Summary

Over the last few weeks, headlines around the U.S. dollar losing its global reserve currency status have become widespread and captured attention. In our view, the U.S. dollar is not on the brink of losing global reserve currency status at any point in the foreseeable future. The dollar meets all the characteristics of a reserve currency, and is still the dominant currency in the global payments’ marketplace as well as the currency of choice for FX reserve managers. While the FX reserve allocation to the dollar has declined over time, we believe this trend is a product of one-off developments and not necessarily a movement to shun the greenback. Going forward, we believe the dollar will maintain its status as the global reserve currency as EU fragmentation risks will prevent the euro from gathering momentum, a distorted Japanese Government Bond market counters the yen, and convertibility challenges limits the rise of the renminbi for the time being.

U.S. Dollar’s Reserve Status Is Under False Scrutiny

In recent weeks, the U.S. dollar’s status as the world’s global reserve currency has come under intense scrutiny, with some analysts predicting the demise of the greenback’s reign. Such speculation has occurred in the context of recently announced initiatives such as China and Brazil announcing clearing arrangements in each other’s local currencies, Middle Eastern energy exporting countries agreeing to settle transactions in renminbi, and the BRICS nations announcing plans to develop a single currency to reduce dependence on the U.S. dollar. Still, while such initiatives could at the margin see less use of the U.S. dollar for trade or investment purposes, we see many characteristics which suggest the U.S. dollar will remain the preeminent global currency for the foreseeable future.

To be considered a “reserve currency” a currency must demonstrate certain characteristics. These desirable attributes include being:

- Freely convertible (i.e. not pegged and/or subject to capital controls)

- Widely accepted and used in trade and global transactions

- Backed by large and liquid debt markets easily accessible to foreign investors

- Not subject to undue political influence (i.e. associated with an independent central bank)

