Markets have been left somewhat bruised from a fresh round of hawkish gunfire from central bank chiefs, so nerves are running high ahead of the June jobs report out of America. The ISM PMIs and the Fed meeting minutes are also expected to send speculation about a July rate hike into overdrive. However, Australia’s Reserve Bank might decide against raising interest rates thrice in a row. The yen, meanwhile, will be hoping that Japanese data will provide some relief from its selloff.

Can NFP report and ISM PMIs lift the rate path fog?

Investors are being dragged kicking and screaming by policymakers to come round to the thinking that monetary policy tightening has still some way to go. But there was some progress over the last week for the Fed’s Jay Powell and his European counterparts, who once again made the case for ‘higher for longer’.

For Powell, the job of convincing the markets has been somewhat harder as inflation poses less of a threat in America right now than it does in Britain and the Eurozone. However, the Fed is unlikely to be satisfied until it sees clear signs that the labour market is becoming less tight and wage growth is slowing.

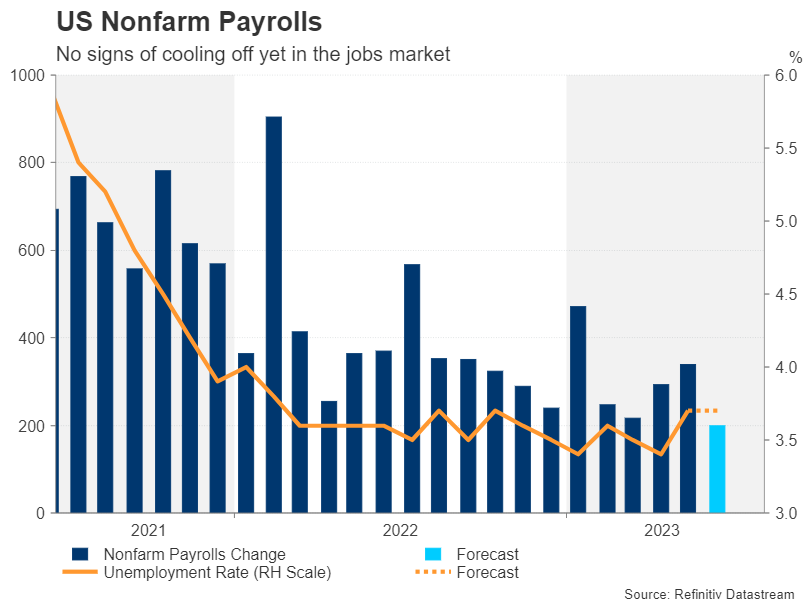

Nonfarm payrolls jumped by 339k in May, blowing past expectations, and even though the unemployment rate spiked up, all the indications are that the US labour market continues to sizzle. The projection for June is a figure of 200k – consistent with recent months’ forecast range. The jobless rate is expected to remain at 3.7%, while average hourly earnings are forecast to have risen by 0.3% m/m in June, unchanged from the prior month.

Unless there is a big shock in the data – either positive or negative, the report may not produce a decisive enough result that could steer policymakers in a specific direction. Hence, investors will also be looking at the other releases of the week, particularly the ISM manufacturing and non-manufacturing PMIs on Monday and Thursday, respectively. A further deterioration in the ISM surveys in June could revive recession fears after Powell played down the prospect in a panel discussion organized by the ECB in Portugal.

Factory orders due Wednesday and the ADP employment survey on Thursday will also be watched. US markets will be closed on Tuesday for the 4th of July Independence Day celebrations. The minutes of the Fed’s June policy meeting will be important too on Wednesday, although with Powell having made two major public appearances since, it’s unlikely the minutes will offer any new insight.

