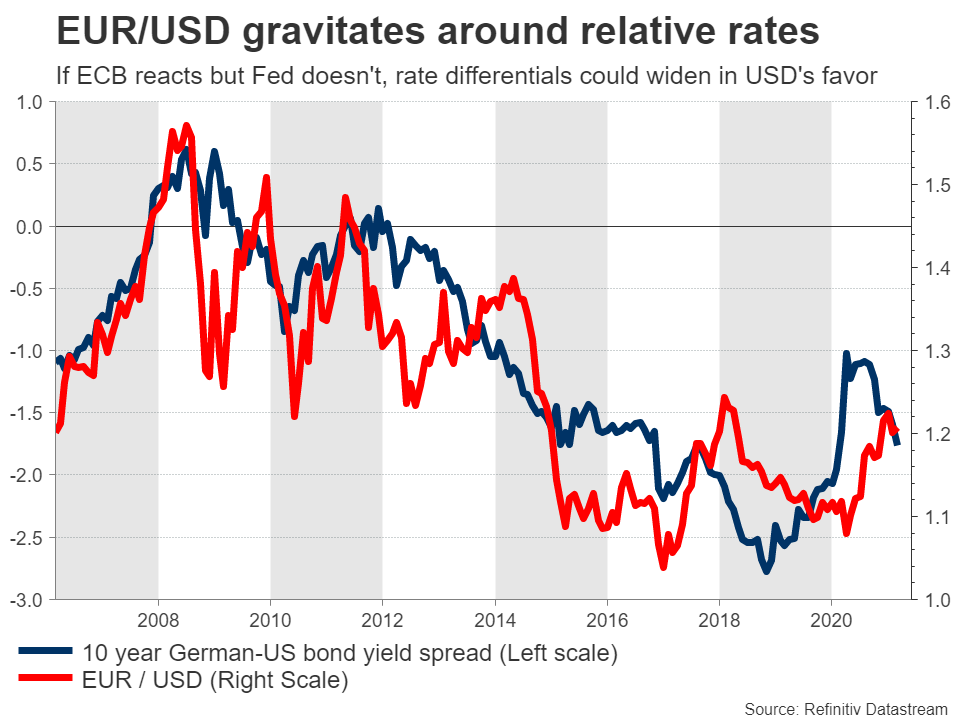

Some central banks like the ECB hit the panic button when bond yields went berserk lately, but some others such as the Fed and the Bank of England appeared rather comfortable with the moves. If this divergence persists, rate differentials between these economies could widen further, spilling over into the FX arena. In this case, the euro and the yen might be in trouble, while the dollar and the pound could shine.

ECB ready to fight?

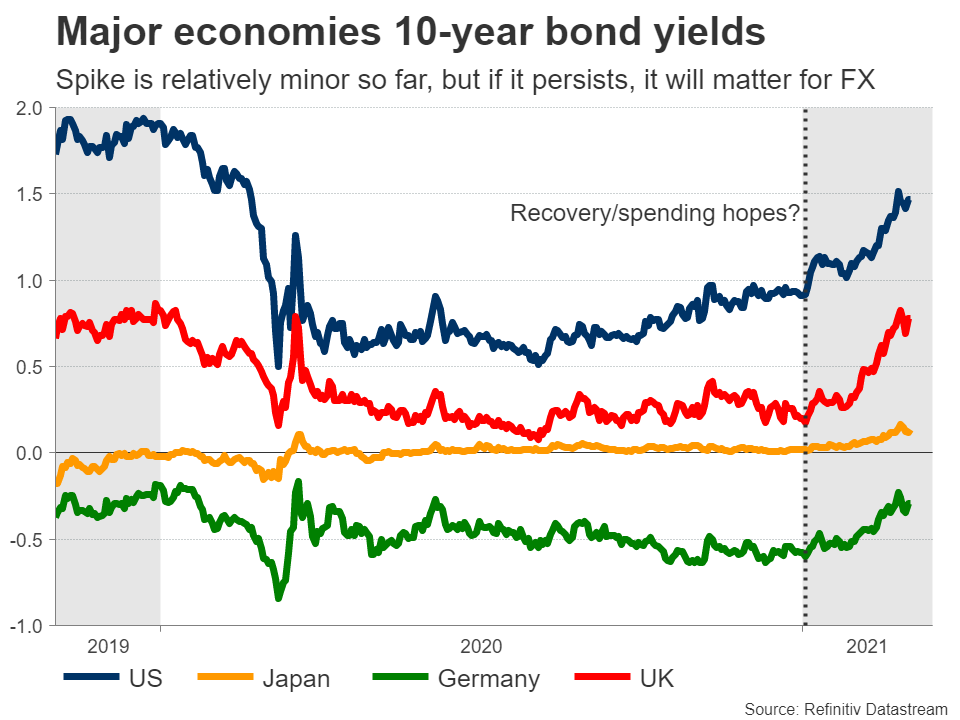

The global spike in bond yields has elicited some very different reactions from central banks. Higher yields can be a sign that investors are becoming more confident in the economic recovery and are thus bringing forward the timeline for rate increases.

