Canada’s June CPI release will come on the heels of a downside surprise in the U.S. inflation data that lowered the odds of additional Federal Reserve interest rate hikes beyond a widely expected July increase. Year-over-year growth in Canadian CPI also looks set to decelerate substantially – we expect to see a 2.9% rate in June, down from 3.4% in May and just below the top end of the Bank of Canada’s 1% to 3% target. That marks a dramatic slowdown from a peak rate of 8% a year ago. Much of that slowing has come from lower energy prices. Gasoline prices were running 20% below year ago levels in June after surging last year on higher oil prices. Mortgage interest costs have continued to surge (a record +30% year-over-year as of May.) Food prices will not outright decline but the rate of growth in grocery prices has been decelerating in recent months.

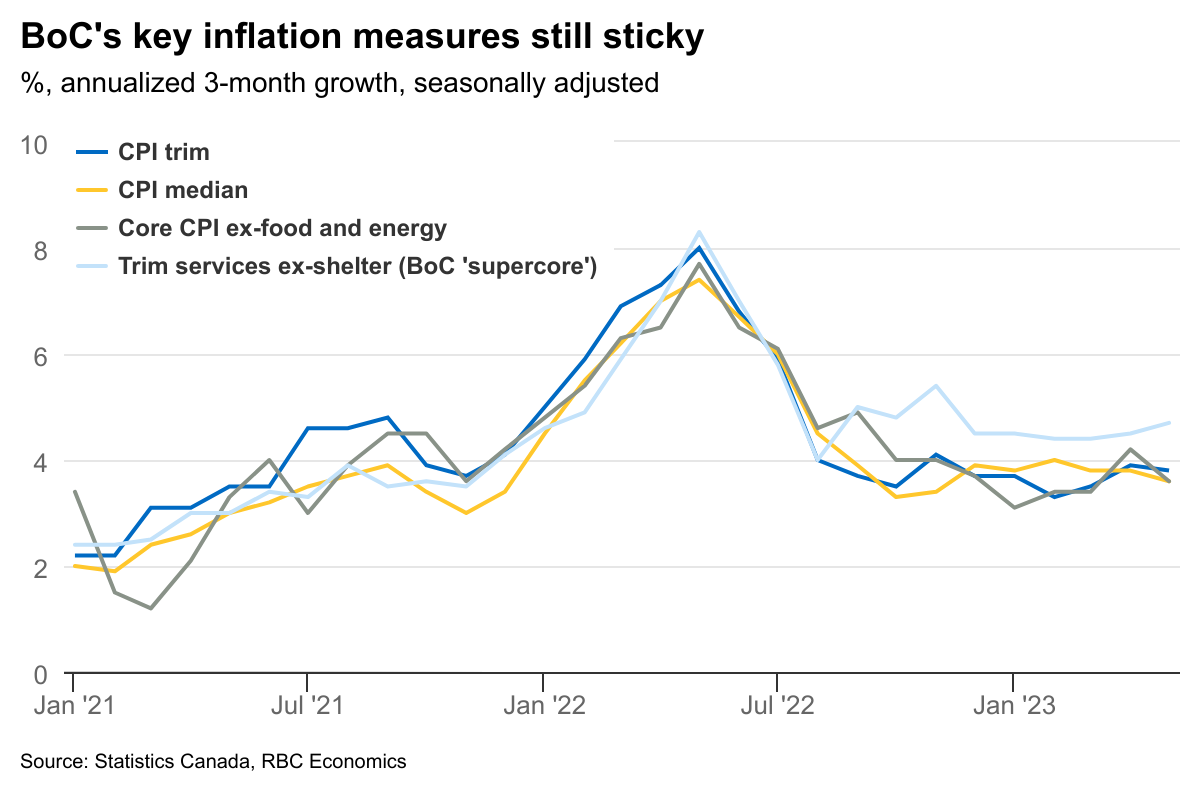

But the BoC will be focused on more recent month-over-month growth in the range of ‘core’ measures designed to provide a better gauge of underlying broader inflation pressures. And growth in those has been stickier at rates still above the BoC target. The BoC’s preferred median and trim CPI measures have been tracking in the range of 3 ½% to 4% at an annual rate and core services excluding shelter (BoC ‘super-core’) has been running closer to 5%.

Consumer demand is still firm – particularly for discretionary services heading into the busy summer travel season. And home resale markets are once again adding to price growth as existing home prices start to edge higher after declining last year. The BoC won’t hesitate to hike interest rates again if that momentum in spending persists. However, interest rate headwinds continue to build. The household debt service ratio very likely hit a new record high in Q2, leaving households vulnerable to any deterioration in labour markets. And the unemployment rate edged higher in May and June. We continue to expect broader inflation pressures will slow enough to prevent additional interest rate hikes from the central bank.

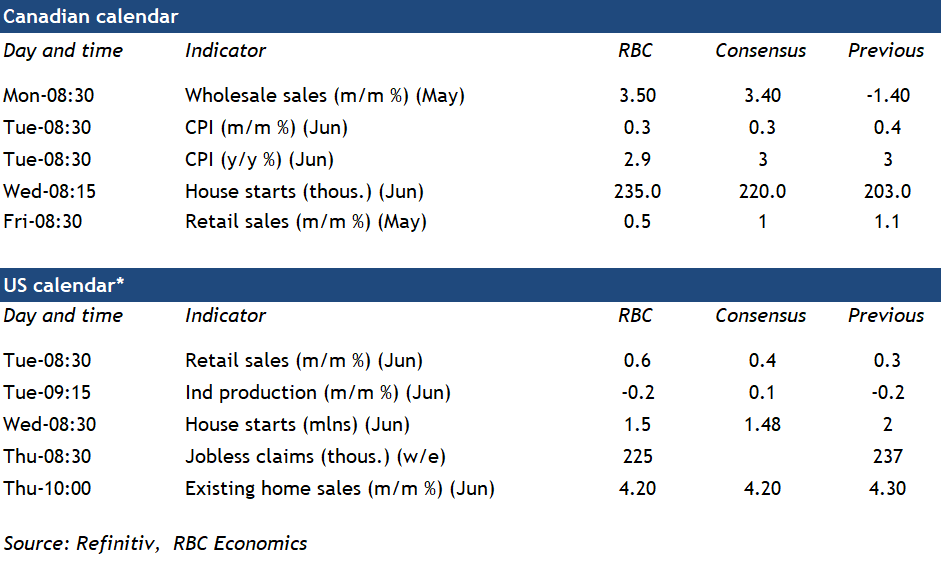

Week ahead data watch

StatCan’s early indicator showed the “core” wholesale sales (excluding petroleum products) increased by 3.5%, sales in the miscellaneous sector added to most of the growth in May, offsetting the decrease in farm product sales.

Canadian housing starts likely bumped up from 203K in May to 235 in June. Permits issuance has been slowing, but the 3-month rolling average of permits issuance was still running at 250k – above the level of May starts and implying more building activity in the pipeline.

U.S. retail sales likely ticked up 0.6% in June, thanks to a boost in auto sales during that month. We expect ex-auto sales were little changed at +0.1% on a month-over-month basis, supported by a price-related increase in gasoline station sales.

We expect a dip (-0.2%) in June’s industrial production in the U.S., due to declines in utility sector output (fewer cooling days than normal).

Food prices will not outright decline but the rate of growth in grocery prices has been decelerating in recent months.){kind=link}