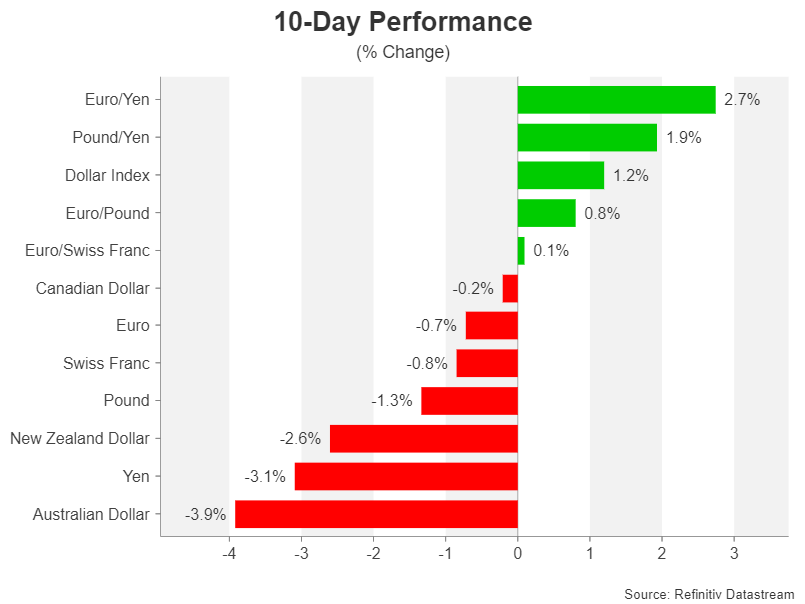

For the US dollar, which has retraced more than half of its June losses, it will be difficult to extend its recovery unless the data can boost the probability for additional rate hikes in 2023 more than Powell already has.

RBA might pause again

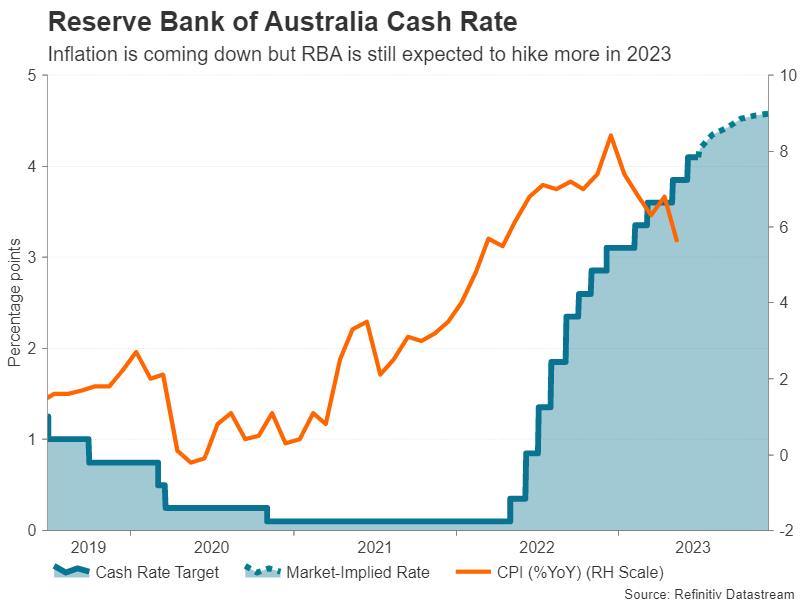

The Reserve Bank of Australia meets on Tuesday for its July policy decision and following the drop in the monthly consumer price index, there is less urgency for policymakers to increase borrowing costs for a third straight meeting. The RBA skipped a hike in April but resumed in May and June. The fall in the 12-month CPI rate to 5.6% in June, combined with soft PMI figures for the same month and ongoing doubts about the Chinese economy, suggests it’s time to pause this month.

However, a third consecutive hike cannot be completely ruled out as the labour market continues to tighten. Employment rose by an impressive 76k in May. Even if the RBA skips a move in July, it will likely maintain a hawkish stance, keeping the door open to further tightening in the future.

The net effect of the meeting outcome might therefore be neutral for the Australian dollar in the most dovish scenario and broader market risk sentiment will probably be a bigger driver for the currency.

