Summary

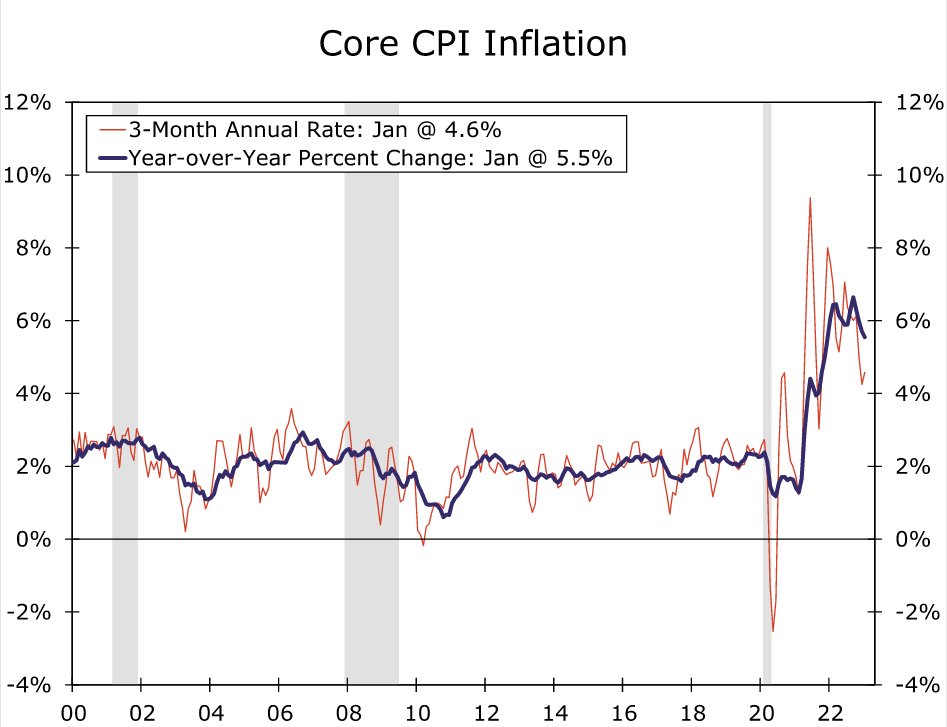

Inflation is not going away quietly. Consumer prices increased 0.5% in January, the biggest monthly move since October. Firmer food inflation and a rebound in energy prices helped boost the headline number. Excluding food and energy, the core CPI increased 0.4% amid a slight pickup in core goods and a solid 0.5% rise in core services prices. Over the past three months, the core CPI rose at a 4.6% annualized pace, an acceleration from the 4.3% run-rate seen over the three-month period ending in December and notably stronger than the 3.1% pace that was originally reported with the December CPI report.

In our view, inflation is still set to grind lower, but the process is likely to be bumpy and take time. Despite some directional improvement over the past couple of quarters, prices are still growing well-above the Fed’s 2% target, and the tight labor market suggests that there are still inflationary pressures that could forestall a full return to 2% inflation. We continue to look for the FOMC to raise the fed funds rate by another 25 bps at both the March and May meetings and to hold the target range at 5.00%-5.25% through the year’s end to ensure that high inflation will be quelled for good.

Inflation Continues at a Vexing Pace

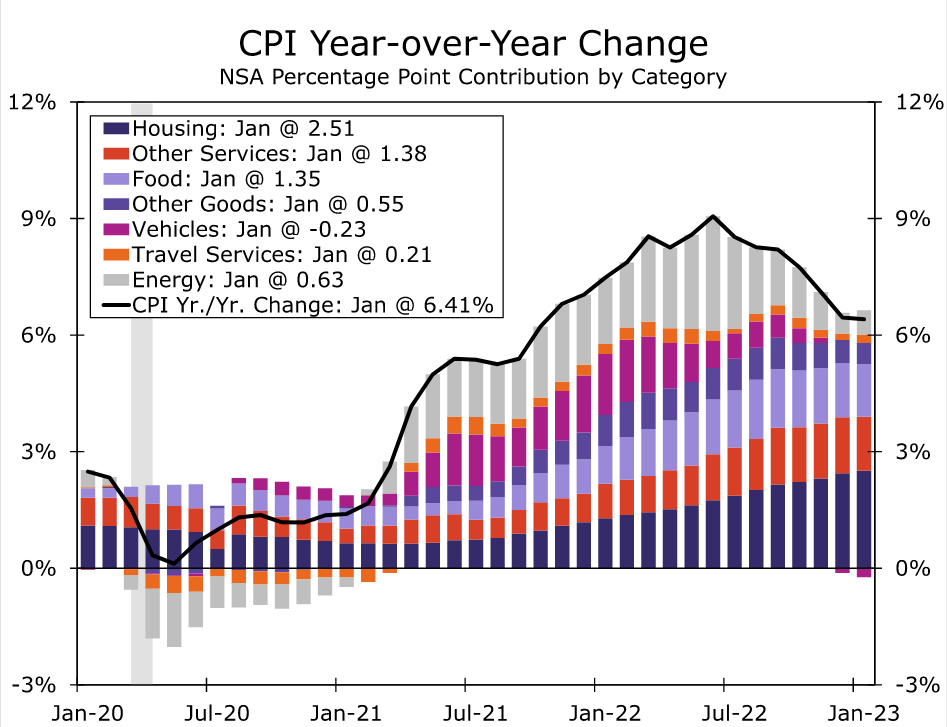

January’s CPI report underscored that the battle against inflation will not be quickly won. Consumer prices rose 0.5% over the month after tame gains of 0.2% and 0.1% in November and December, respectively. The strong outturn in January led the year-over-year inflation rate to tick down only a tenth of a percentage point to 6.4%. Excluding food and energy, “core” prices increased 0.4% in January and 5.6% over the past year.

