Following the FOMC and ECB decisions last week, the central bank torch will now be passed to the BoE, which will deliver its decision on Thursday. A 25bps hike is mostly priced in, so the spotlight will fall on clues and hints on how officials are planning to move forward. The US CPIs will also attract special attention as investors are trying to figure out whether the Fed will pause or hike once more in June.

Will the BoE hint at more hikes?

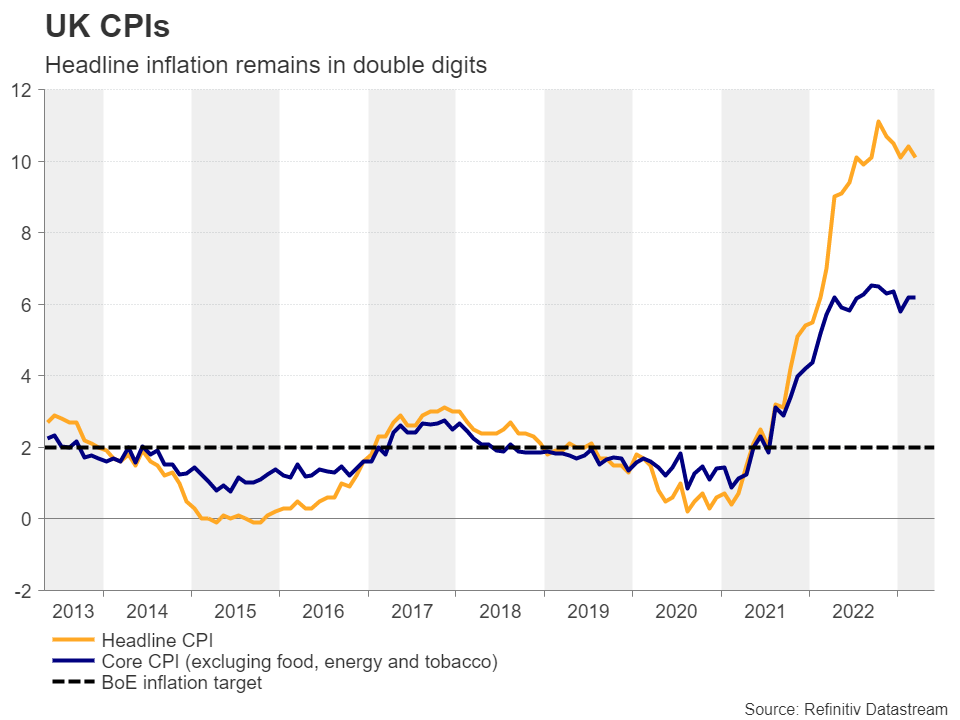

At its latest meeting in March, the BoE raised interest rates by 25 basis points, marking the 11th consecutive hike for this Bank. However, officials played down the surprise surge in inflation during February and maintained a careful view regarding their future course of action, saying that further tightening would be required if there is evidence of more persistent price pressures.

Since then, data showed that inflation slowed by less than expected, with the headline year-over-year rate staying fractionally above 10%, which is allowing investors to price in around 60bps worth of additional rate increases until the end of this year. For this gathering, they are assigning a nearly 85% chance for another quarter-point hike, with the remaining 15% pointing to no action.

Therefore, a 25bps hike by itself is unlikely to shake the pound. Any market reaction may come from the statement, the minutes and/or the updated economic projections. Back in February, the Bank projected that CPI inflation would end the first quarter at 9.7% and slow to 3.0% in 12 months. So, revising higher, or even maintaining that same path may allow investors to continue pricing more hikes, even if officials repeat the same cautious guidance.

