Fed Preview: Too Early for a Pivot

- We expect Fed to hike by 75bp next week, which is fully priced in by the markets.

- The recent soft macro data and the WSJ article suggesting that moderation in hiking pace could be near have sparked a ‘pivot’ rally in the markets – we think it is still too early.

- High spot core inflation, only modest tightening in real financial conditions and rising inflation expectations leave Fed little room to manoeuvre.

Anything but 75bp would be a major surprise to the markets next week, so the focus will be on how Fed sees the balance of risks for policy tightening going forward. Is FOMC looking to moderate the pace of hikes already in December or is further tightening in financial conditions still needed? We lean towards the latter.

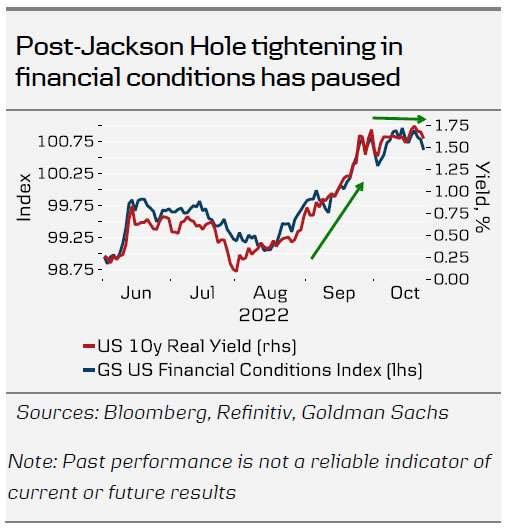

Since the late-August Jackson Hole, Fed has clearly emphasized that there is still too much demand in the economy, and financial conditions need to be tightened further to close the positive output gap. While the communication had the desired impact on the markets in September, lately the direction has been turning.

Real yields have ticked lower, equity markets recovered modestly and EUR/USD is back at parity. As we argued back in Research US – Fed continues to guide US economy towards a recession, 1 September, one of the key risks for US economy is that a ‘verbal’ pivot leads to pre-emptive easing in financial conditions, which is what we are now seeing. Fed also noted in the September minutes, that the cost of overdoing the tightening is lower than allowing inflation to prolong unnecessarily from here.

Fed has to maintain financial conditions restrictive well into 2023 in order to avoid renewed waves of commodity-driven inflation becoming more entrenched – a risk highlighted by Brent still trading above $95/bbl despite the gloomy growth outlook.

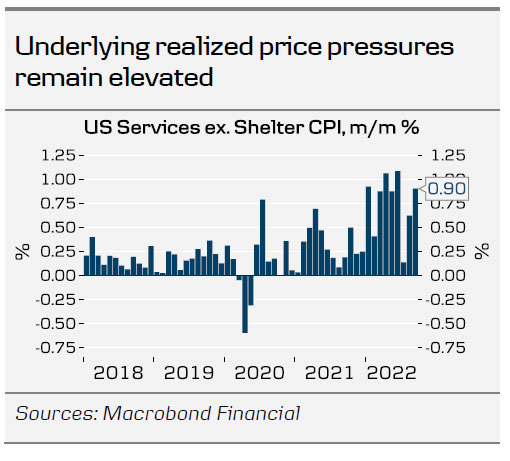

The September CPI surprised to the upside, driven by stickier components of inflation. While the cooling housing markets signal some easing in sticky prices with a delay, shelter prices did not explain the uptick in Core Services CPI in September (+0.8% m/m). In addition, the downturn in freight rates and commodity prices has not translated into lower core goods consumer prices, which to us is another signal of persistently high demand.

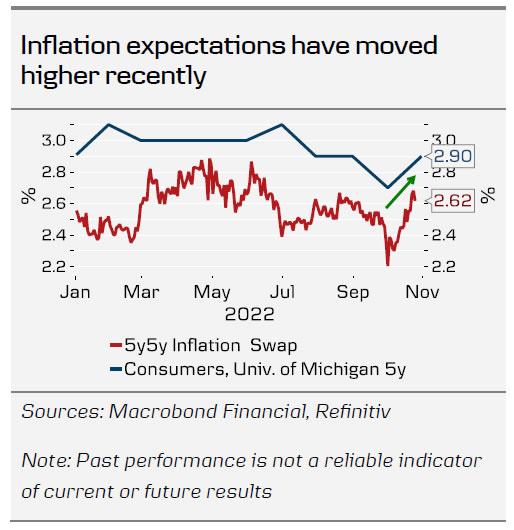

Both market and consumer-survey based inflation expectations have ticked higher in October, with 5y5y inflation swaps now trading at pre-JH levels. The levels are not yet concerning for the Fed as such, but the direction is in stark contrast to the steady decline seen since spring. Labour markets still remain in decent shape with especially the private service-providing sector recording strong gains. The uptick in October Service PMI input prices index suggests, that the rise in labour costs continues to feed into consumer prices at a rapid pace.

We stick to our forecast of 2x75bp hikes this year for now. If Fed clearly signals slower hiking pace (e.g. 50bp) for December, we look to revise our forecast with an additional hike for early 2023.

{kind=link}