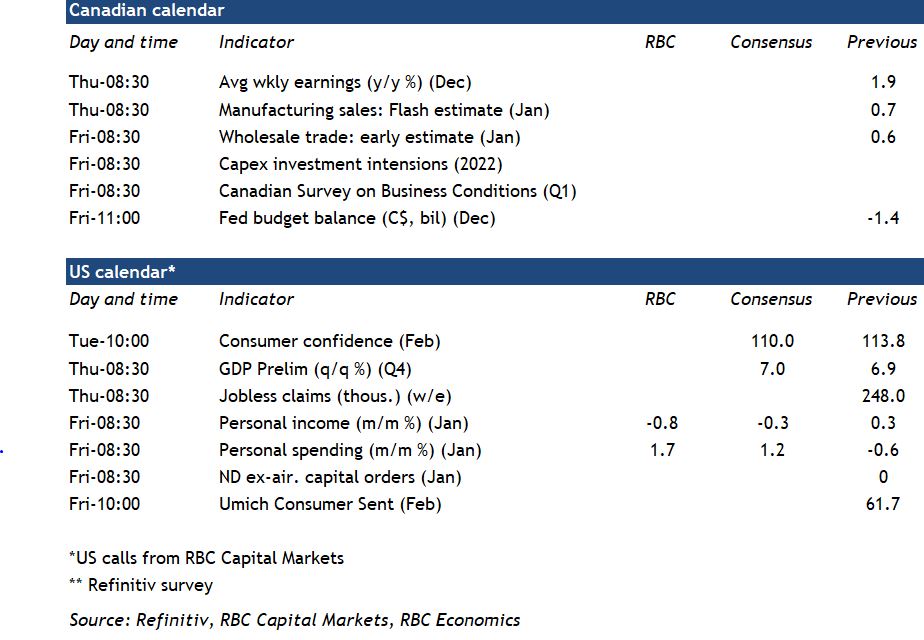

January manufacturing sales will likely look substantially weaker in Statistics Canada’s preliminary estimate for the month. The rapid spread of the Omicron variant kept many workers at home, either due to illness or self-isolation. Indeed, over 10% of manufacturing workers were absent from work due to illness in January and hours worked fell 3.3%. We expect this disruption to be temporary and look for a quick recovery starting in February as the rise in COVID cases slows. What’s more, early signs are that travel and hospitality spending are bouncing back as government restrictions ease. That sets the stage for a broader resumption in activity following an ugly-looking round of economic data last month.

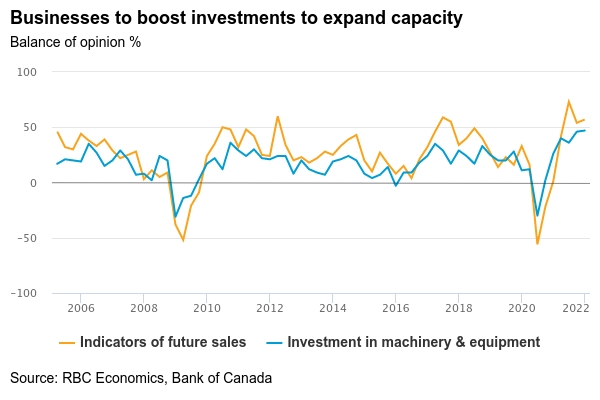

The latest Canadian Survey on Business Conditions (CSBC) will be released Friday. It was conducted from January 4 to February 7, when Omicron was spreading quickly through the population. Still, most firms are likely to have anticipated a rise in sales while acknowledging that capacity pressures and high input costs remain significant issues. In the Bank of Canada’s Business Outlook Survey (BOS), over 75% of firms reported they would have difficulty filling an unexpected increase in orders. Global supply chain pressures are making those challenges worse. And tight labour markets (with more job vacancies than can be filled with the available workforce) represent a production constraint that won’t end with the pandemic. That has pushed business investment intentions higher. We expect the annual Business CAPEX intentions survey to echo increased investment plans (particularly for machinery & equipment) in the BOS as firms rush to expand output.

Week ahead data watch:

- Canada’s alternative labour market SEPH and job vacancy survey will likely record elevated levels of unfilled jobs in December, particularly within the hospitality and retail sectors. Labour markets deteriorated in January, but are expected to bounce back in February.

- U.S. personal spending is expected to tick higher, supported by a 3.8% surge in retail sales that more-than-retraced a 2.5% drop in December.

{kind=link}