Sunrise Market Commentary

- Rates: Will risk sentiment continue to support core bonds?

Core bonds profited yesterday of renewed sabre rattling between North Korea and the US, giving the profit taking on shorts more impetus. Today’s data will be largely ignored at the expense of the risk sentiment. There might be some more correction, but we still are in a sell-on-uptick modus, also as oil prices are moving higher. - Currencies: EUR/USD and EUR/GBP are nearing significant support levels

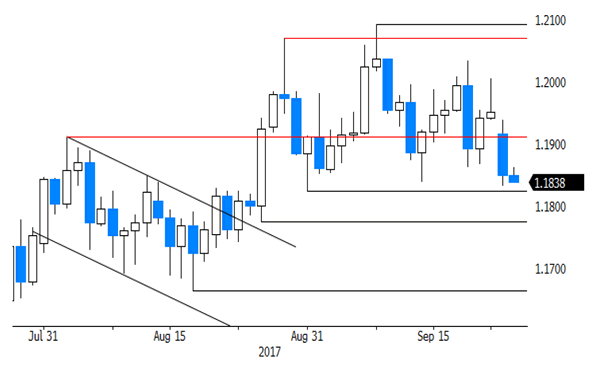

Yesterday, sentiment on the euro obviously turned less positive after the German election even as the impact on other markets was modest. A risk-off correction also weighed more on the euro than on the dollar. Eco data probably won’t be decisive for FX trading today. If EUR/USD drops below 1.1823, the recent correction might have further to go.

The Sunrise Headlines

- US equities were hard hit by North Korean threats, but recovered quite well limiting daily losses. NASDAQ lost more ground. Asian equities trade marginally lower.

- Brent crude oil has risen above $59 a barrel to its highest in more than two years, lifted by fast-growing demand and a threat to Iraqi Kurdistan’s crude exports as the autonomous region holds a referendum on independence

- The U.S. has gamed out four or five scenarios on how the crisis with North Korea will be resolved, and "some are uglier than others," McMaster said. U.S. officials dismissed as "absurd" N-K Ri Yong Ho’s comment that Trump’s UN speech amounted to a declaration of war.

- NY Fed Dudley signalled one more hike this year, calling factors holding down prices temporary, while Chicago’s Fed Evans and Minneapolis Fed Kashkari said tightening before seeing signs of wage and price pressure would be a mistake.

- The ECB is not scared of tapering QE, ECB Coeure said. The board member said any exit will be careful and "in light of the price stability mandate.”

- Iraq’s parliament voted to ban Kurdish crude exports, take back control of disputed oil fields and demanded troops be sent to Kurdistan-controlled territory after Monday’s non-binding independence referendum. Turkish President Erdogan hinted at shutting off oil exports and at a military response.

- Today’s calendar contains US New Home sales, consumer confidence and the Richmond Fed survey. Focus will though be on geopolitical issues, and on the manifold Fed and ECB speakers.

Currencies: EUR/USD And EUR/GBP Are Nearing Significant Support Levels

Will EUR/USD drop below 1.1823 support?

Yesterday, the focus for FX trading turned from the dollar to the euro. The German election outcome might complicate intra-EMU cooperation. EUR/USD settled in a gradual intraday downtrend. The pair dropped below 1.19. ECB Draghi mentioned the recent rise of the euro as a source of volatility/uncertainty. Later on a new exchange of hostile comments between North Korea and the US made investors look for safe havens. The risk-off triggered a simultaneous decline of USD/JPY, EUR/USD and EUR/JPY. USD/JPY finished the session at 111.73. EUR/USD close the day at 1.1848. A real test of the 1.1823 support didn’t occur.

Yesterday’s risk-off trade in the US also leaves its traces in Asian overnight. Major Asian equity indices show minor losses. USD/JPY hovers in the mid 111 area, near yesterday’s low. However, yesterday’s motive, additional fiscal spending ahead of the snap elections, doesn’t support the yen anymore. EUR/USD stabilizes in the mid 1.18 area. Oil jumped sharply higher yesterday and maintains its gains this morning (Brent 59.40 $/p), but there is no obvious (invers) link with the dollar.

