U.S. Highlights

- FOMC voting members noted the interest rate path will depend on incoming data and highlighted the uncertainty surrounding the effects of regional bank stress on credit availability.

- Inflation remained relatively elevated, despite moderating last month, as total and core PCE inflation both rose 0.3% month-on-month (m/m) in February.

- Pending home sales in February surpassed expectations by a notable margin as modest price declines and lower mortgage rates supported activity at the start of the year.

Canadian Highlights

- As part of a $67 billion, five-year spending pledge, this week’s federal budget outlined necessary investments in Canada’s clean energy transition. Funds were also put towards health care and cost-of-living relief.

- These measures do come with a cost however, as the government’s deficit remains elevated in the near term, and does not return to balance over the forecast horizon. This leaves the government less flexibility to address a potential economic downturn.

- There were no traces of weakness in the January GDP report, however. GDP expanded 0.5% m/m that month, and Statcan’s flash estimate signals solid growth took place in February.

U.S. – Quiet End to a Volatile Quarter

The last week of the first quarter was relatively quiet as markets continued to digest last week’s Federal Reserve decision and the potential implications of regional bank stress on credit conditions. In terms of economic data, we received updates on housing, consumption, and inflation. Equity markets drifted higher on the week, with the S&P 500 up 2.5%, while the 2-year Treasury yield rose by roughly 30 basis-points (bps) to sit at 4.1% as of the time of writing – still about 90bps below its cyclical peak of 5% at the start of the month.

Starting off on Sunday, we heard from Minneapolis Fed President Neel Kashkari. Reiterating Chair Powell’s statements from last week, Kashkari noted that the banking system is resilient, but that uncertainty remained regarding the extent to which stress in the banking sector may lead to a credit crunch. For this reason, Kashkari assessed that “it’s too soon to make any forecasts about the next interest rate meeting [in May]”. This marks a notable deviation from his comments on March 1st that he was open to a 50bps hike in March. The uncertainty is also reflected in the market’s sentiment about the Fed’s May decision – now pricing the odds of a hike at basically a coin toss.

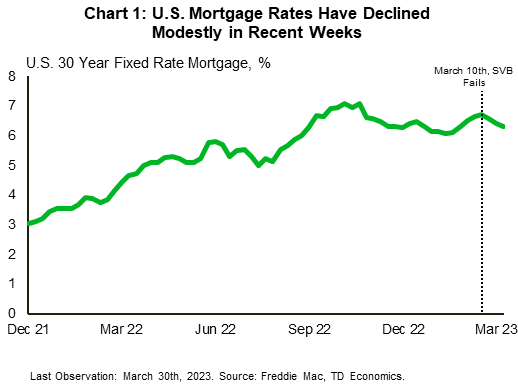

Housing data surprised to the upside this week, with pending home sales rising by 0.8% month-on-month (m/m) in February, down from the 1.8% rise seen in January, but well above the consensus expectation of a 3% m/m decline. This relative strength was likely front-loaded in the month, as mortgage rates rose by roughly 50bps in February. Pending home sales tend to lead final sales by 1-2 months, so this could be an indicator that the spring housing market may begin with some strength, particularly considering that mortgage rates have fallen by roughly 30bps since March 10th (Chart 1). However, stretched affordability and still relatively high financing costs are expected to remain notable headwinds moving forward.

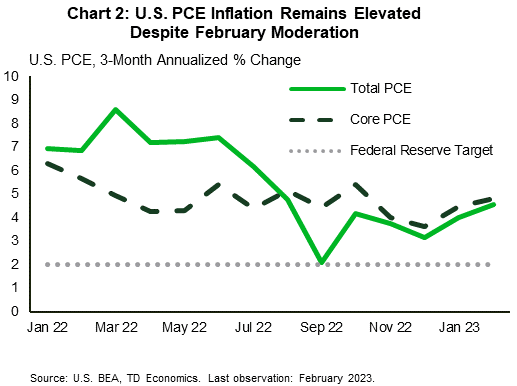

The pulse check on the American consumer this week showed that personal income grew by 0.3% m/m in February, decelerating from January’s gain of 0.6%. This helped to push personal spending up by 0.2% m/m, with housing and health care services seeing the largest increases. Total and core PCE inflation both rose by 0.3% m/m, decelerating relative to January but remaining elevated (Chart 2). More recent data showed that consumer confidence rose in March on a modestly improved outlook for six months ahead, whereas the consumer assessment of the current economic situation deteriorated. The survey cut-off was 10 days after SVB failed, so it is likely that this reading only partially captures the consumer response to recent banking sector stress.

