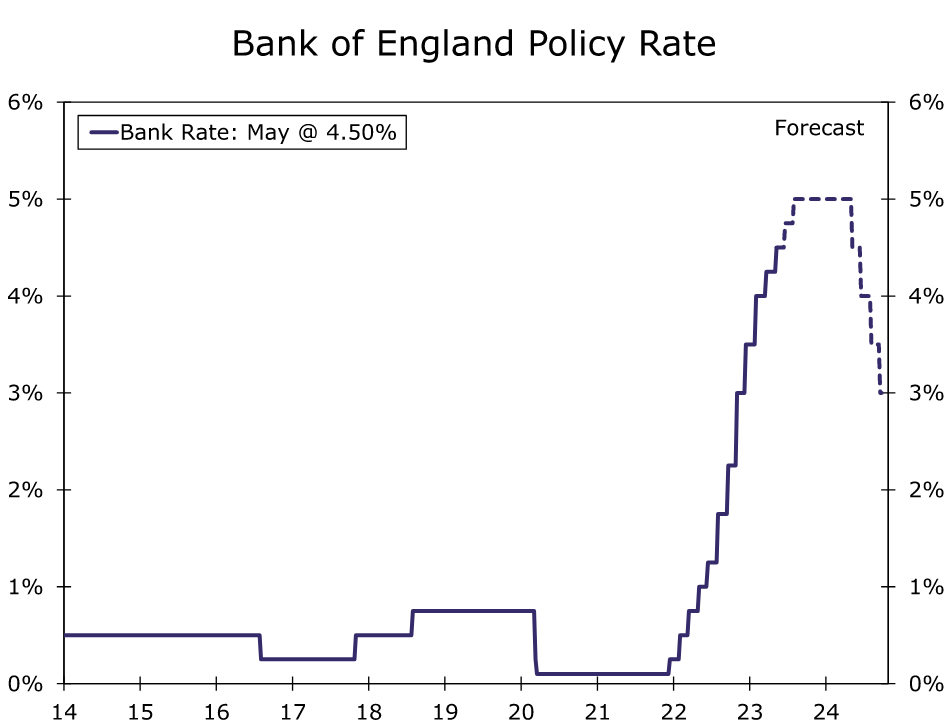

Summary

The U.K.’s April CPI data surprised to the upside, with headline inflation and energy prices receding less than expected. Perhaps even more importantly, for now underlying price pressures still appear to be intensifying as both core inflation and services inflation quickened. In our view, elevated wage growth should keep underlying inflation trends elevated in the near term. With U.K. inflation dynamics remaining firmer than expected, we now anticipate the Bank of England (BoE) will deliver more monetary tightening than previously. Specifically, we expect the central bank to raise rates 25 bps at both its June and August meetings, which would see the policy rate peak at 5.00%. We also expect ongoing price pressures to discourage the BoE from easing monetary policy prematurely, and now forecast the Bank of England to begin lowering interest rates in Q2-2024, one quarter later than our previous forecast.

