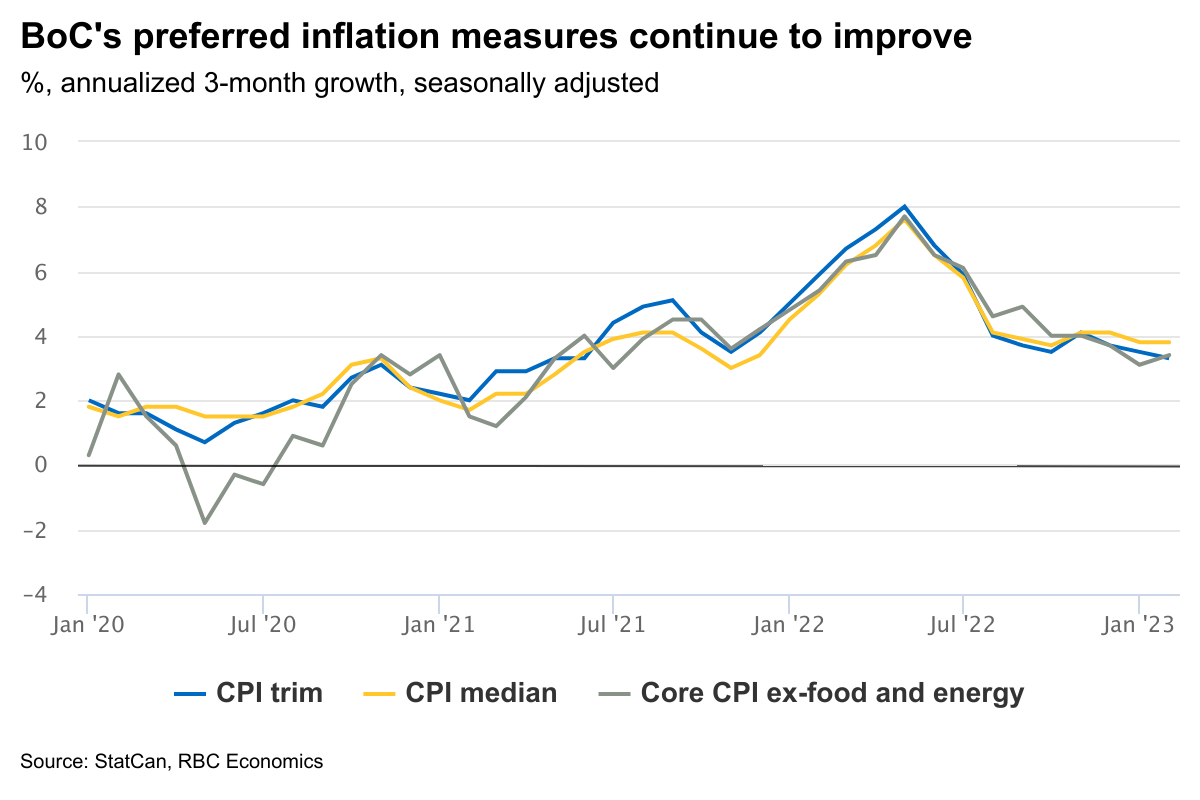

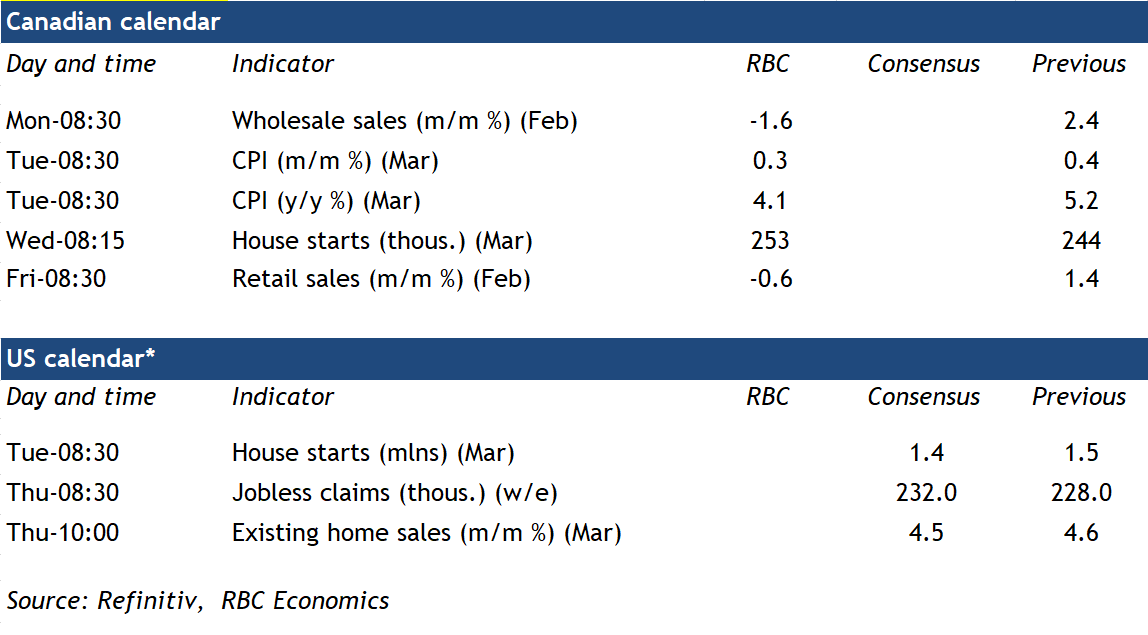

Growth in the Canadian consumer price index likely slowed sharply in March. We expect a deceleration to 4.1% year-over-year growth. That would be a full percentage point down from February and the lowest headline CPI reading since August 2021. Much of that decline is coming from lower energy prices. The price of gasoline was down 13% from March of last year, when the Russian invasion of Ukraine sent oil prices soaring. Food price inflation is still running hot (+9.7% year-over-year in February) but appears to be past its peak with annual growth likely to edge lower for a second straight month. But the breadth of price growth across other products and services has also been narrowing. And growth in the Bank of Canada’s preferred median and trim core CPI measures has slowed to a ~3.5% annualized rate over the three months ending in February (from a peak of 8% in summer of 2022). By our count, a little more than half of the goods and services in the CPI basket were still seeing inflation above the BoC’s 1% to 3% target range over that period, but that’s down from a peak of almost 90% last year.

Inflation is expected to drift even lower. Labour markets (and consumer demand) remained exceptionally firm early in 2023—but rising interest rates and elevated prices are increasingly cutting into household spending power. Delinquency rates on consumer loans are still low but on the rise. A preliminary estimate from StatCan was for a 0.6% decline in retail purchases in February, partially reversing a bigger 1.4% increase in January. And industry reports