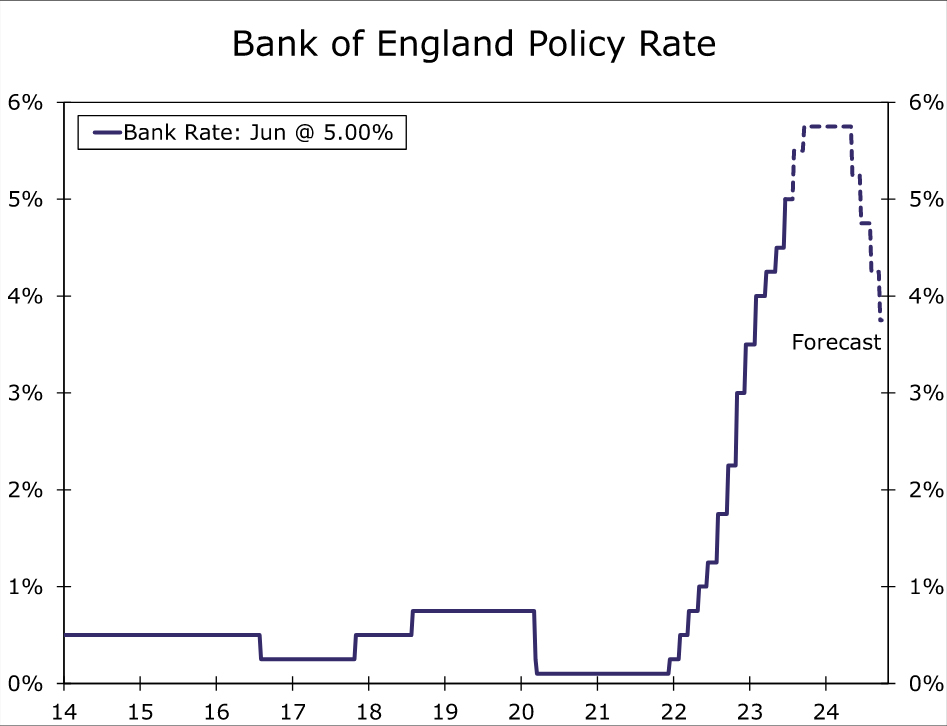

- In the wake of disappointing inflation news in recent months, the Bank of England (BoE) today decided to deliver a large 50 bps policy rate hike to 5.00%.

- In raising interest rates, the BoE said “the second-round effects in domestic price and wage developments generated by external cost shocks are likely to take longer to unwind than they did to emerge” and that if “there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required.”

- We doubt wage or price inflation will cool substantially by the time of the Bank of England’s August announcement. With the BoE’s economic projections in August likely to show much higher inflation forecasts, we expect the U.K. central bank to deliver another 50 bps rate increase, to 5.50%. Beyond that, we also see a 25 bps hike to 5.75% in September, which we expect to be the peak for the current cycle.

- The Norges Bank also raised its policy rate 50 bps to 3.75% and the Swiss National Bank raised its policy rate 25 bps to 1.75%. We expect both central banks to raise rates further through September, while we also think the risk of more extended ECB monetary tightening is rising.