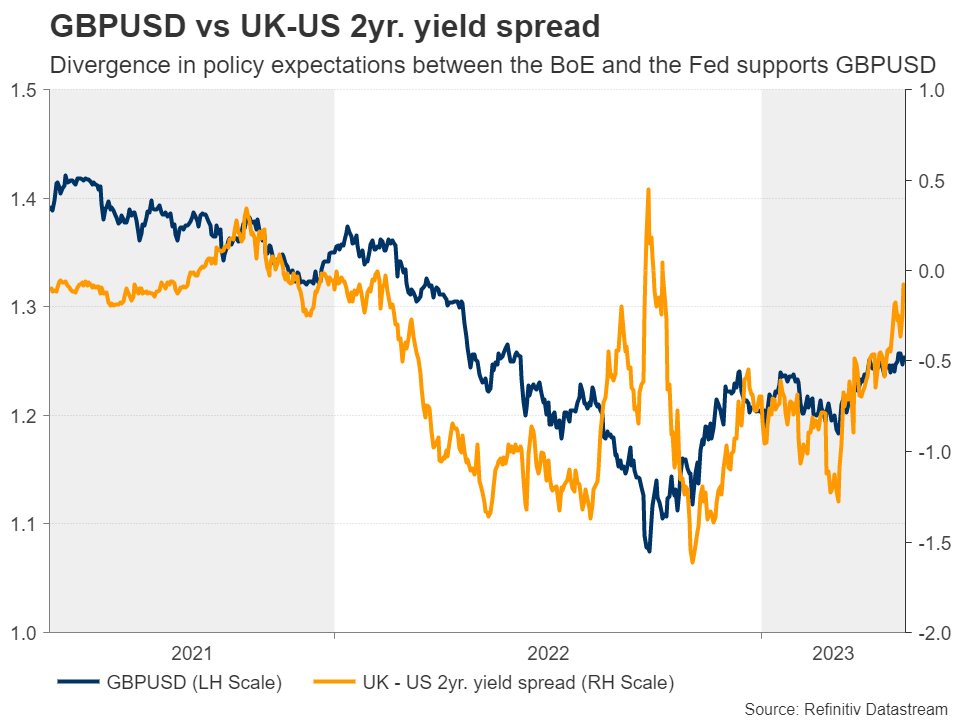

With the Fed expected to cut rates by around 75bps by the end of the year, the path of least resistance for pound/dollar will likely remain to the upside, even if a reiteration of the prior guidance results in a small setback. What could distort the outlook may be a larger-than-expected slowdown in the first estimate of the UK GDP for Q1, which is scheduled to be released on Friday, alongside the nation’s trade data for March.

Will the US CPI numbers spark speculation for a June hike?

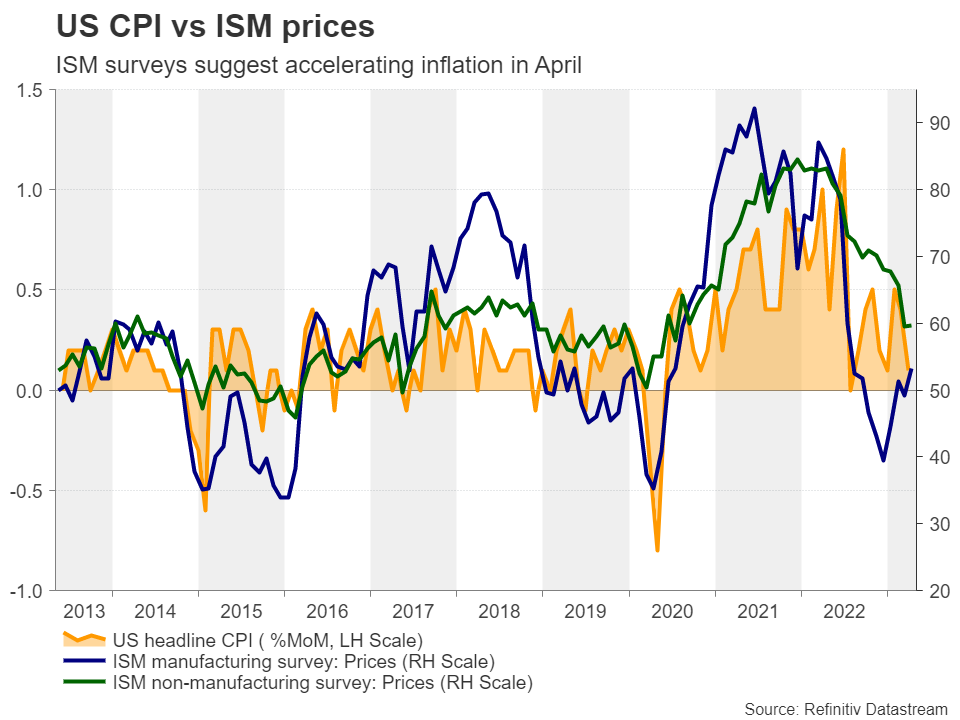

In the US, the highlight will probably be the US CPI numbers for April, due out on Wednesday. The headline rate is forecast to have rebounded to 5.2% y/y from 5.0%, while the core one is expected to have held steady at 5.6% y/y, more or less confirming the ISM and S&P global PMI surveys, which showed that output prices accelerated during the month.

