It will be a quiet summer week, with no central bank meetings and only a handful of economic data. The main event will be the latest edition of US inflation, which could shape the narrative around the Fed and the dollar. Overall, we are entering a period when market liquidity might be very thin, making sharp moves possible without much news.

US inflation set to cool

Fed officials have started to beat the tapering drums. This past week, another two senior policymakers threw their weight behind dialing back stimulus soon. One of them was Vice Chairman Clarida, the Fed’s second in command.

The other was Board Governor Waller, who went as far as saying that if the next couple of employment reports are strong, the Fed should get the ball rolling in September already. Both are permanent voters in the FOMC, so their views carry weight.

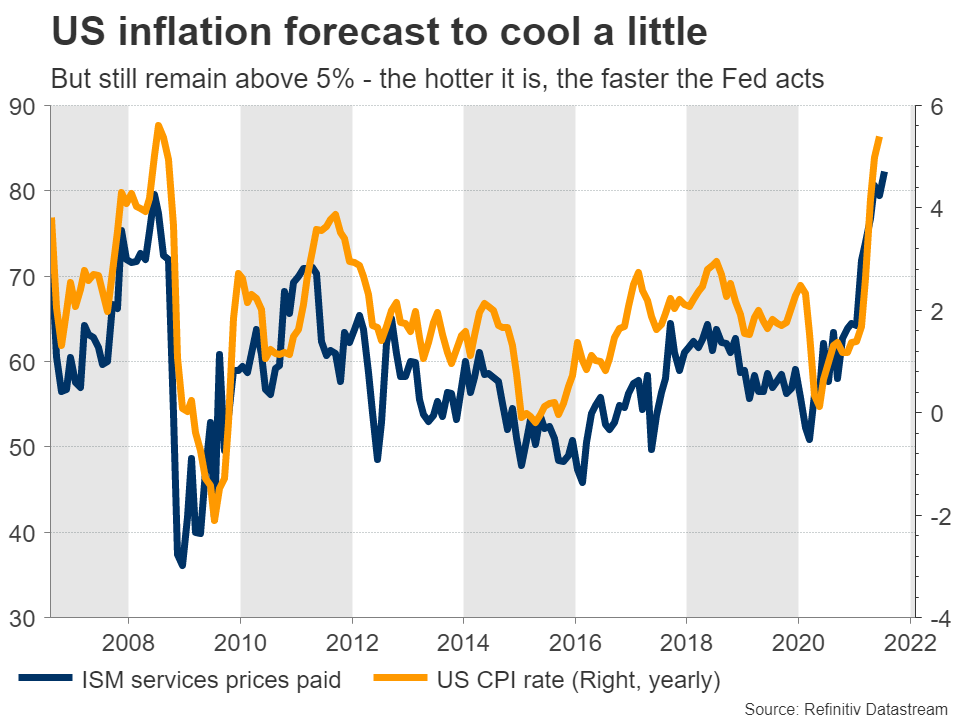

Next week’s inflation stats will be crucial. Forecasts point to a minor slowdown. The monthly CPI print is expected at 0.5% in July, which would push the yearly rate down a touch. That said, this would still leave the yearly rate comfortably above 5%. We could also see an upside surprise, considering the signals in the PMI surveys.

The dollar’s path next week will depend on this dataset. It could determine whether the prospect of a September tapering announcement is realistic or not. The hotter inflation is, the better the chances that the Fed gets moving early.

