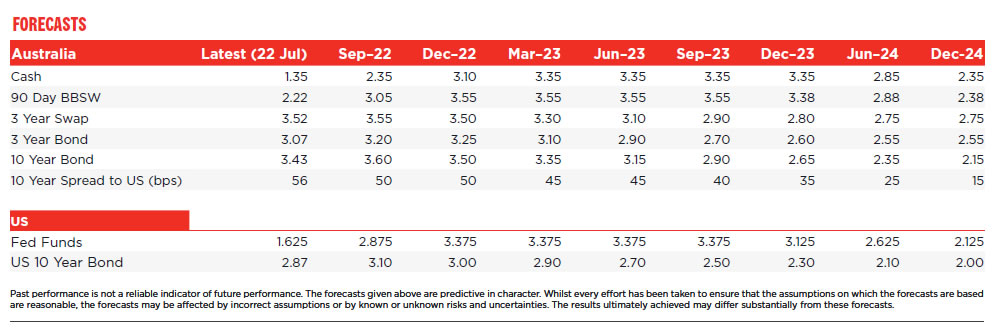

We have revised our profile for the RBA cash rate cycle to include 50bp moves in both August and September; followed by a step down in the pace to 25bp increases at every meeting from October to February 2023. The terminal cash rate forecast has been revised up from 2.6% to 3.35%. Under this policy stance economic growth is expected to slow to 1% in 2023 and the unemployment rate to lift from 3% to 4.4% in 2023. We expect the Bank to cut the cash rate by 100bps in 2024.

This week we have received three very important communications from the Reserve Bank. These were: the Minutes of the July Board meeting; and the speeches by both Governor Lowe and Deputy Governor Bullock.

Three consistent themes run through these pieces:

- The Bank is committed to the concept of assessing the stance of monetary policy through the lens of the neutral rate. The Bank’s estimate of neutral is higher than our own.

- The most significant challenge to returning inflation to the target range is containing inflation expectations and inflation psychology. Such is the emphasis on this issue that it is likely the Bank will err on the side of containing these expectations, even at the risk of weighing more heavily on economic activity than might have been their preference under other circumstances.

- A key area of interest will be how households respond to higher interest rates. There are reasons to expect a degree of resilience given a tight labour market supporting strong nominal income growth; a high savings rate; and large financial buffers in household balance sheets.

Westpac’s forecast for the peak in the terminal cash rate in this cycle has been 2.6%.

That was partly based on our assessment that the neutral cash rate is in the 1.5–2.0% range.

The Minutes, the Governor’s speech, and the Deputy Governor’s responses in the Q&A session all point to the RBA assessing the neutral rate as being at least 2.5%.

The Governor and the Minutes both note that there are a number of different approaches to the measurement of neutral, but the Governor concludes that “most approaches suggest that the neutral real rate for Australia is at least positive.”

Converting this neutral real rate into a nominal rate is trickier when inflation is volatile. Rather than current inflation, the adjustment should use medium to longer term inflation expectations. He currently assesses these as being at the target rate of 2.5% but points out that if inflation expectations were to lift then the neutral rate estimate would also increase.

The cash rate is currently 1.35% and we have been expecting the Board to lift the rate to 1.85% at its August meeting.

That will still be 65bp below the Bank’s assessed neutral rate.

We had assumed that having reached 1.85% – within our estimated ‘neutral zone’ – the Board could step back to smaller increments at a slower pace. Our profile was for: a 25bp lift in September; followed by a pause in October; a 25bp move in November, in response to another sharp lift in annual underlying inflation in the September Quarter inflation report; a pause in December and a final lift of 25bp at the February Board meeting in response to the peak in annual inflation in the December Quarter inflation report. That would see a terminal cash rate of 2.6%.

Given the guidance from the Bank this week, that neutral is 2.5%, it seems unlikely that the Board would take until next February to reach its assessment of neutral.

Such an approach seems particularly unlikely given the nervousness around inflation expectations and the current accurate assessment of a very tight labour market and a resilient household sector. On the latter we also note that momentum in spending is likely to be remain solid through the June and September quarters despite the recent collapse in Consumer Sentiment.

Accordingly, we have revised our profile for the RBA’s tightening cycle to reflect these factors.

Firstly, there will need to be a further 50bp increase in the cash rate in September, to 2.35%, moving it more decisively into the RBA’s ‘neutral zone’.

With the cash rate around neutral and following a cumulative increase of 225bps in only five meetings, it would then be appropriate for the RBA to step the increases down to a 25bp pace in October, taking the cash rate slightly above neutral to 2.6%.

With the policy position now perceived as contractionary the Board would remain on the slower 25bp path, guided by developments around inflation; inflation expectations; the labour market and the economy, while continuing to send the signal that it remains committed to containing inflation by moving policy further into the contractionary zone.

Inflation outcomes and inflation expectation concerns will be the dominant motivating forces for policy.

The September quarter inflation report will signal further increases in underlying inflation to 5% annual growth, prompting a further 25bp move at the November meeting. The cash rate will be 2.85% before the December meeting.