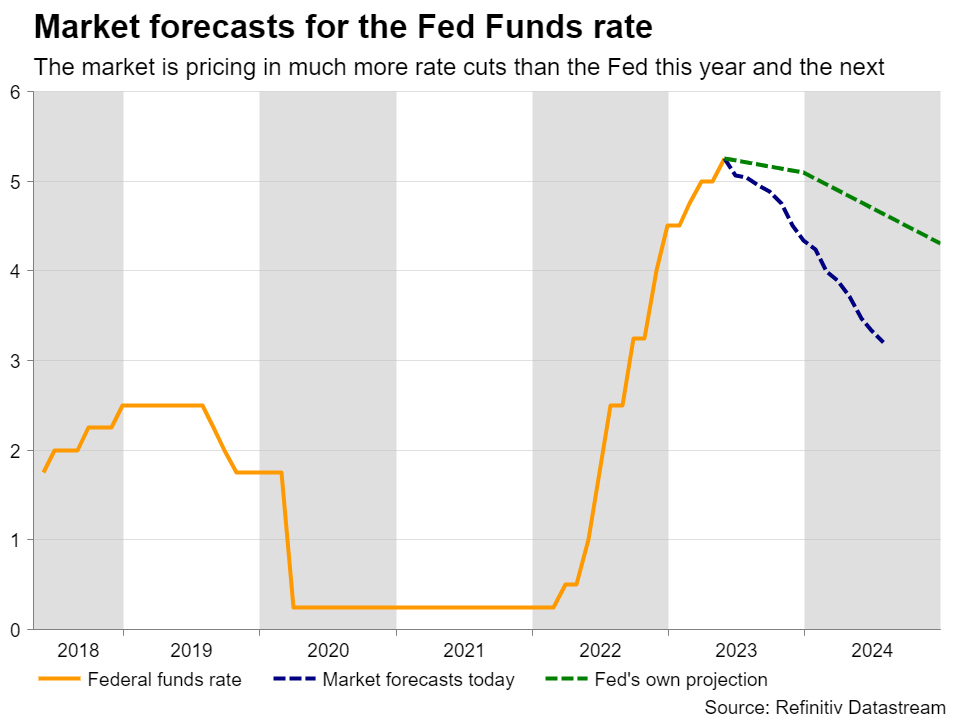

However, such results are unlikely to spark strong speculation about a potential Fed hike in June. After all, the PMI reports were available ahead of Wednesday’s FOMC decision, and yet, even after Powell refused to close the door to a June hike, investors are still pricing in a 90% probability for no action, with the remaining 10% pointing to a quarter-point cut. They are also expecting more than 75bps worth of rate reductions towards the end of the year.

For the pricing to change and start indicating a decent probability for another hike in June, a strong upside surprise may be needed. That could add fuel to the dollar’s engines, but calling for a bullish reversal may still be premature. For a full-scale reversal to start being examined, inflation must continue to accelerate, data may need to reveal that the US economy is in a better shape than many are anticipating, and the Fed might need to prove market expectations wrong, either by raising rates in June or by keeping them untouched through and beyond summer.

China trade data and BoJ Summary of Opinions also on tap

Flying to Asia, China’s trade data, due out on Tuesday, may attract some attention from aussie and kiwi traders, as the world’s second largest economy is the main trading partner of both Australia and New Zealand. Following this week’s disappointing PMIs, weak trade data could corroborate the idea that after the post-reopening boost, the engines of the Chinese economy are now struggling to gather momentum. China’s CPI and PPI numbers are coming out on Thursday.

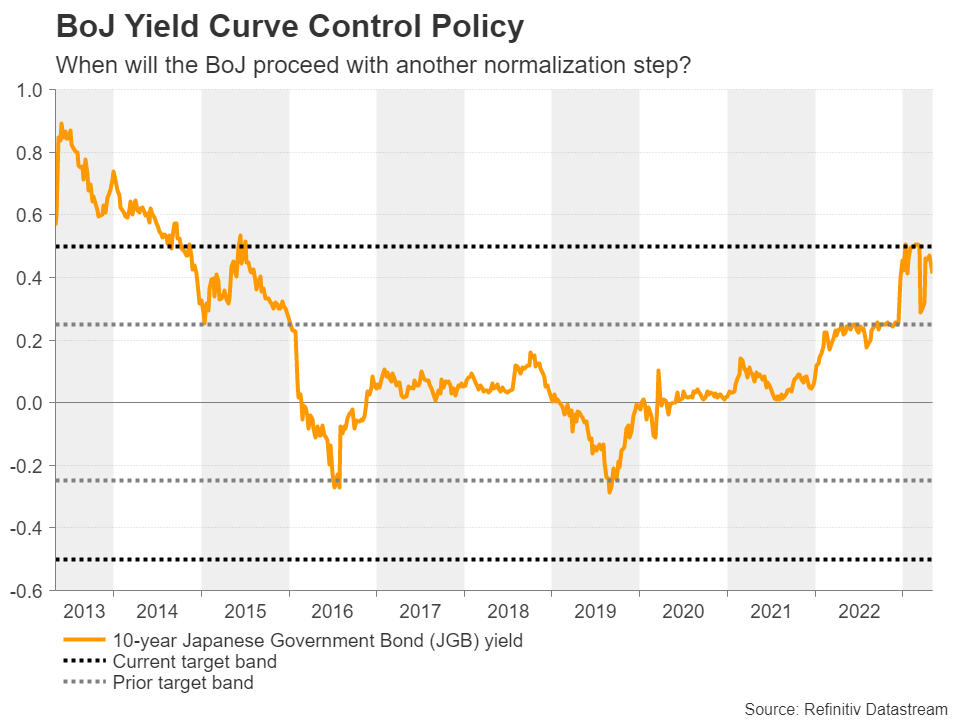

Regarding Japan and the yen, traders could pay some attention to the BoJ’s Summary of Opinions, as this would be the summary concerning the first gathering under Kazuo Ueda’s leadership. At that meeting, officials decided to keep their policy settings unchanged, and although they removed the pledge to keep interest at “current or lower levels”, they decided to conduct a monetary policy review with a planned time frame of around one and a half years.

The yen tumbled at the time of the announcement as the review’s time frame may have raised some speculation that the Bank is unlikely to proceed with any changes during that period. However, with no clear clues on when the Bank may proceed another normalization step, traders may dig into the summary to see whether there is still a chance for that to happen before the end of the year.

{kind=link}