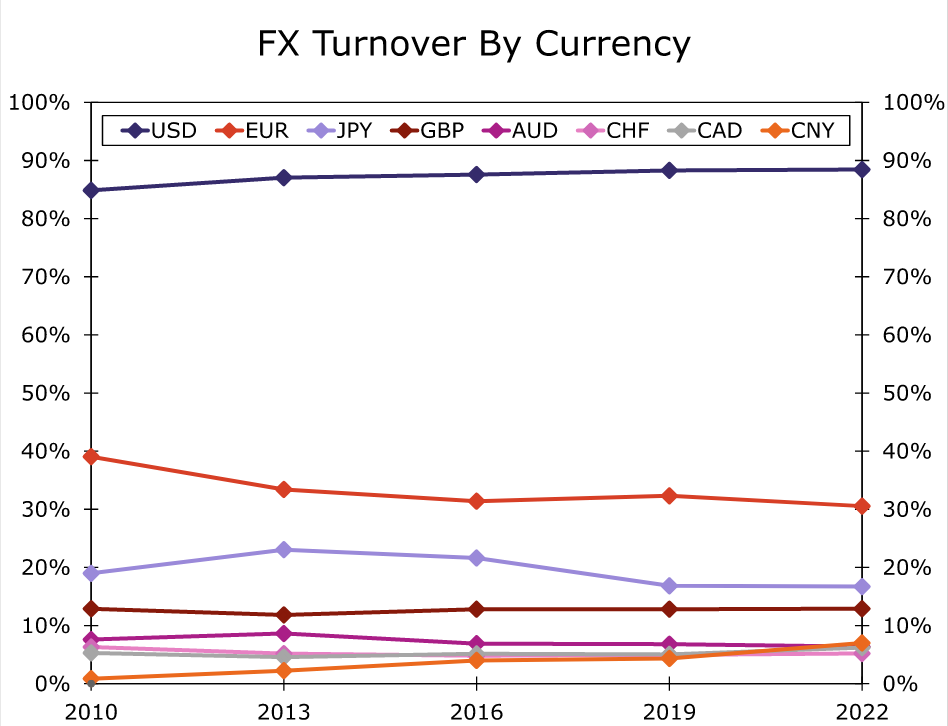

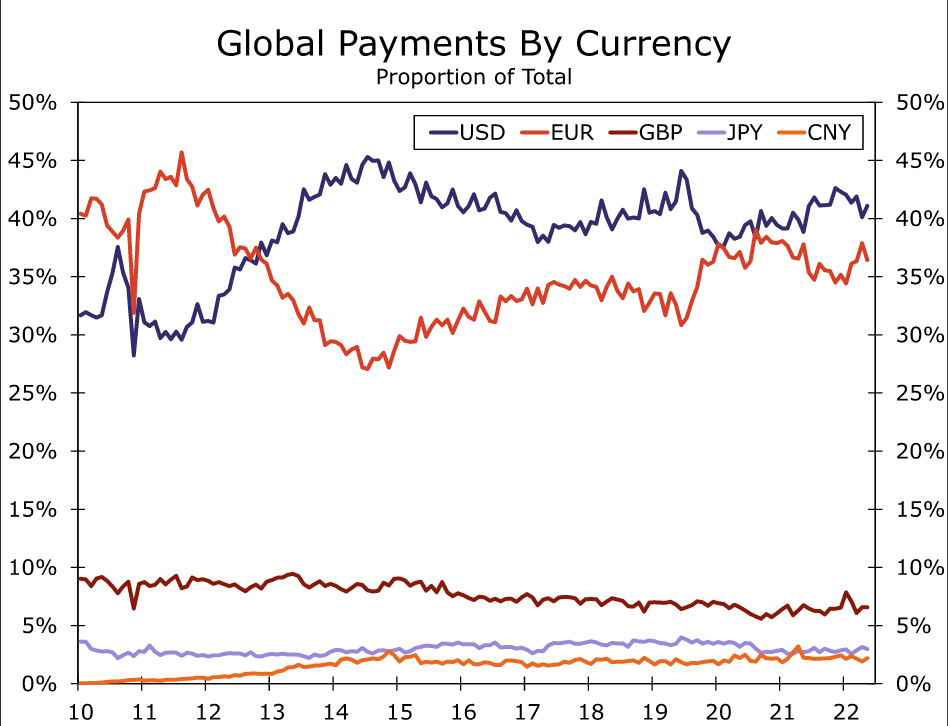

The U.S. dollar measures up well, and certainly better than any other currency, against these metrics, underpinning our view that the dollar’s global reserve currency status will remain intact going forward. To that point, the greenback is the most used currency for trade and other cross-border transactions by a fairly wide margin. According to relevant and available data, no clear evidence exists that U.S. dollar usage is diminishing. According to the Bank for International Settlements (BIS) three-year survey of foreign exchange turnover—which indicate the prevalence of individual currencies across a range of transactions (spot, forward, swaps, options and other products)—the U.S. dollar’s percentage share of FX turnover in April 2022 was 88.4%, which is higher than the 84.9% in April 2010 (Figure 1). Keep in mind given that foreign exchange transactions are two-sided, these percentages add to 200%. This relatively high usage reflects the ease of transacting in U.S. dollars, no convertibility issues, and the dollar’s widespread acceptance around the world. Some distance behind the dollar is the euro at 30.5%; however, euro usage is down notably from 39.0% in April 2010. In fact, aside from the Chinese renminbi, all other key major currencies have seen their usage decline from 2010-2022. In the case of the Chinese renminbi, the yuan only appears in ~5% of total FX turnover. Data from the Society for Worldwide Interbank Financial Telecommunication (SWIFT) confirms the U.S. dollar’s prominence in the global marketplace. SWIFT publishes monthly figures of the proportion of global payments made in each currency. Once again, the U.S. dollar comes out on top, rising to 41.1% of total payments in February 2023 (Figure 2). To be fair, the U.S. dollar is not as dominant on this metric, with 36.4% of payments made in euros in February. However, other currencies such as the British pound, Japanese yen and Chinese renminbi are far behind. We also note that proportion of global payments in U.S. dollar has ranged between 35% and 45% since 2013, and there is no clear evidence of a trend decline of the use of the U.S. dollar in the SWIFT data.

