Summary

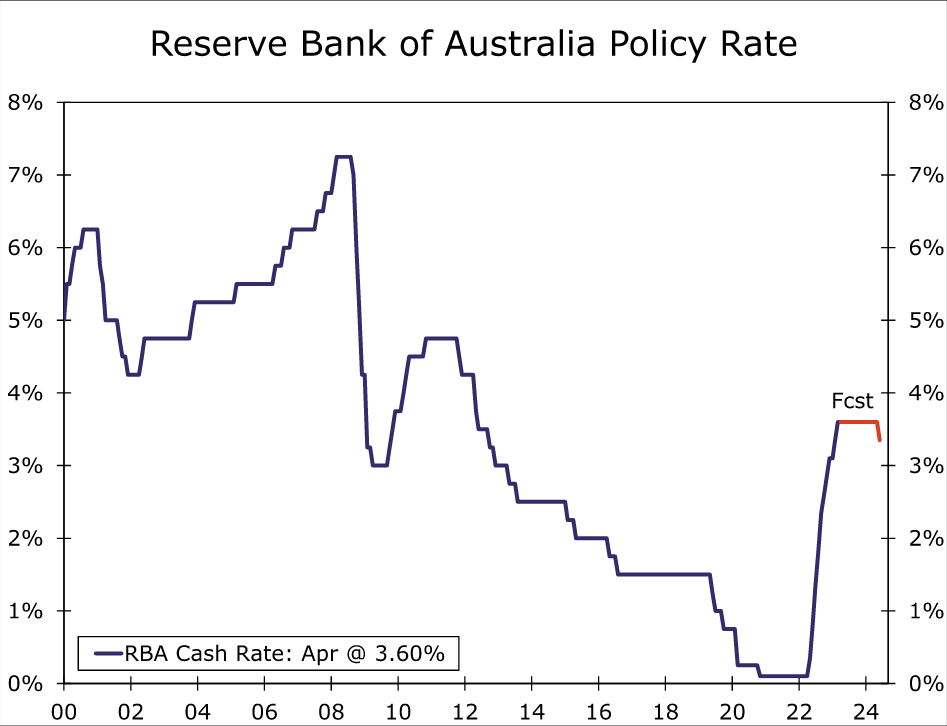

- The Reserve Bank of Australia (RBA) paused its monetary tightening in April, holding its policy rate at 3.60%. The RBA also softened its guidance in regard to further rate hikes, stating that “some” further tightening of monetary policy “may well be needed”.

- In holding policy steady, the RBA cited the cumulative tightening to date, evidence that inflation has peaked, and a cautious outlook for consumer spending. Household fundamentals suggest consumer spending trends will remain distinctly subpar given falling real household incomes and rising household interest costs.

- After the RBA’s pause, we believe the bar to resume rate hikes has risen. That is not a bar we expect to be met. Instead, we expect the current policy rate of 3.60% to be the peak for this cycle, and we do not expect the RBA to begin easing monetary policy until well into 2024.