U.K. Delivers A Large June Rate Increase

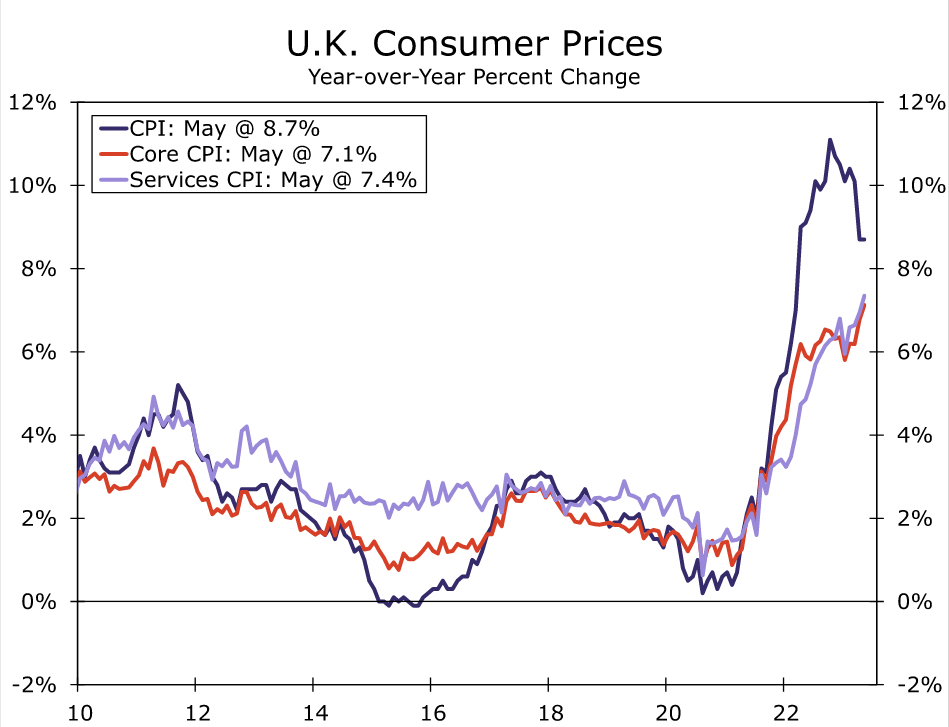

In the wake of disappointing inflation news in recent months, the Bank of England (BoE) today decided to deliver a large 50 bps policy rate hike to 5.00%. The rate hike was large relative to the past couple of meetings, which had seen 25 bps increases delivered, and also relative to the consensus forecast which had called for a 25 bps hike. The BoE’s hand was essentially forced by especially rapid inflation in recent months, which saw the May headline CPI hold steady at 8.7% year-over-year, and core CPI inflation accelerate further to 7.1%.

In raising interest rates today by a 7-2 vote (with the two dissenters voting for no rate change), BoE policymakers said “the second-round effects in domestic price and wage developments generated by external cost shocks are likely to take longer to unwind than they did to emerge. There has been significant upside news in recent data that indicates more persistence in the inflation process, against the background of a tight labor market and continued resilience in demand.”

In addition, policymakers said they would “continue to monitor closely indications of persistent inflationary pressures in the economy as a whole, including the tightness of labor market conditions and the behavior of wage growth and services price inflation. If there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required.”