Annual revisions to the seasonal factors that were released on Friday foreshadowed that, while inflation has come off its peak, momentum remains stronger than the prior three monthly reports indicated. The three-month annualized pace of core CPI inflation through December was revised up to 4.3% from 3.1% previously. The January report further dampens enthusiasm that inflation is rapidly slowing. In light of the strong core inflation reading in January, the three-month annualized rate quickened to 4.6% from the 4.3% pace registered in December.

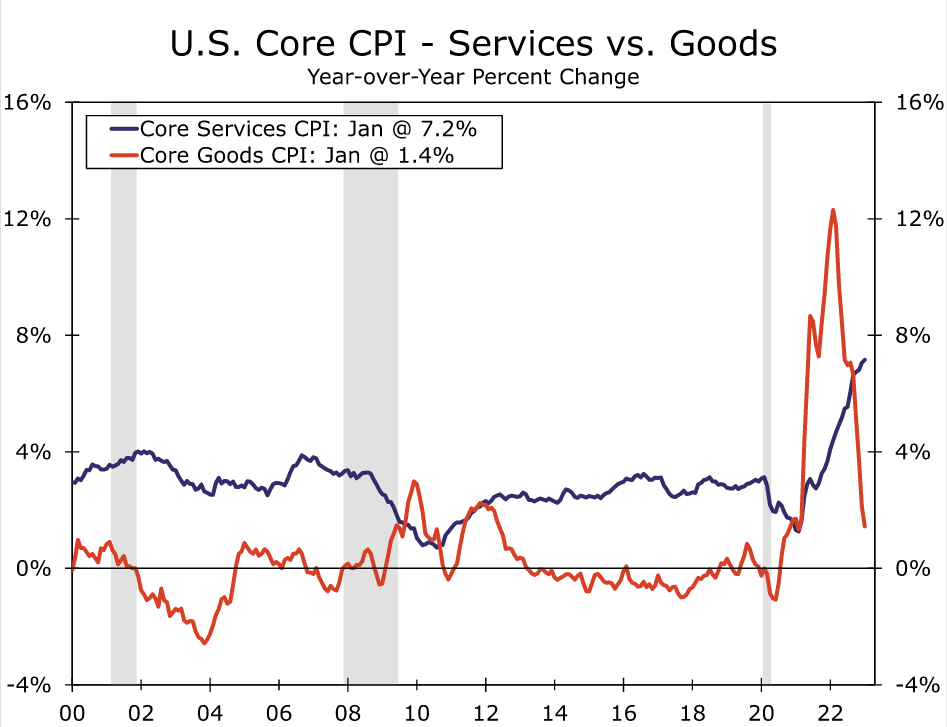

Core goods prices increased a scant 0.1% in January. The normalization in used auto prices continued with prices falling 1.9% in the month, the seventh consecutive month of deflation. New vehicle prices also increased a relatively tame 0.2%. That said, not all goods’ categories posted disinflationary prints. Apparel prices rose 0.8% in January, and inflation for medical drugs and supplies jumped 1.1%. Overall, core goods inflation has slowed markedly over the past year, but as broken out in a nearby chart, the improvement has been primarily driven by vehicles.

Core services prices once again advanced faster than goods with a 0.5% rise in January. Rent and owners’ equivalent rent growth each eased slightly but remained strong with gains of 0.7%, as the long lag between these measures and market-based rents has yet to reflect the ongoing disinflation in residential housing costs. Travel-related services prices were mixed, with lodging away from home up 1.2%, car rentals up 3.0% but airline fares down 2.1%. The core services ex-primary shelter measure that Chair Powell and other FOMC members have cited as a “super-core” measure of inflation increased 0.4% over the month and at a 3.2% three-month annualized rate.

At the same time core prices continue to grow at an elevated pace, prices for necessities continue to bite. Supporting the rebound in inflation in January was a 2.0% rise in energy prices. A 2.4% rise in gasoline prices ends, or at the very least disrupts, a downward run that saw gasoline prices falling 24% over the second half of 2022 and played a meaningful role in the improvement of real income dynamics in recent months. Since peaking in June, headline CPI inflation has fallen 2.7 percentage points on a year-over-year basis, with energy goods alone shaving off 2.3 points. At the same time, consumers have yet to benefit from plummeting natural gas prices, with energy services up 2.1% in January. Price increases at the grocery store slowed only slight in January (up 0.4%) and remain more than 11% higher than a year ago.

Still More Work to Do

Today’s report makes clear that there will be some bumps on the road back to 2% inflation. We continue to look for inflation to trend lower, but we believe getting back to an inflation rate the Fed can live with on a sustained basis will neither be quick nor painless. While inventory dynamics and higher interest rates are putting downward pressure on goods and shelter prices, the tight labor market continues to emit upward pressure on prices across all categories. Over the past three months, the core CPI increased at a 4.6% annualized rate. Although this is down from the highs of last year, it remains too high to meet the Fed’s mandate of price stability.

As we wrote in our recent monthly U.S. Economic Outlook, the prospects for a “soft landing” have increased relative to a few months ago. Among other factors, slower inflation, most notably for energy and food, have helped propel solid gains in real disposable incomes. However, the upshot of a remarkably resilient U.S. labor market is that it may cause inflation to remain stubbornly above the Fed’s 2% target for price growth. Labor demand and cost growth remain inconsistent with 2% inflation, and that keeps the chance of a recession still more likely than not, in our view. We have not seen the end of Fed tightening this cycle, let alone the full effects. We continue to look for the FOMC to raise the fed funds rate by another 25 bps at both the March and May meetings and to hold the target range at 5.00%-5.25% through the year’s end to ensure that high inflation will be quelled for good.

{kind=link}