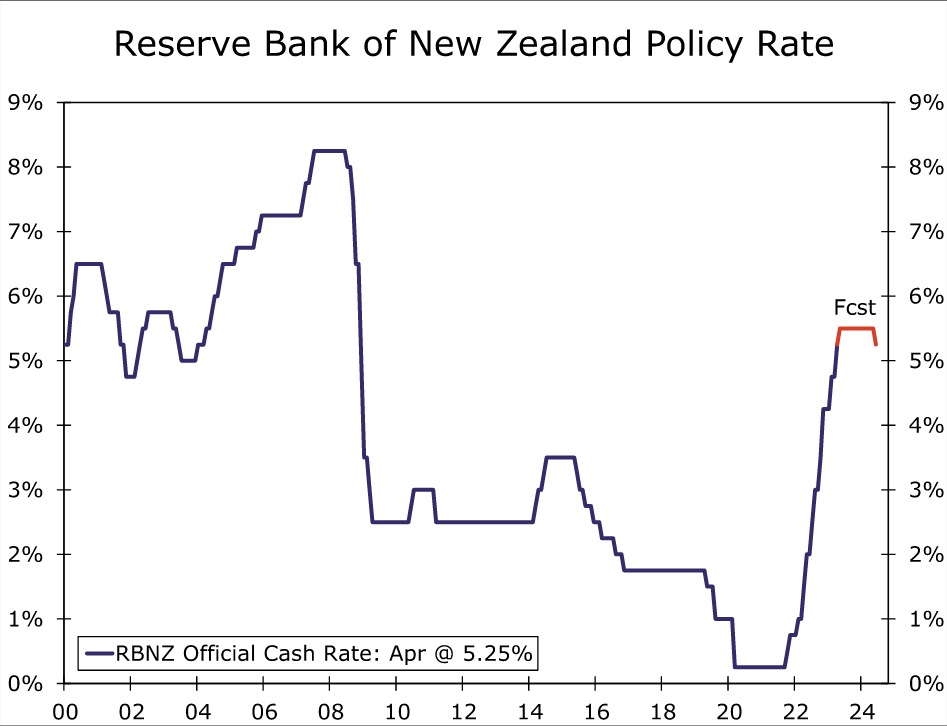

- In contrast with the RBA, the Reserve Bank of New Zealand (RBNZ) was more hawkish than expected at its April monetary policy meeting, delivering a 50 bps rate hike to 5.25%. Policymakers said that inflation is still too high and persistent, while employment is beyond its maximum sustainable level.

- Taking into account the 500 bps of monetary tightening delivered so far in this tightening cycle, the RBNZ anticipates growth to slow in early 2023. Meanwhile on the inflation front, consumer prices have not yet shown signs of receding substantially.

- In our view, moderate growth and elevated inflation sets the backdrop for additional tightening from the RBNZ, although believe the central bank is near the end of its rate hike cycle. We forecast one last 25 bps rate hike in May, bringing the Official Cash Rate (OCR) to 5.50%. However, we would not rule out a larger increase, and note that the risks are tilted toward a 50 bps increase in May.

Reserve Bank of Australia Reaches a Rate Hike Pause

After some 350 bps of rate hikes since May of last year, the Reserve Bank of Australia (RBA) paused its monetary tightening at its April meeting, holding its Policy Rate steady at 3.60%. The RBA acknowledged that monetary policy operates with a lag and the full effect of the past rate increases has yet to be felt. In that context, the April pause offers the central bank additional time to assess the impact of the cumulative increase in interest rates so far.

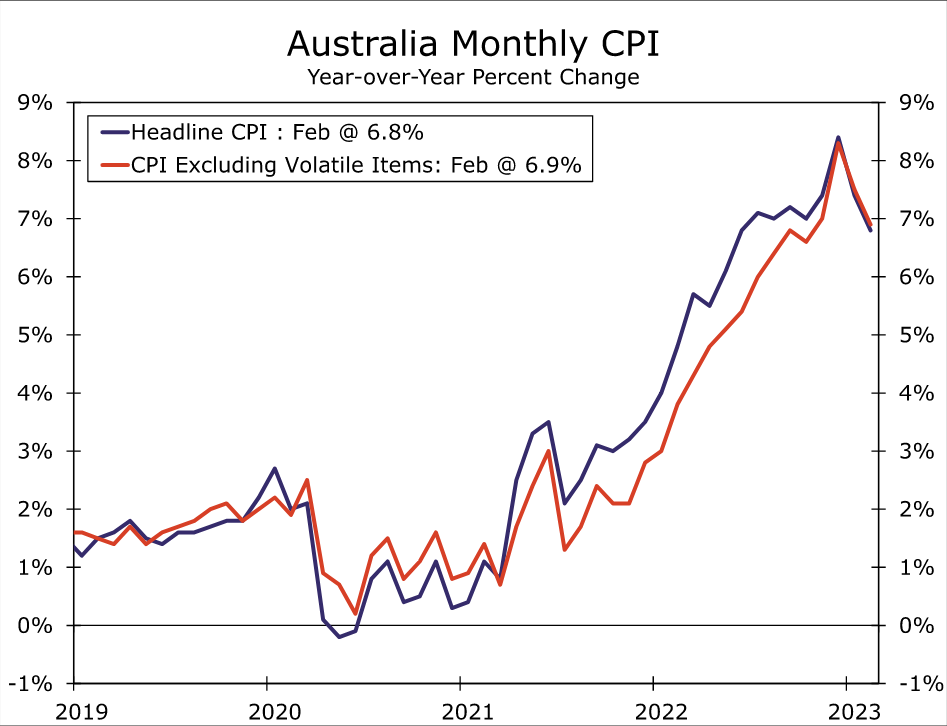

The RBA’s announcement highlighted other factors that contributed to the pause at the April meeting as well. The central bank said there is growing evidence that inflation has peaked, and in particular highlighted the monthly CPI indicator. That measure saw CPI inflation slow to 6.8% year-over-year in February from a recent peak of 8.4% in December. The CPI excluding volatile items also slowed to 6.9%. While inflation is still elevated well above the RBA’s medium-term target range of 2%-3%, the recent slowdown means it is nonetheless heading in the right direction. The RBA expects inflation to decline in 2023 and 2024, reaching around 3% by the middle of 2025.

