- US jobs report could decide whether Fed pulls the QE handbrake

- Euro trades heavy after German restrictions, commodity FX bleeds

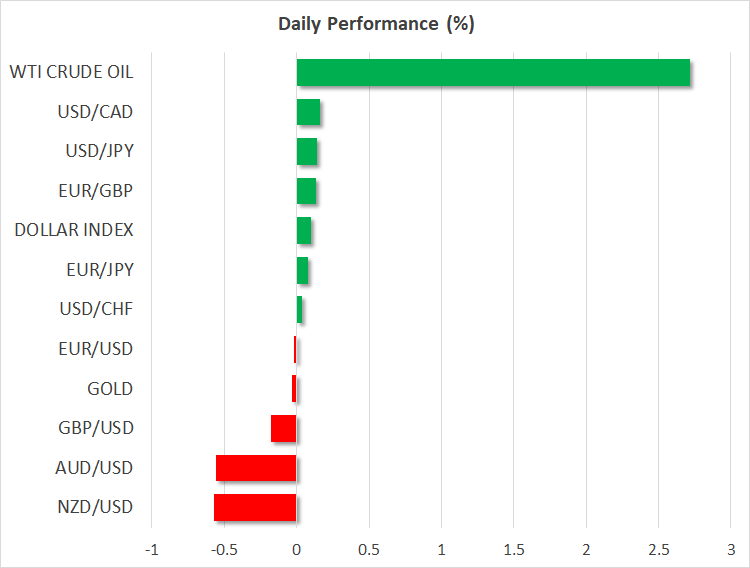

- Oil bounces even without OPEC support, gold grinds lower

Nonfarm payrolls coming up

The US employment report for November will dominate trading in financial markets today as investors grapple with whether the Fed will speed up the tapering process. Nonfarm payrolls are projected to clock in at 550k, pushing the unemployment rate down one tick to 4.5%. Wage growth is expected to have accelerated slightly.

Labor market indicators were quite encouraging during the month. The ADP report showed 534k jobs being added in the private sector, the preliminary Markit PMIs pointed to a “solid” rate of job creation, the employment sub-index of the ISM manufacturing survey rose, and jobless claims fell during the NFP survey week.

Blending everything together, the tea leaves point to another solid jobs report that is more or less in line with the forecasts. Considering also that American workers are quitting their jobs at a record pace in search for higher wages, the US labor market seems to be in pretty good shape overall.

As for the dollar, the outlook remains bright. If the upcoming employment data and next week’s inflation report reaffirm the recent trends in the US economy, that could give the Fed the confidence needed to expedite the tapering process, putting the wind back into the sails of the reserve currency.

A look around the FX market

The commodity dollars continue to bleed as worries over new restrictions have dampened the outlook for global growth, with the Australian dollar hitting fresh one-year lows today. The Reserve Bank of Australia is unlikely to turn the tide when it meets next week as current market pricing for three rate hikes next year seems excessive considering the current state of the economy.

Sterling has suffered a similar fate since Omicron entered the equation, despite recent speculation that this variant may turn out to be more infectious but less deadly. The euro initially found some relief as energy prices cooled, yet the recovery looks shaky when new restrictions threaten to hamstring economic growth.

Germany just announced that unvaccinated people will be barred from restaurants and many shops. Euro/franc touched a new six-year low in the aftermath. The Swiss National Bank is almost certainly intervening to smoothen the descent, but it may need to roll out even bigger guns if it wants to change the course of this battle.

Stocks bounce back, gold feeling blue

The mood in equity markets improved yesterday as bargain hunters came out in force, pushing the S&P 500 higher by 1.4%. That said, the environment could remain challenging until traders figure out exactly what Omicron means for riskier plays heading into year end, especially if the Fed pulls the handbrake on quantitative easing soon.

Oil prices spiked lower after OPEC decided to stick to its planned production increases, but bounced back in the following hours as risk appetite improved to close the session higher overall.

Gold refuses to participate in the volatility that has gripped other asset classes, grinding lower instead. The bulls are now praying that next week brings another US inflation surprise that sends investors scrambling for hedges and chases the blues away from bullion.

Finally, the ISM non-manufacturing PMI will also be released today. Additionally, the latest employment data out of Canada could be crucial ahead of next week’s Bank of Canada meeting.

{kind=link}