point to another decline in auto sales in March. Our own tracking of RBC debit and credit card spending has shown early signs of softer spending on discretionary goods. Services spending held up better but data from the Bank of Canada’s latest consumer survey suggests sentiment is softening there as well. We expect the easing in domestic inflation to persist–and for the Bank of Canada to hold the line on further interest rate increases through this year.

Week ahead data watch

We expect Canadian retail sales to edge down 0.6% during that month, in line with StatCan’s early indicator—due mainly to a price-related sales drop at gas stations. StatCan’s advance estimate suggested wholesale trade fell by 1.6% in February, largely driven by a sales decline in the motor vehicle and parts sector.

Canadian housing starts likely increased to 253,000 units in March from 244,000 units in the previous month. Residential building permit issuances have been slowing, with a 3-month rolling average of 248,000 units in February.

but appears to be past its peak with annual growth likely to edge lower for a second straight month. But the breadth of price growth across other products and services has also been narrowing. And growth in the Bank of Canada’s preferred median and trim core CPI measures has slowed to a ~3.5% annualized rate over the three months ending in February (from a peak of 8% in summer of 2022). By our count, a little more than half of the goods and services in the CPI basket were still seeing inflation above the BoC’s 1% to 3% target range over that period, but that’s down from a peak of almost 90% last year.){kind=link}