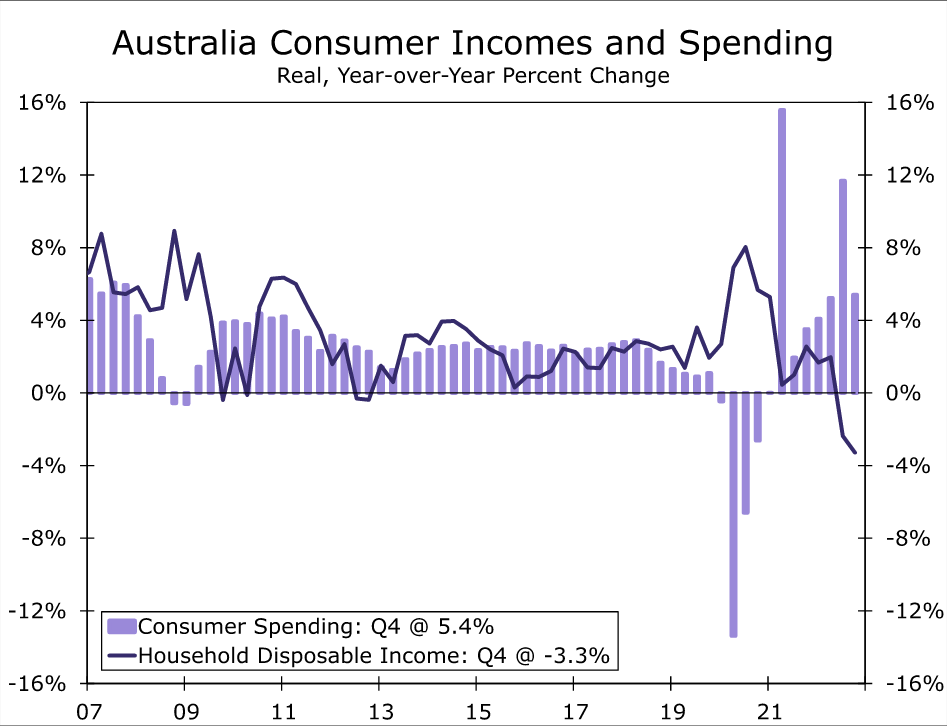

Another factor the RBA has focused on for a few months now and once again in April is trends in the outlook for consumer spending. The RBA said there is “further evidence that the combination of higher interest rates, cost-of-living pressures and a decline in housing prices is leading to a substantial slowing in household spending.” Certainly, our assessment of household sector fundamentals suggest that growth in consumer spending is likely to remain distinctly subpar. Although Australian employment trends have for the most part remained relatively steady and household incomes have risen, those income gains have not kept pace with the rate of inflation. As a result, after adjusting for higher prices, real household disposable incomes were actually down 3.3% year-over-year in Q4-2022. Those income trends are in contrast to trends in real consumer spending, which showed a gain of 5.4% in Q4. Given the underwhelming trends in real household incomes, some further slowing in consumer spending in the quarters ahead also appears likely.