Today, the eco calendar is well filled with US economic data, Fed speakers including Yellen and ECB speakers Praet and Liikanen. US New Home sales declined sharply in July (-9,4% M/M). They are notoriously volatile and we expect a significant rebound in August. Consumer confidence (Conference board) was near a cyclical high in August (122.9). However, the hurricanes and higher gasoline prices suggest a decline in September. The market reaction on a weaker figure (consensus 119.5) should be modest. CB speakers are a wildcard. However, Yellen probably will hold the line of last week’s press conference. We don’t expected ECB’s Praet to bring key new elements on the ECB policy debate at this stage.

Yesterday, the uncertain political consequences of the German election outcome for Germany and for Europe weighed slightly on the euro. Contrary to what was the case of late, a flaring up of risk-off sentiment this time weighed more on the euro than on the dollar. So, there are tentative signs that market sentiment turned less euro friendly. Today’s eco data probably won’t be a big help for the dollar. However, question remains whether global sentiment (cautious risk-off) and/or CB talk will sustain a further euro correction. We have the impression that yesterday’s trends (simultaneous decline of USD/JPY, EUR/USD and EUR/JPY) might go somewhat further. A break of EUR/USD below 1.1823 could inspire a further technical repositioning.

From a technical point of view EUR/USD hovers in a consolidation pattern between 1.1823 and 1.2070. It was disappointing for EUR/USD bears that the recent correction didn’t reach the range bottom. More confirmation is needed that the bottoming out process in US yields and in the dollar might be the start of more sustained USD gains (against the euro). In case of a break, next support in EUR/USD comes in at 1.1774 and 1.1662 The day-to-day momentum in USD/JPY was constructive recently, but it was in the first place due to yen weakness. USD/JPY regained the 110.67/95 previous resistance, a short-term positive. The 114. 49 correction top is the next important reference. However, yesterday’s price action suggests that this cross rate remains sensitive to changes in overall risk sentiment.

German election and global risk-off push EUR/USD close to 1.1823 support

EUR/GBP

EUR/GBP: euro softness to inspire further losses?

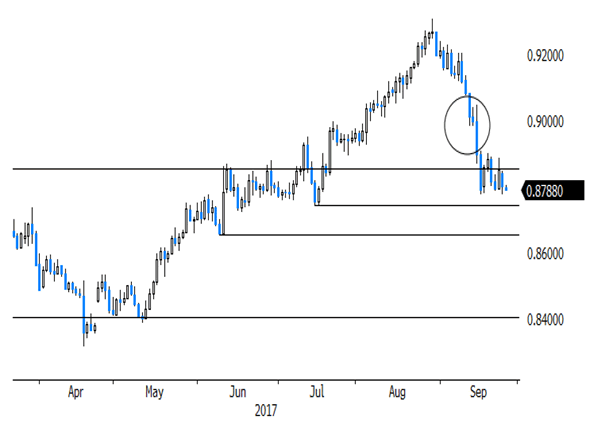

Sterling trading was driven by global markets reaction to the German election results. The euro remained under pressure in early European dealings. EUR/GBP declined to the 0.8785 area. The rise of sterling temporary propelled cable, but finally the dollar outperformed the euro and sterling. The German election outcome might complicate the Brexit negotiations. It hasn’t become easier for Merkel to make concessions. The risk-off correction (North-Korea) later in the session affected EUR/USD and cable in a similar way. Cable closed at 1.3466. EUR/GBP hovered with reach of the recent lows and close the session at 0.8798

Today, UK loans for housing are only of intraday significance. The formal Brexit negotiations restarted yesterday evening. There is no indication that a break-through on the stalemate is imminent. The EU wants progress on the conditions of the divorce, before considering talking on a new trade relationship. In theory this is negative for sterling, but the market focus isn’t on the Brexit negotiations. In line with the assessment on EUR/USD, we think that the euro sentiment has worsened after the German election. If so, the EUR/GBP correction might have some further to go.

EUR/GBP made an impressive uptrend since April and set a MT top at 0.9307 late August. Recent UK price data amended the dynamics and the reversal of sterling was reinforced by hawkish BoE comments. Medium term, we maintain a EUR/GBP buy-on-dips approach as we expect the mix of relative euro strength and sterling softness to persist. However, the prospect of (limited) withdrawal of BOE stimulus put a solid floor for sterling ST term. We look how far the current correction has to go. EUR/GBP is nearing support at 0.8743 and 0.8652, which we consider difficult to break

EUR/GBP: near recent lows