FX Reserve Managers Continue to Choose the Dollar

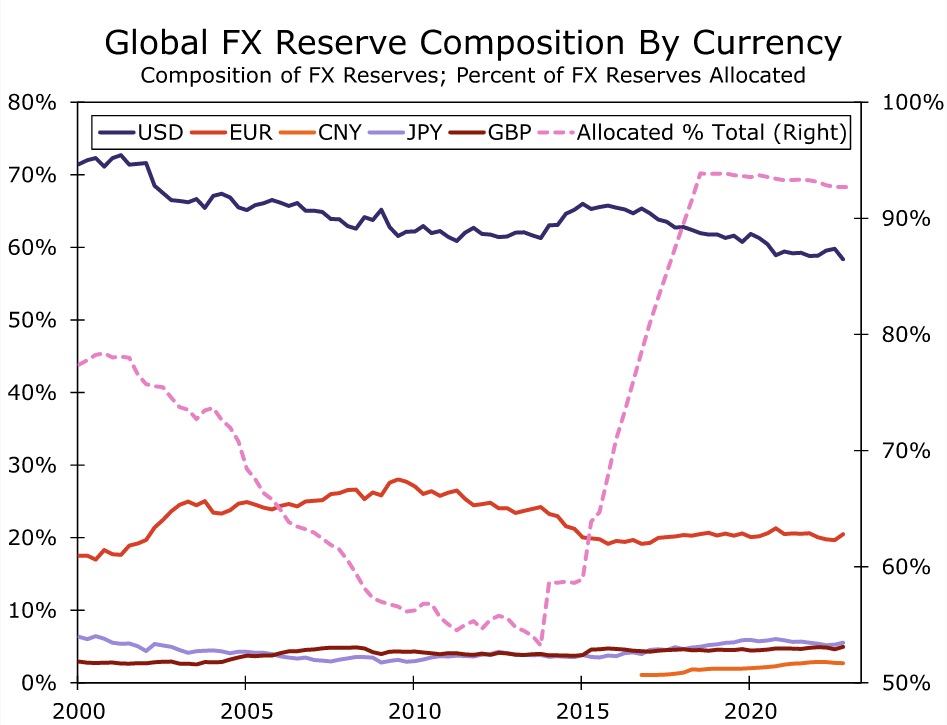

In addition to usage in the global marketplace, the composition of foreign exchange reserves held by central banks around the world continue to be dominated by the U.S. dollar. At the end of 2022, foreign exchange reserve assets totaled US$11.963 trillion, of which the U.S. dollar represented the majority of these global FX reserve assets. According to these IMF data, the U.S. dollar is still the most popular choice of FX reserve managers in managing currency reserves. That said, we acknowledge there has been a gradual shift away from the proportion of FX reserves held in U.S. dollars over the past decades. In Q1-2000 FX reserve managers held 71.5% of global FX reserves in dollars. This number has since fallen to 58.4% by at the end of 2022 (Figure 3).

We see multiple relevant factors that have likely contributed to the gradual decline in the U.S. dollar’s use as a reserve currency during this timeframe. First, the introduction and adoption of the euro in 1999 and early 2000s likely contributed to the dollar’s initial downward trend. To that point, in the immediate years following the introduction of the euro, the decline in U.S. dollar-denominated FX reserves coincides with increasing usage of the euro as a reserve currency. However, holdings FX reserves in euros was a one-off occurrence (albeit a long one) and ran its course around 2010. The second phase of the decline occurred started around 2015 and lasted through 2020; however, we question, or at least cannot say with any certainty, whether the dollar was being shunned or if these dynamics were more statistical in nature. We say statistical in the sense that this was a period when a more robust sample of countries, most notably China, began reporting the composition of their FX reserves to the International Monetary Fund. Starting in 2015 and persisting for a few years, additional central banks became more transparent and a larger allocation of all global foreign exchange reserves became know. In 2018, the IMF was able to report that the currency allocation of 93% of global FX reserves were known, up from just 53% in late 2013 (Figure 3). With China’s massive FX reserve position being included the composition calculation, disentangling whether the dollar’s allocation declined as a result of FX reserve managers moving away from the greenback or whether China’s FX reserves were allocated toward multiple currencies and not just the dollar is a bit of an unknown. Regardless of whether the decline was a product of FX reserve management or a statistical byproduct of changing areas of coverage, most importantly we note that proportion of FX reserves held in U.S. dollars has been stable since late 2020, and still far above the next most used currency by hard currency reserve managers.