U.K. Inflation Remains Too High For Comfort

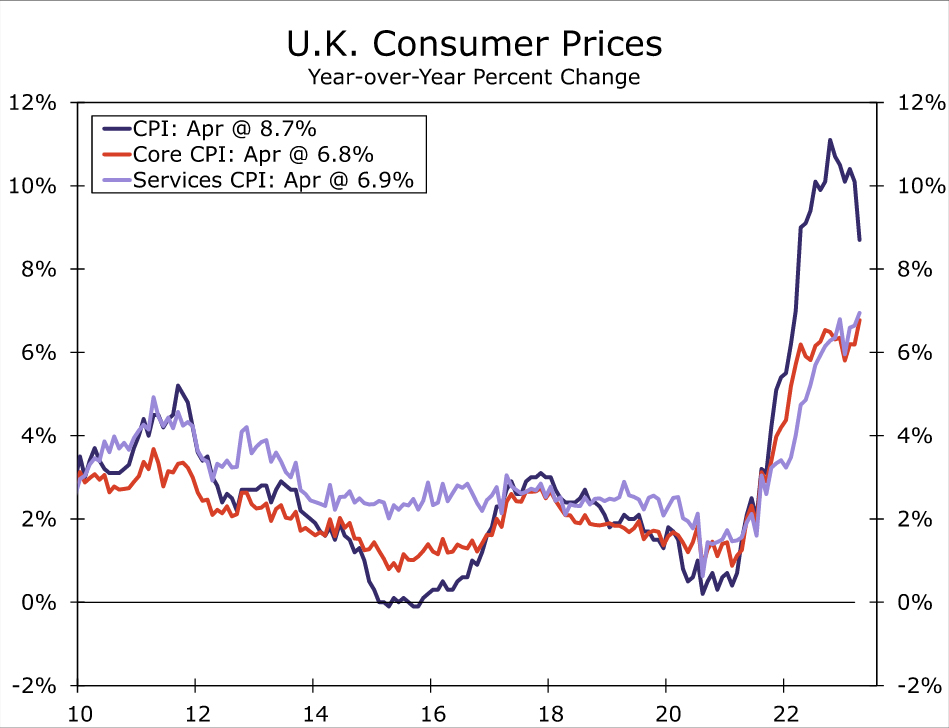

The U.K. April consumer price index was an unpleasant surprise for Bank of England policymakers, and the U.K. public in general. Headline inflation slowed and energy prices receded, albeit by much less than expected. The headline CPI slowed from 10.1% year-over-year in March to 8.7% in April, but that was still well above the 8.2% consensus forecast. Perhaps even more problematic were continued, and indeed intensifying, signs of underlying price pressures. The core CPI quickened sharply and unexpectedly to 6.8%, while services inflation also firmed to 6.9%.

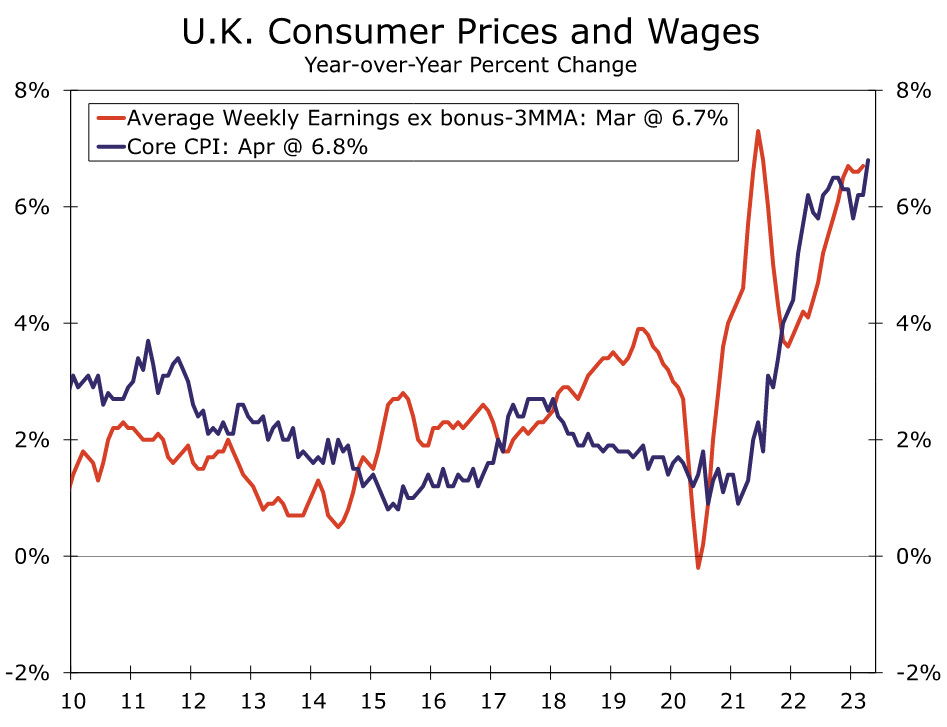

Today’s inflation print is not the only wage or price release that has offered reason for concern in recent months. The U.K. labor market has remained quite resilient to date, meaning that wage inflation remains elevated and has shown little slowing to date. Employment for the January-March period was 182,000 higher than employment during October-December, while the unemployment rate for the first quarter was 3.9%, rising gradually from the low point of 3.5% seen in mid-2022. Against this backdrop wage growth remains elevated. For the January-March period, average weekly earning excluding bonuses rose 6.7% year-over-year, a pace of wage inflation that could see underlying inflation pressures persist for the time being.