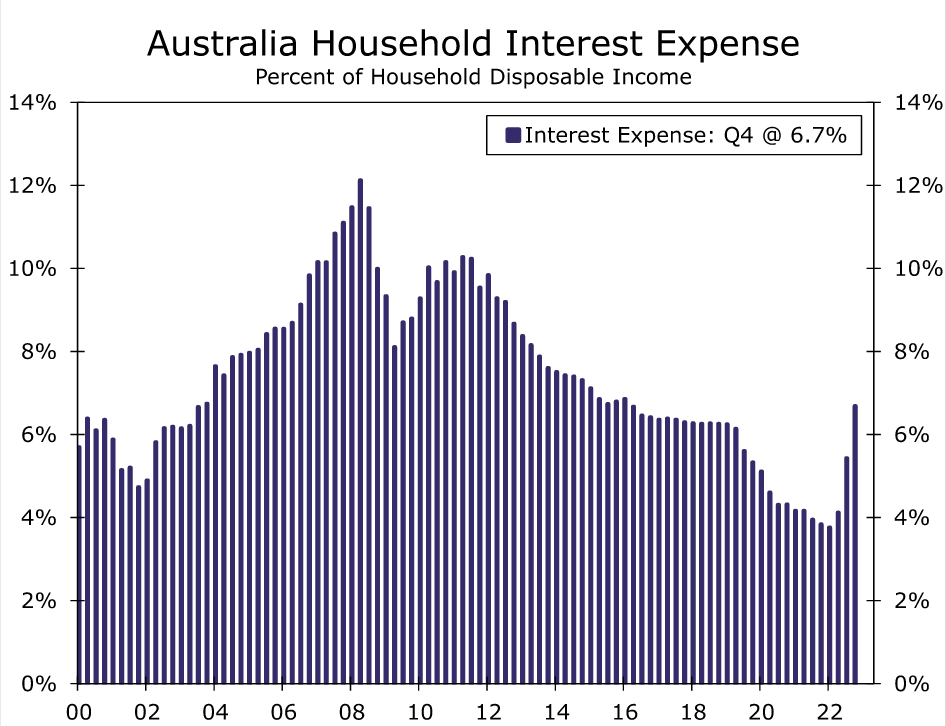

An additional factor that could be a headwind for consumer spending, as alluded to by the RBA, is the cumulative increase in interest rates so far. With a sizable portion of Australian mortgage borrowers on variable, rather than fixed rates, policy rate increases are flowing through fairly quickly to household budgets. Indeed, as a percent of disposable income, household interest expenses have already jumped to 6.7% by Q4-2022 from a low of 3.8% as recently as Q1-2022. With those interest expenses also squeezing household cash flows, they should also prove a restraining factor for consumer spending in the quarters ahead.

Overall, we believe a cautious consumer will be enough to keep the Reserve Bank of Australia on hold for the rest of 2023, at a minimum. To be fair, the RBA’s April announcement also included some more hawkish elements. The central bank acknowledged that the labor market remains very tight and wage growth is firming. In addition, the RBA said it remains alert to the risk of a wage spiral and seeks to guard against higher inflation expectations becoming entrenched. In subsequent comments, RBA Governor Lowe offered comments both for and against further monetary tightening. He said “the decision to hold rates steady this month does not imply that interest rate increases are over,” but also said the RBA “is prepared to have a slightly slower return of inflation to target than some other central banks.” Overall however, after the RBA’s pause and with the central bank having softened its further policy guidance to some extent, saying “some further tightening of monetary policy may well be needed to ensure that inflation returns to target”, we believe the bar is somewhat higher for the Reserve Bank of Australia to resume rate hikes. That is not a bar we expect to be met. Instead, we expect the current policy rate of 3.60% will be the peak for this cycle, and we do not expect the Reserve Bank of Australian to begin easing monetary policy until well into 2024.

Reserve Bank of New Zealand Hawkish But Nearing End of Tightening Cycle

In contrast with the RBA, the Reserve Bank of New Zealand (RBNZ) was more hawkish than expected at its April monetary policy meeting. The RBNZ surprised market participants, delivering an unexpected 50 bps rate hike to 5.25%. Policymakers cited inflation is still too high and persistent, while employment is beyond its maximum sustainable level.

Taking into account the 500 bps of monetary tightening delivered so far in this tightening cycle, the RBNZ anticipates growth to slow in early 2023 but remain positive. Indeed, higher frequency monthly data for the first few months of the year has hinted at recovering growth after a negative GDP print in Q4-2022. For one, consumer spending appears to have rebounded early this year. More specifically, retail card spending, while flat in February, gained 2.6% month-over-month in January, while credit card spending jumped 5.5% and 2.7% month-over-month in January and February, respectively. In our view, resilient consumer spending should keep the economy intact enough to avoid recession this year, even as growth slows.

In addition, while sentiment indicators have not been stellar by any means, they have improved over the past few months. Business confidence, which tracks the general state of the economy as it relates to firms, increased to -43.4 in March from -70.1 in December of last year. Furthermore, PMI survey data has also improved compared to Q4. In encouraging news, the manufacturing PMI moved back into expansionary territory after spending all of Q4 in contraction, reaching 52.0 in February. Meanwhile, the services PMI remained expansionary, moving up to 55.8 from 52.0 in December.

Overall, in our view, steady growth trends in Q1 have set the backdrop for additional monetary tightening from the RBNZ. Notably, in the April announcement, the central bank said a slowdown in spending growth is necessary to return inflation to target over the medium-term. Even though recession is not the base case scenario, given the RBNZ expects a slowdown this year and also believes employment is currently beyond its maximum sustainable level, we do not think the RBNZ will shy away from hiking rates even if growth trends were to worsen.