Household spending will be losing momentum and the housing market will have been slowing for nearly six months.

But inflation; inflation expectations and the labour market will still be running too hot and with the cash rate only 35bp above the minimum assessed neutral another 25bp adjustment will come in December.

As in our previous profile we expect that the final increase will be in February following the peak print in both headline and underlying inflation.

As we have assessed previously, we expect the March quarter inflation report, which will inform the May Board meeting, to show a clear fall in both annual and quarterly inflation – a turning point that will allow the Bank to remain on hold.

The difference between this revised profile and our previous profile is that the peak terminal rate will be 3.35% rather than 2.60%. That will be 85bp above the Board’s assessed neutral rate and 135bp above our estimate of neutral.

We think this higher terminal rate will reflect the Board’s risk averse approach which will lead it to err on the side of ensuring inflationary expectations are contained so that inflation can return to the target range over the course of 2023.

Just as the Board over-stimulated the economy in the face of the COVID threat, so it will be prepared to tighten to address what it perceives as the greater risk – losing control of inflation expectations at this time of rising inflation and very tight labour markets rather than fine tuning the economic downturn.

Central banks refer to this approach as taking the course of least regret.

Forecast changes

This higher terminal rate does mean significant changes to our key forecasts.

GDP growth is revised down from 2% to 1% in 2023; and from 2.5% to 2% in 2024.

Consumer spending growth is downgraded from 2.5% to 1.5% in 2023 and from 2.8% to 2.0% in 2024.

The unemployment rate lifts from 3% by end 2022 to 4.2% in 2023 and 5% in 2024 (compared to 3.2% ,3.5% and 3.9% respectively).

Higher interest rates will also add pressure to the housing market where a price correction is already underway. Prices are now expected to decline 4% over calendar 2022 and 10% in calendar 2023, with a ‘peak to trough’ fall of over 15%. Rate cuts, which did not figure in our previous profile, will provide some recovery in prices in 2024.

Underlying inflation slows to 3.0% in 2023 and 2.7% in 2024 (compared to 3.2% and 3.0% respectively).

Containing inflation would, justifiably, be seen by the authorities to be a successful outcome, although our previous forecasts also anticipated a sharp slowing in inflation in 2023 mainly in response to supply side adjustments in fuel, food, building materials and energy.

A 1% growth rate and zero per capita growth in consumer spending in 2023 would be seen, in hindsight, as an acceptable cost to not losing control of inflation and inflationary expectations.

A 2ppt increase in the unemployment rate over two years will be painful (in contrast with 1% in our earlier scenario) but certainly enhances the prospects of containing wages growth to around 4% – meaning positive real wages growth through 2023 and 2024 but not a more problematic rise that would add to inflation pressures.

Despite the insipid growth rate of 1% in 2023 the Board will maintain the contractionary policy stance throughout 2023. Underlying inflation is forecast to hold above the top of the target band through most of the year. That will keep the Board cautious about easing back on policy too early and risking a resurgence in inflationary expectations.

Wages growth will also provide some degree of caution in 2023 as annual growth lifts to 4.5% from the June quarter. Without the higher terminal rate that peak would have been 5%.

By early 2024 with inflation slowing back into the band; the economy operating below capacity; wages growth slowing and the unemployment rate rising it will be time to move the policy setting back to neutral.

Over the course of 2024 we expect the cash rate to be reduced by 100bps from 3.35% to 2.35%.

Growth details of our revised RBA profile (Andrew Hanlan; Matthew Hassan; Justin Smirk)

A strong starting point

The Australian economy has considerable momentum in mid- 2022. This reflects earlier and substantial policy stimulus and a reopening recovery from the delta lockdowns over the second half of 2021 – centred in NSW and Victoria.

Household balance sheets are generally in good shape. Households have accumulated around $260bn in ‘excess’ savings over 2020, 2021 and into early 2022. The saving rate remains elevated and as it normalises towards the “equilibrium” 6% level unlocks substantial dollars to fund additional spending in the near term.

The economy is operating at or beyond full capacity – a situation which we last experienced in the mid-1970s. The number of job vacancies are very high – with 1 vacancy for each person that is unemployed. Output in a number of sectors – particularly home building – is constrained by labour and material shortages – such that a sizeable pipeline of work outstanding has emerged. This large pipeline of work will support the level of activity going forward.

Some of these forces and dynamics which are driving the strong economic momentum in mid-2022 will cushion the looming economic downturn in 2023 as monetary conditions shift to a contractionary stance.

Components of the GDP slowdown

We have updated our Australian activity forecasts informed by the revised RBA rate profile.

We have marked down our output profile for 2023 and 2024. Output growth is now forecast to slow to 1% in 2023, downgraded from 2% previously, then recover to 2% in 2024, rounded down from 2.5%.

Note, that we have also rounded up the 2022 growth forecast, to 4.4%, from 4%, to reflect a likely stronger outcome for the June quarter – with Q2 growth now a forecast 2%, with upside risks.