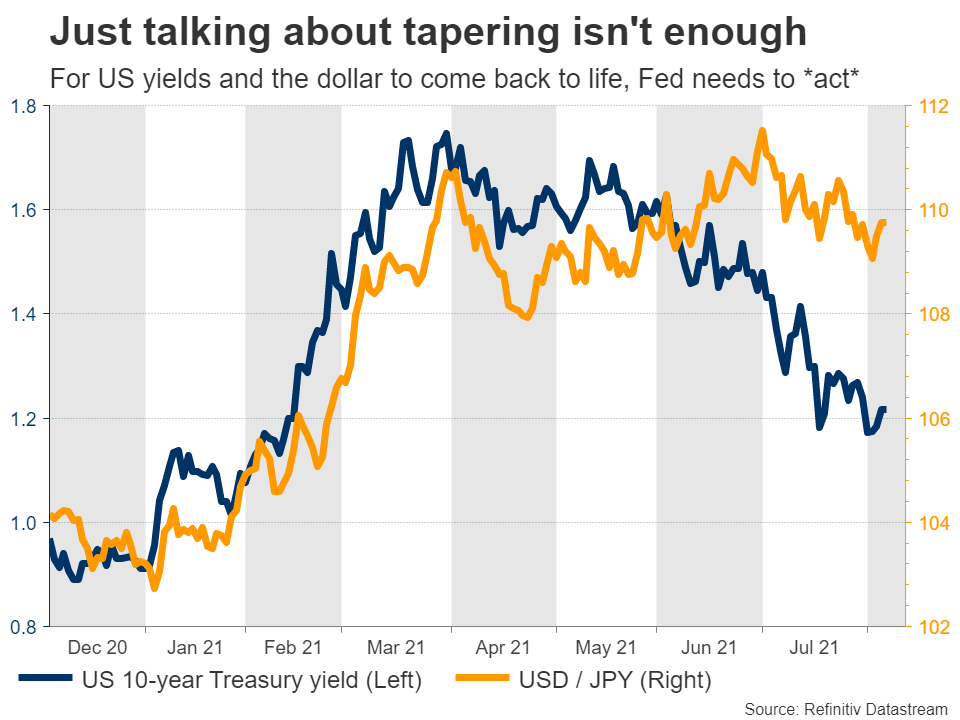

In the big picture though, it doesn’t really matter whether the announcement comes in September or December. What matters is that the Fed is years ahead of the European Central Bank and the Bank of Japan in the normalization game. Ultimately, this points to a stronger dollar against the euro and yen.

The catch is that any dollar strength may not materialize until the Fed actually begins to withdraw stimulus. Fed officials have been flirting with tapering for months now, but real US yields continued to slide. For that to change, the Fed needs to take its foot off the gas, not just talk about it. As the saying goes, talk is cheap.

Sterling turns to UK growth

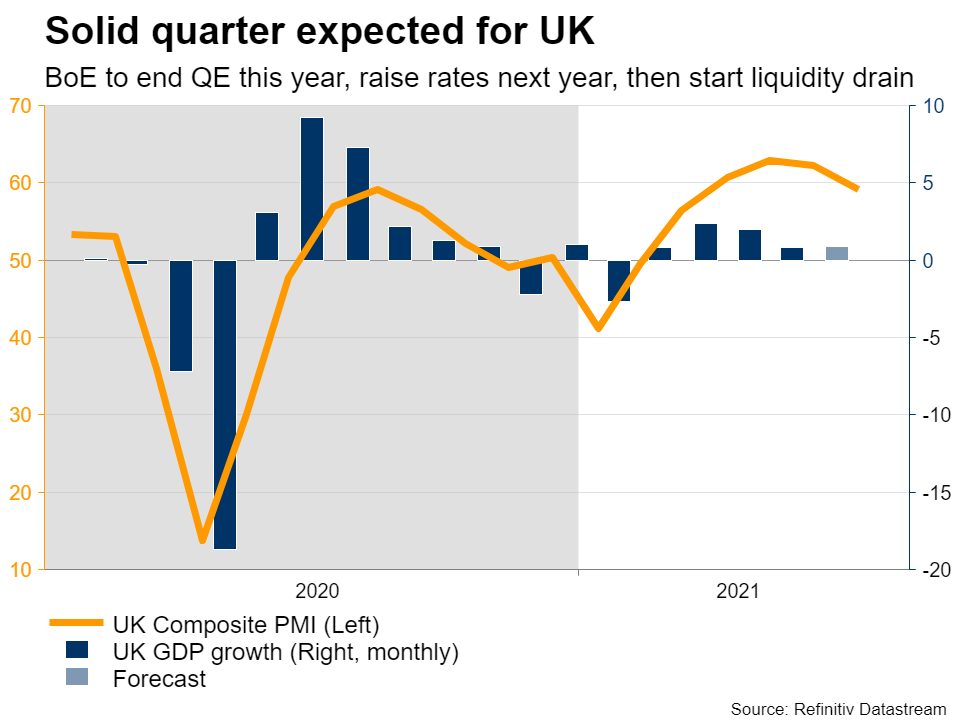

Across the Atlantic, British economic growth numbers for June and the entire second quarter will be released on Thursday. It was a good quarter overall, with widespread vaccinations enabling the reopening of the economy and boosting consumption. Markets will probably focus on business investment, to gauge whether this momentum will be sustained.

The Bank of England took another step towards normalization this week. The first rate increase is now expected in late 2022, while policymakers also signalled that once the Bank Rate hits 0.5%, they will stop reinvesting maturing bonds. This means that after two rate increases, the BoE will begin ‘quantitative tightening’ like the Fed did back in 2017-2019. Higher UK yields are on the horizon.

This is great news for sterling. If the UK economy continues to perform, allowing the BoE to be among the first major central banks to raise interest rates this cycle, the pound could also shine against the euro and the yen.

The FX market is essentially divided into two camps right now – the central banks that will be raising interest rates in the coming years and those that won’t. America, Britain, Canada, and New Zealand are moving towards higher rates, whereas Europe, Japan, and Switzerland aren’t.

For the pound, the risk is what happens to unemployment now that the government’s job-protecting programs are being rolled back. The furlough scheme has been cut back and will end completely in late September. On the bright side, the BoE doesn’t foresee a spike in unemployment because of this.

Chinese and German data coming up

Over in China, trade data for July will be released over the weekend, ahead of inflation numbers early on Monday. Markets usually pay more attention to producer prices, which are seen as a proxy for global factory demand.

In Germany, the ZEW survey for August is due out on Tuesday. This is typically not a market mover for the euro, but it will be interesting to see how strategists see the Eurozone’s largest economy performing in August.

Finally, the earnings season will begin to wind down with household names like Walt Disney, eBay, Electronic Arts, and Airbnb releasing their quarterly results.

{kind=link}