Looking ahead to next week, markets will be closely watching the March employment data release on Friday, with consensus expectations for job growth to cool and the unemployment rate to remain unchanged. This will be one of the more important updates between now and the May Fed meeting, as policymakers continue to look for signs of labor market cooling and its subsequent easing effect on price growth.

Canada – Solid GDP Print Casts Doubt on Cuts

In the current environment, no news is good news for financial markets. A relative dearth of bad financial headlines supported risk-on sentiment this week, pushing Canadian equities and bond yields higher. It also encouraged some flight away from the U.S. Dollar, resulting in about a one cent appreciation in the loonie (as of writing) to just under $US 0.74.

It is premature to expect that we are out of the woods yet with respect to financial market risks. And, even if things don’t materially worsen on that end, economic growth is still likely to slow significantly in coming quarters. Against that slowing backdrop the federal government released their budget this week. In our view, Budget 2023 delivered necessary investments in Canada’s clean energy transition to keep the country competitive with the hefty subsidies in the U.S. Inflation Reduction Act. Specifically, the budget allocated $21 billion in net new spending towards green initiatives through tax credits and access to lower tax rates for zero-emissions manufacturers.

These measures were part of more than $67 billion (about 0.5% of GDP annually) in new spending pledged by the government over the next five years. Other major initiatives were split across the previously announced healthcare transfers to provinces (totaling $22 billion), expanding the dental care insurance program to low-and-middle income families, and other “cost-of-living” measures. The latter amounts to an extension of last year’s the GST rebate which is a more targeted measure than some of the so-called “inflation-relief” funds that have been doled out by provinces over the past year. It will boost household incomes and consumption in the near-term.

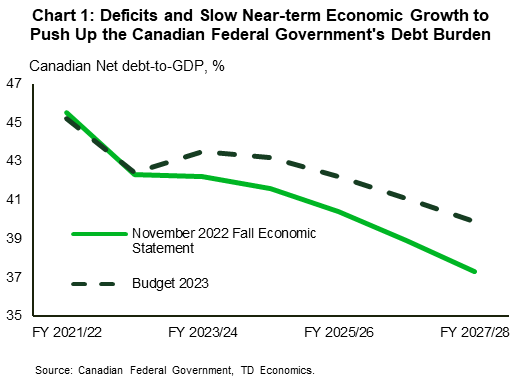

Policymakers’ decision to have their debt burden hang high over the next few years does in theory leave them less fiscal room to deal with a recession if one unfolds (Chart 1). The federal government also maintains a projected deficit through FY 2027/28, versus its November projection of a small surplus that year. Considering the economic backdrop, our preference would have been for the government to build in more prudence.

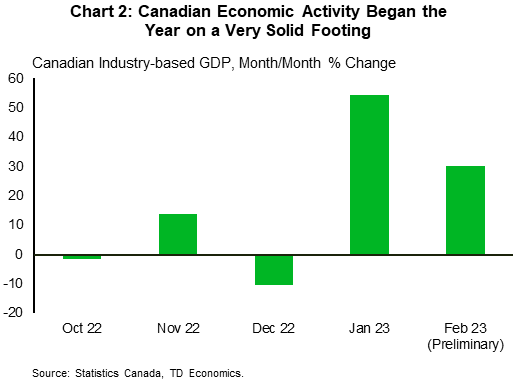

Although Canada’s economic performance is expected to deteriorate as the year wears on, there was no trace of that in today’s GDP report for January (Chart 2). Quite the contrast, in fact, as industry-based GDP expanded at an above-consensus 0.5% m/m pace in January, supported by rebounds in several industries. What’s more, preliminary data points to a 0.3% gain during February. All in, it looks like GDP could record growth north of 2% (annualized) in the first quarter. There’s a high bar for the Bank of Canada to resume interest rate hikes. This solid economic data casts doubts that cuts are on the horizon in the second half of this year, as the market currently expects, and underpins our recent forecast change to move cuts out to 2024.

to sit at 4.1% as of the time of writing – still about 90bps below its cyclical peak of 5% at the start of the month.){kind=link}