We assess that trend growth for the Australian economy is in the order of 2.5%, associated with population growth at around 1.5% – the pre-covid population pace and a rate that we expect to resume during the forecast period associated with the reopening of the national border.

In that context, output growth slowing to a forecast 1% in 2023 is substantially below trend and represents a very subdued pace. Some may describe this as nearing “stalling speed”. Such an outcome compares favourably with earlier periods of severe economic shock, such as: the GFC (output contracted by -0.5% in Q4 2008 and domestic demand contracted by 1% over the two quarters to Q1 2009); the early 1990s recession (output contracted by 1.5% over the first half of 1991); and the 2020 covid recession (output contracted by around 7% over the first half of the year).

Our 2023 activity profile envisages that the level of private demand crests in 2023, with annual growth slowing abruptly from around 6% in 2022 to a forecast 0.2%, before improving to 1.4% in 2024 as inflation eases and interest rates are reduced from early 2024.

Output growth of 1% in 2023 will be centred on public demand, up 2% and adding 0.5ppts to activity. Net exports add a forecast 0.8ppts to activity in the year as export growth outpaces that of imports, which are dented by weak domestic demand. Inventories are a drag, subtracting in the order of -0.4ppts, as firms adjust to sluggish turnover.

Weakness concentrated in the consumer and housing

Consumer spending and the housing sector will drive the loss of economic momentum in 2023, reflecting the combined impact of higher inflation and rising interest rates. Consumer spending is forecast to expand by 1.2% in 2023, which is broadly flat in per capita terms. This experience is on a par with that of 2019 (consumption grew by 0.8% that year) – when the economy was soggy at a time of housing sector weakness (including declining prices) and weakness in real wages. Such an outcome for 2023 would compare favourably with periods of economic recession – when consumer spending typically contracts – supported by some of the key dynamics and forces propelling the economy forward in 2022 (a labour market operating at full capacity and a sizeable household saving buffer).

Home building activity contracts by a forecast 5% in 2023. This represents a material but not a sharp downturn. The sizeable work pipeline helps to hold up the level of activity into 2023, cushioning the impact of higher interest rates.

The higher profile for interest rates will also weigh more heavily on the wider housing market. Most capital city markets are already into a price correction phase. The further ‘front-loading’ of rate hikes will see more impact near term with prices now expected to decline 4% in calendar 2022( 6% in the second half of 2022) and a further 10% in calendar 2023 (compared to previous forecasts of –2% and –8% respectively). The ‘peak to trough’ decline within this is around 16%, closer to 18% in the case of Sydney and Melbourne.

Note that the main dynamic here is still the reduction in buyers’ borrowing capacity from higher rates. ‘Selling pressures’ are expected to remain limited, reflecting a relatively supportive labour market backdrop, ample buffers in household balance sheets and tight lending standards applied in recent years which should limit the extent of financial distress and associated ‘urgent’ sales.

Business investment boosted by infrastructure

Businesses will trim investment spending in this environment, but the extent of any 2023 downturn will be tempered by the fact that consumer spending is still expanding – albeit is flat in per capita terms. Total business investment is forecast to edge 0.5% lower in the year. This includes a 4.5% decline in equipment spending and a 4% contraction in building work, largely offset by additional infrastructure work (mining, road projects, renewables) and the uptrend in software spending.

Moving through 2024, momentum in the economy strengthens as inflation pressures recede – taking pressure of real incomes – and official interest rates become less contractionary. Another key positive in 2024 is that the Stage 3 tax cuts commence from 1 July.

The pace of output growth lifts to around a trend 2.5% rate over the second half of 2024, led by the consumer and an emerging turning point in the housing market. Businesses will be encouraged by the upturn, lifting investment spending modestly over the second half of the year.

The 2% output growth forecast for 2024 includes: consumer spending growth of 2%; home building a decline of –5.5% (with weakness in the first half of the year); business investment +1% and public demand +2%, such that overall domestic demand growth lifts to 1.6%, up from the sluggish 0.7% pace in 2023.

Net exports are still a positive, but much less so as imports respond to rising domestic demand, at a forecast +0.2ppts. An inventory rebuild rounds out the growth picture, adding in the order of 0.3ppts, in response to stronger turnover.

The labour market

Historically, domestic final demand leads employment by two quarters. The slowdown in employment unfolds through the first half of 2023 lifting the unemployment rate to 3.4% by the June quarter (from 3% at the end of 2022).

With employment contracting in Q3 (–0.11%) and Q4(–0.18%), the unemployment rate lifts from 3.1% in Q1 to 4.2% by Q4 and peaks at 5.0% in 2024 Q4. At the same time, we only see a modest increase in the working age population of around 1%yr through 2023, as the return to ‘normal’ immigration still lags the pre-COVID pace, but finally lifting to 1.5%yr through 2024.

Footnote: Economics is certainly an art rather than a science. Arguably, the three most important tools and concepts in economic policy making are: the neutral rate; inflationary expectations; and the NAIRU and economists really have no precise measures of any of them!

{kind=link}