But they also raise the cost of borrowing for everyone, from governments to home buyers. As such, sharp yield increases are counterproductive from a policymaking point of view, as they could sabotage the recovery.

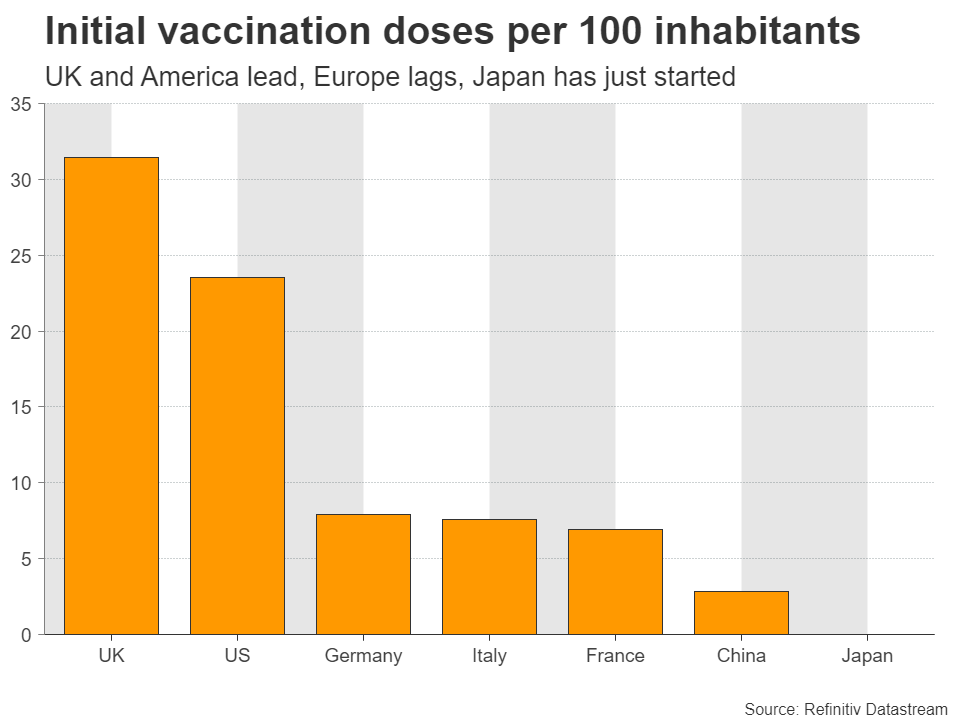

The European Central Bank is the most concerned about all this. From its perspective, this is an American story that is spilling over into the European bond market for no good reason. The US is vaccinating its population quickly, and there’s a cannon barrage of federal spending coming from Congress to ensure the economy heals. This is pushing US yields higher as the Fed is repriced, which is spilling over into the Eurozone.

The problem is that Europe is not really healing. The economy is fragile because of the never-ending lockdowns, vaccinations are painfully slow, and the recovery fund money still hasn’t been distributed to member states. As a result, senior ECB officials have been quite vocal lately, warning that this spike in yields is unwarranted and that the central bank could fight it by increasing its stimulus dose.