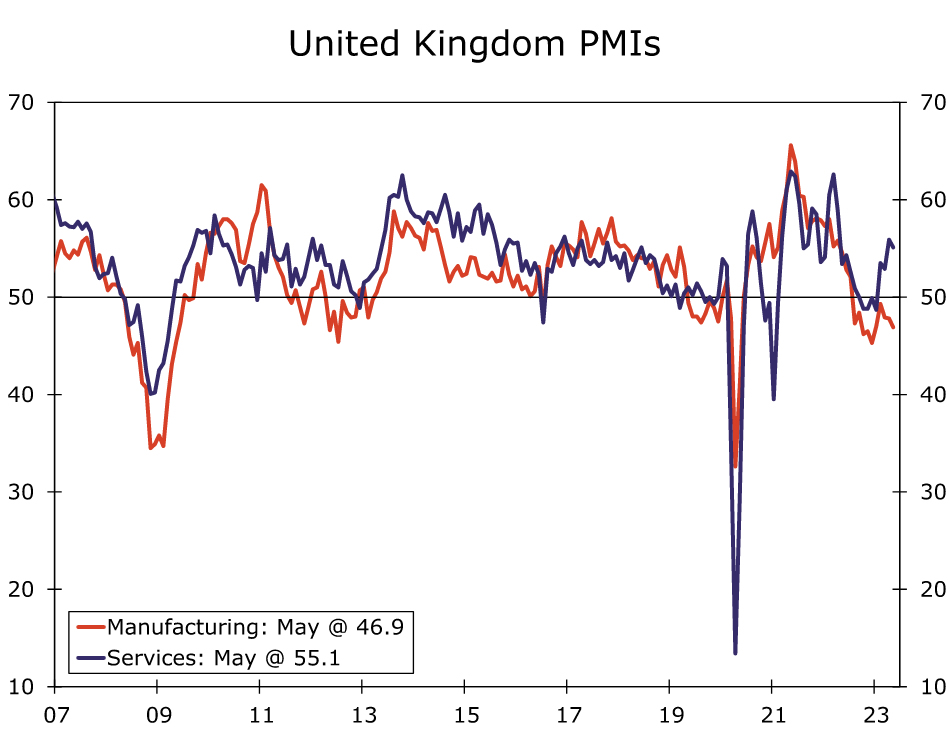

Moreover, it is not just price trends that have printed on the firmer side. Recent news on U.K. economic activity, while far from robust, have shown some resilience. U.K. Q1 GDP rose 0.1% quarter-over-over and 0.2% year-over-year, with the details showing consumer spending flat quarter-over-quarter and business investment rising by 0.7%. Recent survey data suggest that growth could continue into the second quarter. The May manufacturing and service sector PMIs both fell to 46.9 and 55.1 respectively, but the services PMI in particular remains at levels consistent with continued growth. We recently turned slightly more constructive on the U.K. economic outlook. We no longer forecast a recession this year, and expect U.K. GDP growth of 0.2% in 2023.

Expect More Rate Hikes From the Bank of England.

In its monetary policy announcement in early May, the Bank of England (BoE) raised its policy rate to 4.50%, made significant upwards revisions to its growth outlook, and projected inflation to fall below its 2% target over the medium-term. However, the BoE also said it “continues to judge that the risks around the inflation forecast are skewed significantly to the upside, reflecting the possibility that the second-round effects of external cost shocks on inflation in wages and domestic prices may take longer to unwind than they did to emerge.” With respect to policy guidance, the Bank of England said it would “continue to monitor closely indications of persistent inflationary pressures, including the tightness of labour market conditions and the behaviour of wage growth and services price inflation. If there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required.”

Taken together, recent wage and price data in particular, and to a lesser extent recent activity data, point to evidence of more persistent price pressures. As a result, we now expect the Bank of England to raise its policy rate at both its June 22 and August 3 announcements, with would see the policy rate peak at 5.00% for the current cycle. We suspect it will not be until after the August announcement that either U.K. interest rates are high enough, or that central bank policymakers are sufficiently convinced that inflation is heading sustainably back towards its 2% target. We also expect that ongoing price pressures will discourage the BoE from easing monetary policy prematurely, We now forecast the Bank of England to begin lowering interest rates in Q2-2024, one quarter later than our previous forecast for rate cuts to begin in the first quarter of next year.

will deliver more monetary tightening than previously. Specifically, we expect the central bank to raise rates 25 bps at both its June and August meetings, which would see the policy rate peak at 5.00%. We also expect ongoing price pressures to discourage the BoE from easing monetary policy prematurely, and now forecast the Bank of England to begin lowering interest rates in Q2-2024, one quarter later than our previous forecast.){kind=link}