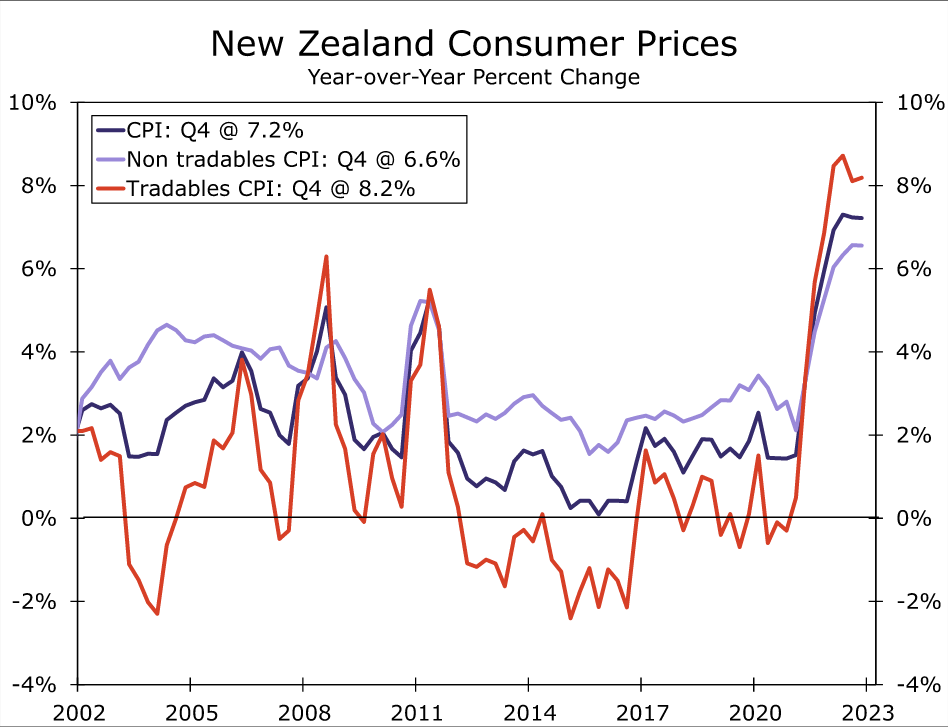

On the inflation front, consumer prices in New Zealand have not yet shown signs of receding substantially. Unlike in Australia, there is no monthly indicator for inflation, so the most recent data is from Q4-2022. At the end of last year, headline CPI remained persistently high at 7.2% year-over-year for the second quarter in a row, after peaking at 7.3% in Q2-2022. And while non-tradables (domestically-oriented) inflation was slightly more contained at 6.6%, tradables CPI was even higher than the headline rate at 8.2%, having ticked back up in Q4. With persistently high inflation in mind, the RBNZ decided on a larger-than-expected rate hike in April.

Policymakers acknowledged they are comfortable that current lending rates faced by businesses and households will help ensure core inflation and inflation expectations begin to moderate. With that said, they noted a risk scenario in which wholesale interest rates, which have fallen significantly in the last two months, could put downward pressure on these lending rates. This risk scenario led policymakers to go with a 50 bps rate hike over a 25 bps hike. In our view, this is a signal that the RBNZ is broadly comfortable with where rates are currently—and indeed, they have already noted that tightening to date implies policy is already contractionary—but they have a preference for maintaining a hawkish approach to ensure interest rates remain high enough to bring down inflation in the longer term. In essence, the central bank appears to be trying to prevent a premature pricing of monetary easing in the form of lower wholesale interest rates and ultimately lending rates for businesses and households.

All in all, we believe the RBNZ is nearing the end of its monetary tightening cycle. Looking forward, we forecast one last 25 bps rate hike in May, bringing the Official Cash Rate (OCR) to 5.50%. However, we would not rule out a larger magnitude hike, and note that the risks are tilted toward a 50 bps increase. Given the RBNZ is expecting to see continued slowing in domestic demand and a more meaningful decline in inflation, we will be closely watching the extent to which incoming growth and inflation data show signs of moderating in assessing the outlook for monetary policy beyond May.

was more hawkish than expected at its April monetary policy meeting. The RBNZ surprised market participants, delivering an unexpected 50 bps rate hike to 5.25%. Policymakers cited inflation is still too high and persistent, while employment is beyond its maximum sustainable level.){kind=link}