Yen crushed by BoJ ceiling

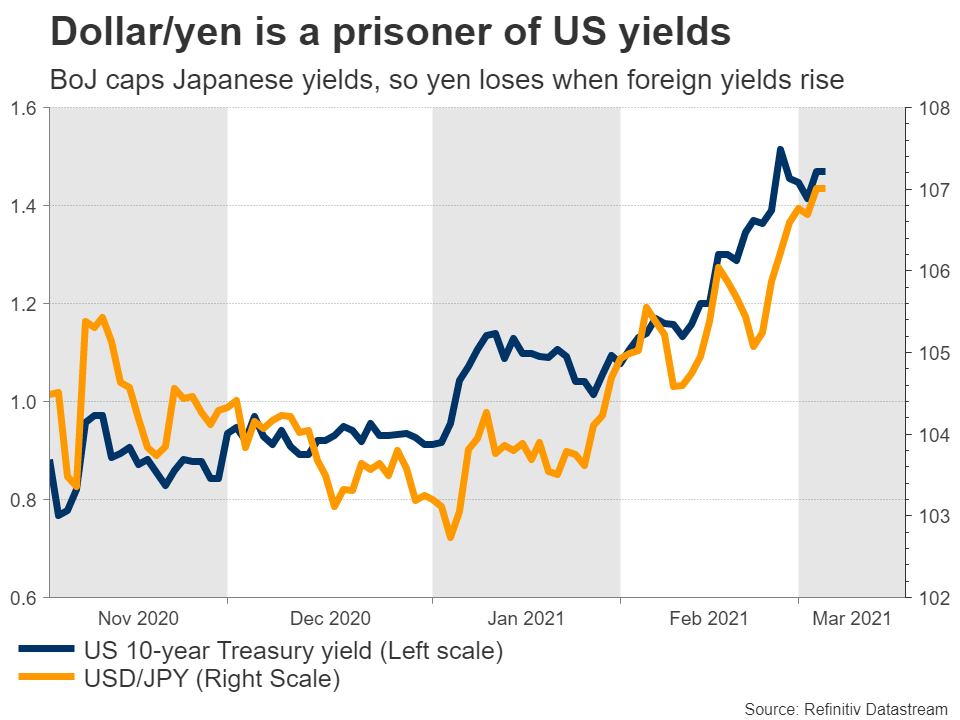

It’s a similar story in Japan, but there is a twist. The Bank of Japan already has a yield curve control strategy in place that keeps a ceiling on Japanese yields, so it doesn’t even need to change its policy settings to fight this global phenomenon. All it has to do is keep the ship steady.

This is bad news for the yen. If global yields are rising but the BoJ won’t allow domestic ones to participate in the rally, interest rate differentials between Japan and the rest of the world naturally widen, making the yen less attractive.

This explains why the yen has been devastated lately. The latest reports suggest the BoJ has no intention of abandoning this strategy, which implies that more pain might lie ahead for the currency if foreign yields continue to march higher. Of course, the mood in global markets will also be crucial considering the yen’s status as a safe-haven.

Fed and BoE sing a different tune

The Fed has a more relaxed view. Most officials seem to think that rates are moving higher for ‘healthy reasons’, reflecting optimism around the economic outlook. Hence, they shouldn’t oppose the move.

After all, the outlook for the US economy has improved dramatically thanks to the swift vaccine rollout, Congress is about to unleash a cannon barrage of relief spending, and the Biden administration is pushing for another gigantic infrastructure package after that.

Of course, there is a limit to everything. The Fed won’t stand idle if bond yields go crazy, as that would tighten financial conditions excessively. That said, the Fed’s pain threshold is much higher than the ECB’s. If this continues, the ECB will probably react quickly, whereas the Fed will only intervene if things really get out of control.

This implies that interest rate differentials between Europe and America could widen further. It is not just a short term story either. Given the outperformance of the US economy, the Fed will almost certainly normalize policy before the ECB does, first by scaling back QE purchases and ultimately by raising rates.

The Bank of England is similar to the Fed in this respect, showing no real concern about rising yields so far. Even though yields on 10-year UK bonds have quadrupled over the last two months, the BoE views this as a natural reaction given that Britain is leading the vaccination race among the developed nations.

What does it all mean for FX?

In a nutshell, rising global yields could hurt the euro and the yen, but boost the dollar and sterling. The ECB’s pain threshold for higher yields is apparently very low, and if it takes action soon to negate these ‘harmful’ moves, the euro could take a hit. Similarly, the BoJ doesn’t even need to act. Because of its yield curve control strategy, higher global yields will automatically weaken the yen.

In contrast, the Fed and BoE are less likely to shoot yields down. They could react if yields truly go parabolic, but that will likely be after the ECB, and the amount of firepower they deploy might be less as well.

Putting everything together, the risks surrounding euro/dollar and euro/sterling seem tilted to the downside, whereas the risks around dollar/yen and sterling/yen may be skewed to the upside.

The key risk to this view would be a major risk-off episode in global markets. If stocks plummet for example and panic returns, investors might pile into bonds again just for their safety, pushing yields back down.

Even so, that’s unlikely to last for very long. The overarching narrative is that central bank normalization is on the horizon, but the Fed and the BoE will normalize much earlier than the ECB or the BoJ.

{kind=link}