Canadian jobs last big clue before next BoC decision

Another central bank that will be pondering whether its next move should be a pause or hike is the Bank of Canada. Next week’s employment report could be crucial in helping policymakers make up their minds before the July 12 decision. Employment in Canada unexpectedly fell in May so another weak report in June could almost certainly keep the BoC on hold in July, especially as there was a downside surprise in inflation too.

This would put the Canadian dollar at significant risk of paring back its month-long gains versus the US dollar.

German data may put euro bulls to the test

In the euro area, it will be a relatively quiet week, with May producer prices (Wednesday) and retail sales (Thursday) on the agenda. However, investors will also be keeping an eye on potential revisions to the June PMIs when the final prints are released on Monday and Wednesday. The flash PMIs were not very encouraging, raising question marks about how much longer the Eurozone economy can remain resilient in the face of rising interest rates and sluggish export markets such as China.

Moreover, key indicators out of Germany will likely attract some attention for traders as Europe’s largest economy is already in a recession and the outlook is not very bright either amid a European Central Bank determined to squash inflation with more rate increases. German trade figures are out on Tuesday, to be followed by industrial orders on Thursday and industrial production on Friday, all for May.

The euro, which has been more successful at fending off the dollar’s latest advances than other majors, could come under pressure if the incoming data keeps surprising to the downside.

Is there any hope for the battered yen?

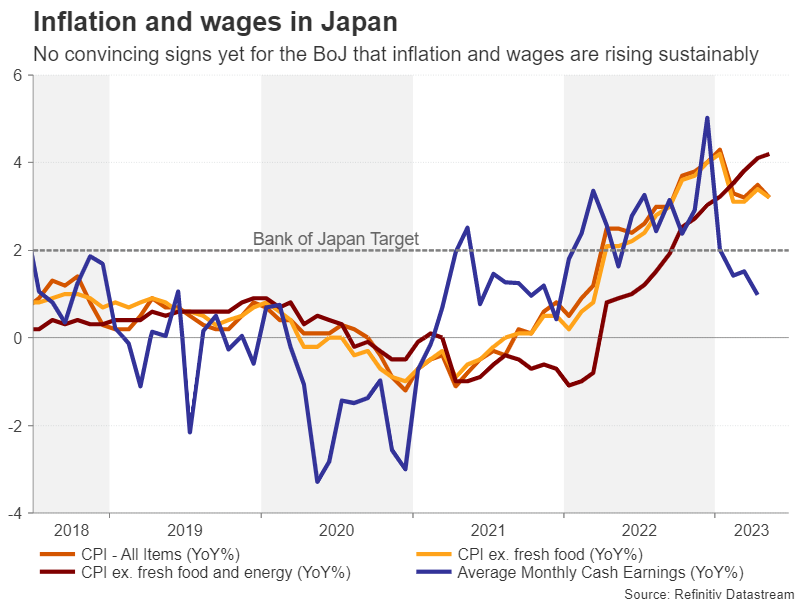

The Japanese yen on the other hand has been badly beaten by the dollar’s resurgence, slumping to more than seven-month lows. The Bank of Japan is refusing to alter its policy course despite an improving economic backdrop and a pickup in underlying inflation. Whilst there have been some subtle shifts in the undertones, the BoJ has mostly maintained its ultra-dovish language and investors are betting that the status quo won’t change anytime soon, pushing the yen to multi-year lows against its main peers.

Next week’s data are not expected to turn the tide for the yen, although a broadly upbeat set of numbers might provide some support for the safe-haven currency.

The Bank of Japan’s quarterly Tankan business survey will start the week on Monday. Forecasts point to growing optimism among businesses for the current and next quarters, as well as plans to increase capital expenditure. Household spending stats will be watched on Friday, along with average cash earnings for May.

Sustainably higher wage growth is a key criterion for the BoJ to begin unwinding its stimulus policies. However, despite reports of bumper pay deals in this year’s Spring wage negotiations, wage growth stood at just 0.8% year-on-year in April. An acceleration in May could increase speculation about a policy change by the Bank of Japan at its July policy meeting, potentially lifting the yen.

{kind=link}