Alternatives Are Limited. Dollar’s Status is Secure

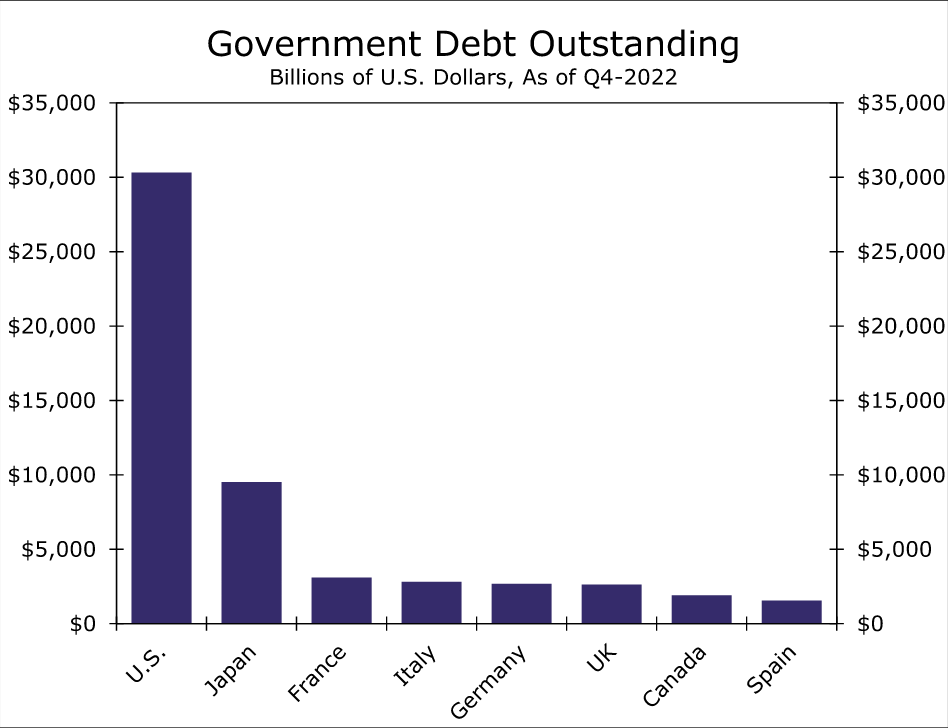

Moreover, we believe there are limits to how much lower, for now, the use of the U.S. dollar by FX reserve mangers can go. As we stated earlier, a desirable characteristic of a global reserve currency is one that is easily and freely tradable, as well as backed by large and liquid debt markets. Using data from the Institute of International Finance (IIF), government debt outstanding for the United States (US$30.3 trillion) and Japan (US$9.5 trillion) comfortably exceed the size of other major government bond markets (Figure 4). This should make those bond markets and their respective currencies popular choices for FX reserve managers, more so the case for the United States. For Japan, the government bond market has been, and continues to be, significantly distorted by the central bank’s Yield Curve Control policy. In addition, the Bank of Japan holds a significant majority of all outstanding Japanese Government Bonds, and yields of Japanese debt remain quite low. While the independence of the Bank of Japan is not in question, the accessibility of the JGB market to foreign investors is something of a challenge and will likely limit the yen’s ability to make significant headway toward becoming the dominant global reserve currency. In Europe, sovereign debt markets are sizable, although still not nearly as sizable as the U.S. or Japan, and in that sense are somewhat segmented. Fragmentation is also a relevant regional risk and one that has gathered momentum since the euro was adopted. Brexit—the risk of Frexit, Grexit, Italexit, Spexit and other percolating EU-fragmentation movements as well as further U.K.-EU tensions—in our view, are enough for FX reserve managers to at least pause when considering allocating an outsized amount to European government bonds. And finally, with respect to Chinese government bonds, capital controls as well as the managed nature of the renminbi and convertibility concerns should offer disincentive for reserve managers to allocate currency holdings toward Chinese assets at this point. Taking these factors into account, we see limited alternatives at the current juncture for FX reserve managers to U.S. government bonds and, accordingly, see limits as to how much lower holdings of U.S. dollar assets by reserve managers will go. With the use of the U.S. dollar for trade and other cross border transactions still widespread, and the use of U.S. dollar assets still a clearly favored choice of reserve managers, we view the U.S. dollar’s status as the global reserve currency as secure for the foreseeable future.

{kind=link}