Last week was dominated by the US, particularly the impressive data releases on Friday. Other regions could steal the limelight this week, particularly the UK where developments across the board are not encouraging. Friday’s fourth-quarter GDP figure could potentially offer some respite, but will this be enough for sterling to recover some of its recent losses?

UK issues remain unsolved

The UK continues to be seen as the problematic child of Europe. It remains a laggard among developed countries in terms of output recovery since the breakout of the COVID pandemic and it is currently facing the strongest and most stubborn inflationary pressures. The various rate hikes by the Bank of England have yet to slow the inflation momentum suggesting that: 1) the BoE has not been aggressive enough in the current hiking cycle, fearing it will cause a recession, and 2) the impact from Brexit is complicating the economy’s reaction to the higher price of money. The BoE is tasked to solve the hardest puzzle among the key central banks, and it cannot rely on any help from the fiscal side of the equation. The UK government under PM Sunak has set priorities that include halving inflation, reducing debt and growing the economy. These intentions appear sensible, but Sunak remains hamstrung by the Conservative party backbenchers, a powerful portion of the government’s members of parliament that have essentially ousted the previous two prime ministers. If we add the fact that the opinion polls show a significant lead of the opposition Labour party, it looks like the current government has a mountain to climb to return the country to solid economic ground. Inevitably, this fluid political environment is not inspiring confidence in the UK economy, as seen at the recent performance by sterling.

Key piece of data on Friday

On Friday morning the ONS will publish the preliminary GDP figure for the fourth quarter of 2022. The Reuters poll points to 0% quarter-on-quarter growth with the year-on-year figure dropping to just +0.4%. Confirmation of these forecasts would not bring a smile to sterling fans, but could instead offer some consolation that the pessimistic expectations of a technical recession do not appear to have materialized. Having said that, the outlook is not encouraging. The recent IMF forecasts showed the UK is forecast to be the only advanced key economy contracting in 2023. In this context, on Thursday morning we have the usual visit of BoE Governor Bailey et al at the Treasury Select Committee. Provided that the participating members of parliaments do not feel the need to ask tougher questions on the Bank’s perceived inability to tackle inflation, the message from the oral testimonies is unlikely to be much different from last Thursday’s press conference.

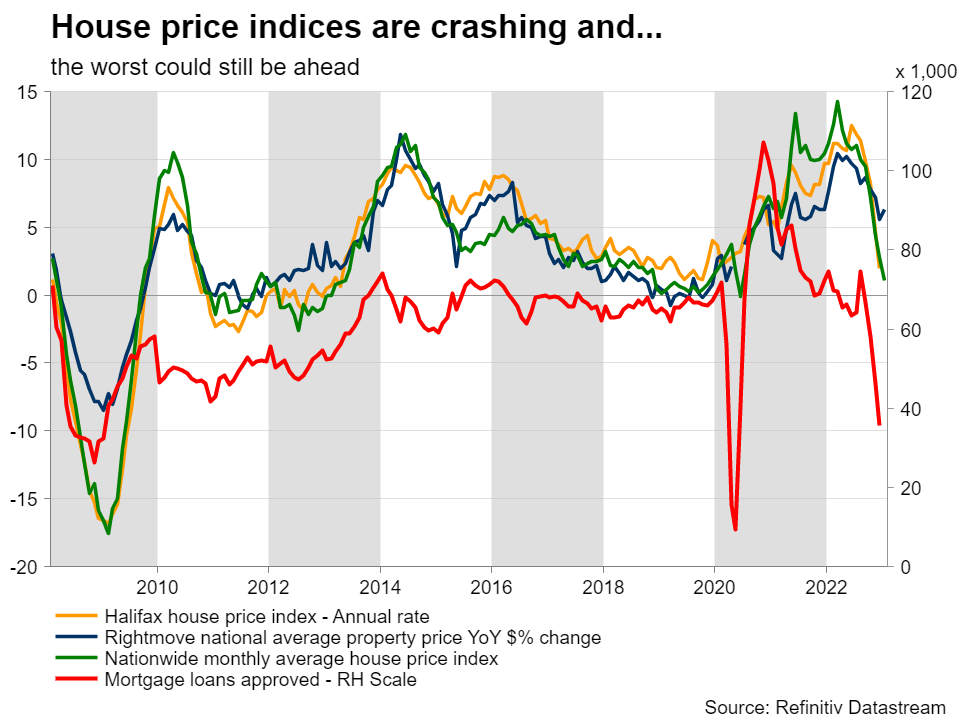

The housing sector is another worry for sterling fans

The January Halifax house price index will be published on Tuesday. The housing sector is especially crucial for the UK economy as property wealth is almost 30% of the total household wealth. The overall negative economic sentiment along with the numerous interest rate hikes by the BoE have put the sector under significant pressure. This is pretty evident by the various indicators measuring price changes. However, the short-term outlook is seen as even more negative due to the recent crash in mortgage approvals. The December print dropped to levels seen during the COVID pandemic breakout in 2020 and amidst the 2007-09 economic crisis.

First taste of January retail sales

Additionally, on Tuesday morning we will get the first real data of consumers’ behaviour in the post-Christmas period as the January BRC retail sales figures will be released. The December year-on-year print showed a promising 6.5% increase, but we have yet to see this figure translating into a similar change in the overall retail sales data. A gap between these two data series has been developing since April 2022. A similar situation was seen during the first part of the COVID pandemic, with retail sales growth eventually recovering aggressively to match the BRC prints in the later part of 2022. However, it could be a while before we see a similar recovery this time as consumer confidence, depicted below using the GfK Consumer confidence index, is close to record lows.

Sterling fans under severe pressure

It has been 11 months since EURGBP touched 0.8200, the lowest level since June 2016, but it probably feels like ages for sterling followers. The continued underperformance of sterling against the euro currency has pushed the pair to the 0.8950 area, testing the September 2022 highs. The latest upward move has been somewhat aggressive, but mostly justified by the momentum indicators. However, there seem to be signs of rally exhaustion developing, which could dent the sterling bears’ appetite at this juncture. A drop towards the 0.8860 would be welcomed by the sterling bulls, but a move closer to the 0.8720 area looks to be more important as it could potentially result in a short-term trend reversal.

{kind=link}