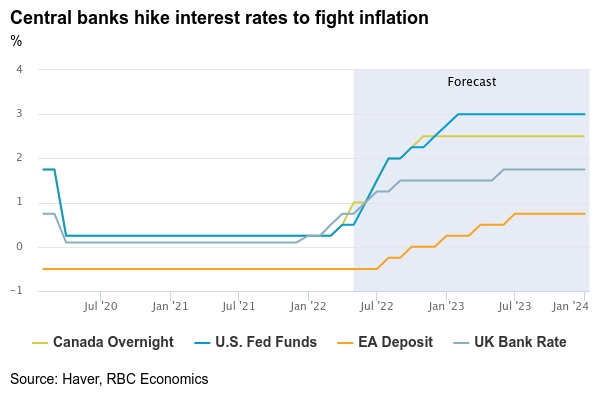

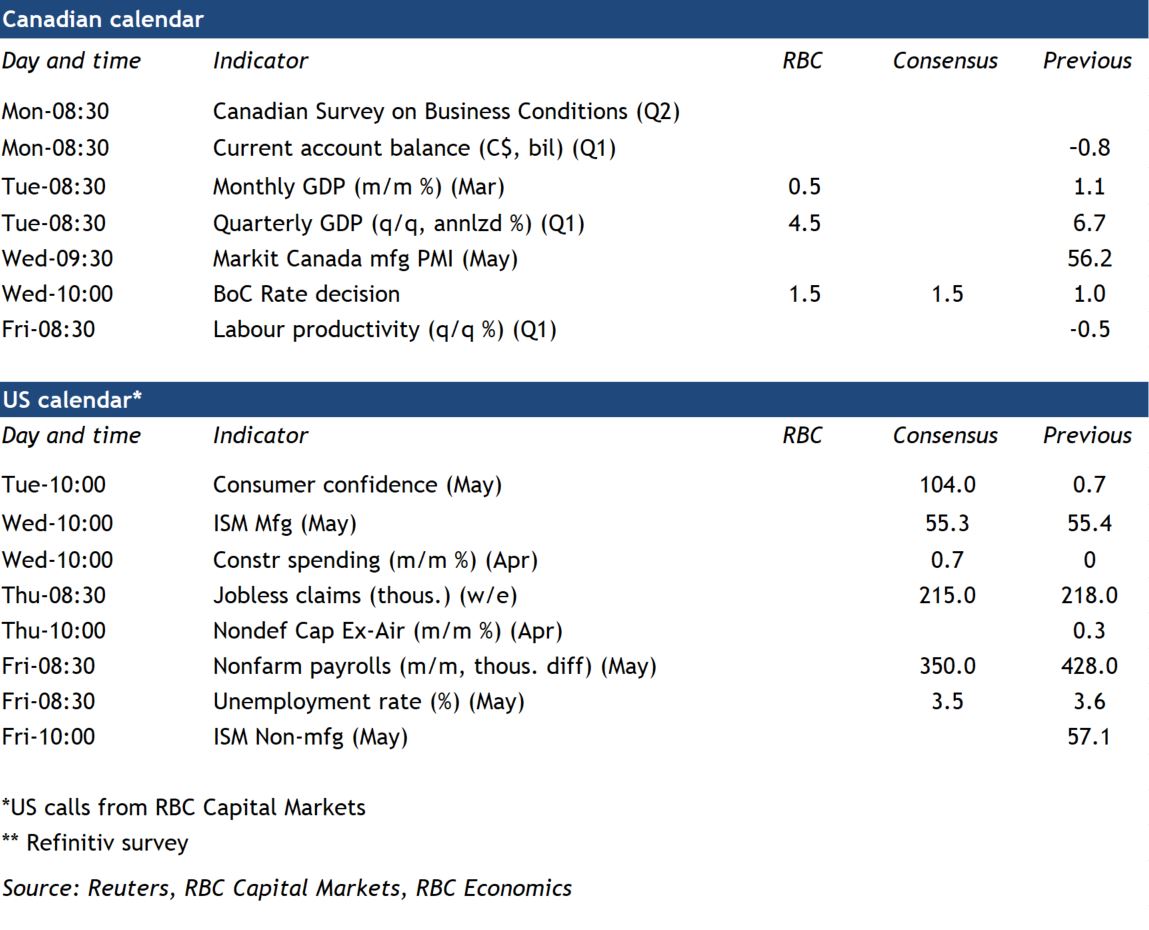

The overnight interest rate is widely expected to rise by another 50 bps on June 1 (to 1.5%), as the Bank of Canada continues its efforts to fight inflation. The hike will build on the BoC’s 50 bp increase in April and 25 bp rise in March—with more increases likely in the months ahead. Inflation is running at the fastest year-over-year pace since the early 1990s. And the economy is running hot, evidenced by still-strong GDP growth and a multi-decade low level of unemployment. We expect GDP growth for Q1 (also to be reported next week) to come in at 4.5%—above the BoC’s last published forecast of 3%. Against that backdrop, the path to at least a more ‘neutral’ level of interest rates—estimated to be in the 2% to 3% range for the overnight rate—is one of little resistance.

The looming question is whether rates need to rise above that neutral range to get inflation back under control. So far, surging inflation has been as much a result of extremely strong demand as supply limits. Higher rates should work to address some of that pressure. Indeed, the initial impact of rising interest rates is already being felt in the housing market, where resales have cooled significantly and prices declined for the first time since the beginning of the pandemic. But with other central banks (including the U.S. Fed) also hiking rates more aggressively, global spending and inflationary pressures are likely to gradually ease. We look for the Bank of Canada to raise the overnight rate to 2.5% by October.

Week ahead data watch:

We expect Canadian Q1 (2022) GDP grew at a 4.5% rate (annualized). Residential investment is expected to tick lower on a dip in home starts and decelerating home resale markets. Net trade is tracking a sizeable subtraction with exports falling more than imports. But we expect consumer spending rebounded quickly following the disruption to spending on services from the Omicron variant in January.

Next week’s Q2 release of Canadian Survey on Business Conditions is expected to point to worsening capacity constraints for businesses in virtually all sectors, limiting their abilities to increase production. Businesses will likely report intentions to further raise output prices, as input, transport costs and wages continue to rise faster, the latter underpinned by severe shortage of labour.

US payroll employment is expected to continue to rise in May with widespread labour shortages adding to wage pressures.

{kind=link}