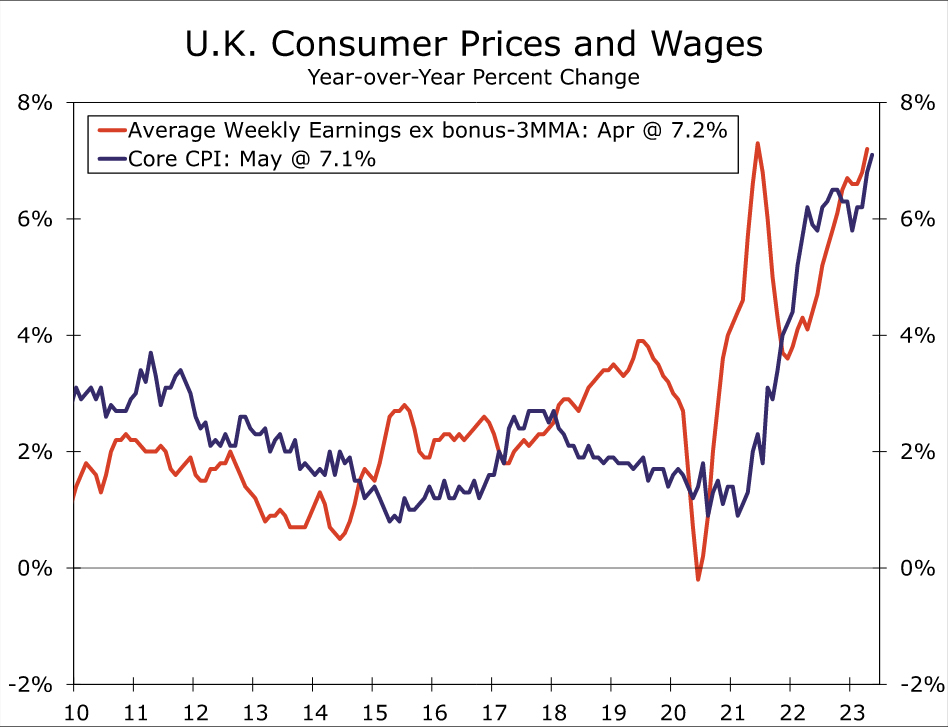

For now, wages continue to grow at a particularly rapid pace, with average weekly earnings ex bonuses for the three months to April rising 7.2% year-over-year. That is a pace of wage growth that does not augur well for a significant near-term slowing in underlying inflation trends. Employment also remains solid for now, and the unemployment rate remains quite low. Against this backdrop, we suspect the BoE will receive further indications of persistent inflation pressures that will require further monetary tightening. Between now and the BoE’s August meeting we will receive one more CPI report and one more labor market report, which we doubt will show a sharp cooling in wage or price pressures. With the BoE’s economic projections in August likely to show much higher inflation forecasts, we expect the U.K. central bank to deliver another 50 bps rate increase, to 5.50%. Beyond that, we also see a 25 bps hike to 5.75% in September, which we expect to be the peak for the current cycle.

With the Bank of England set to raise rates substantially further, we expect the U.K. economy to come under renewed pressure by late 2023, and look for growth to either stagnate or even for the economy to contract. Indeed, given still high inflation and rising interest rates, we now expect a mild recession, forecasting U.K. GDP to contract in Q4-2023 and Q1-2024. In terms of our full year GDP growth outlook, we forecast modest U.K. GDP growth of 0.2% for 2023 and 0.4% for 2024. But only once there are clearer signs of a growth slowdown and a deceleration of inflation, do we believe those factors will convince the Bank of England to bring its tightening cycle to an end. While we do not expect Bank of England rate cuts until Q2-2024, against a backdrop of mild recession and a more quickly declining inflation, we forecast a cumulative 250 bps of rate cuts next year, an aggressive pace of monetary easing that would broadly match that of the Federal Reserve. For the U.K., a low growth/high inflation mix, combined with an outlook for aggressive Bank of England easing next year, are reasons we remain cautious on the pound’s prospects versus the greenback over the medium-term.

Europe’s Other Central Banks Also Active

The Bank of England was not the only central bank in the spotlight today. The Norges Bank raised its policy rate a larger-than-forecast 50 bps to 3.75%, saying inflation and wage growth remain high, and that a higher policy rate than previously signaled is need to bring inflation down to target. The central bank also said another rate increase is likely in August, and signaled a peak policy rate of 4.25%. In keeping with that guidance, for the Norges Bank we now expect 25 bps rate increases in August and September, for a peak policy rate of 4.25%.

The Swiss National Bank (SNB) also raised its policy rate by 25 bps, as expected, to 1.75%. Even as the SNB lowered its near-term inflation forecasts, it projected medium-term inflation at or slightly above its 2% inflation target over the medium term. Specifically, the SNB forecast CPI inflation of 2.2% for 2024 and 2.1% for 2025. Against this backdrop the SNB said it “cannot be ruled out that additional rises in the SNB policy rate will be necessary to ensure price stability over the medium term.” We expect the Swiss National Bank will raise its policy rate another 25 bps to 2.00% in September.

Finally, although the European Central Bank (ECB) was not active this week, we do believe the risk of more extended monetary tightening is rising. Currently, we forecast a final 25 bps rate hike to 3.75% in July—a move that has already been clearly signaled by ECB President Lagarde. However, it may be that additional favorable CPI readings (such as the downside surprise for the May CPI) will be required to dissuade the ECB from further tightening. In contrast, if underlying pressures were to remain persistent in coming months, and we do not see a perceptible shift to a less hawkish ECB outlook at the July announcement, we would be inclined to adjust our ECB monetary policy outlook to also include a 25 bps rate increase in September, to 4.00%.

today decided to deliver a large 50 bps policy rate hike to 5.00%. The rate hike was large relative to the past couple of meetings, which had seen 25 bps increases delivered, and also relative to the consensus forecast which had called for a 25 bps hike. The BoE's hand was essentially forced by especially rapid inflation in recent months, which saw the May headline CPI hold steady at 8.7% year-over-year, and core CPI inflation accelerate further to 7.1%.){kind=link}