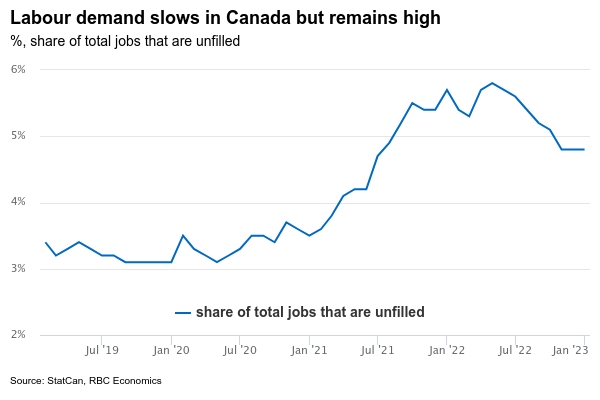

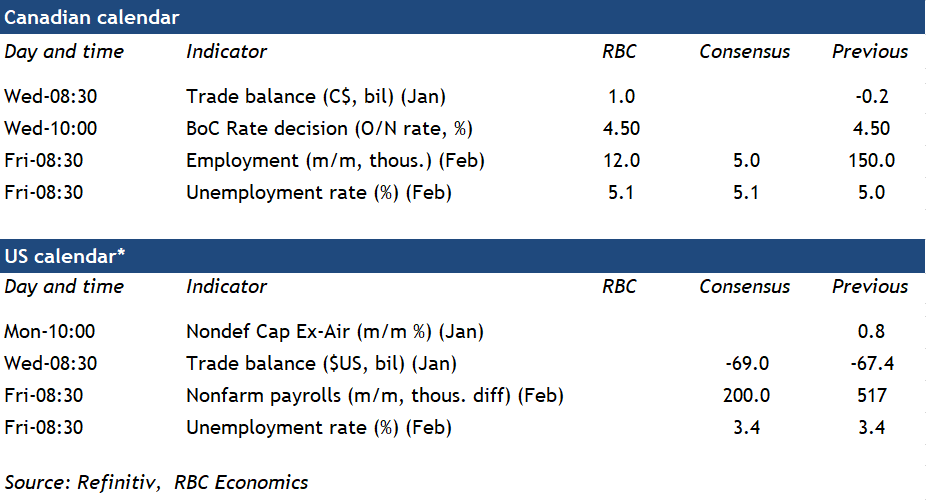

All eyes will be on Canada’s labour market numbers next Friday after a shockingly strong 150,000 employment gain in January. The Canadian employment count is notoriously volatile. Two years of stop-and-start pandemic lockdowns have probably added to those challenges by making the data more difficult to seasonally adjust. And other labour market data hasn’t been quite as robust. The number of job vacancies (while still very high) has declined and the Bank of Canada’s Q4 2022 Business Outlook Survey hinted at slower hiring plans. Still, January’s employment gains were too large and broadly-based to discount entirely. A 0.3% increase in the preliminary estimate for GDP in the month also pointed to a relatively resilient economic backdrop at the start of 2023 given aggressive earlier BoC interest rate hikes. We look for employment to edge slightly higher in February and for the unemployment rate to tick up to a still very low 5.1%. And we continue to expect unemployment to drift higher over the rest of 2023 as the lagged impact of interest rate hikes flow through to household debt payments and weigh on spending and GDP growth.

The BoC will also be looking closely at signs of resilience in labour markets. It’s expected to leave the overnight rate unchanged at its next policy decision on Wednesday—for the first time since the start of this hiking cycle in March of last year. The BoC committed to a “conditional pause” at its January meeting and data released since then (outside of those surprise January labour market numbers) has not met the relatively high bar needed to suggest a change in course. GDP data has been mixed, with a downside surprise on fourth quarter GDP growth offsetting the surprisingly firm 0.3% tick higher in the advance estimate for January. That left growth in the economy tracking slightly below the BoC’s January forecast.

More important, inflation has shown further signs of moderating. Core inflation as measured by the Bank’s preferred indices (CPI trim and CPI median) continue to show improvement. The breadth of inflation pressure has continued to narrow after peaking last summer. We still think the most likely scenario is that the BoC will not need to hike interest rates further this year. But that call hinges on whether the previous hikes are enough to slow consumer spending and labour market momentum in the months ahead.

Week ahead data watch

Canadian trade balance likely edged back to a surplus in January from a small $0.2 billion deficit in December, largely due to an uptick in the oil prices during that month. Advance estimates indicate motor vehicle production jumped higher in January, which likely buoyed both imports and exports.

U.S. payroll employment is expected to rise 200,000 in February, still strong but down from an upside surprise of 517,000 jobs in January. The unemployment rate is expected to edge up to 3.5%. Job postings have been edging lower but weekly jobless claims are still low, and labour markets remained tight.

{kind=link}