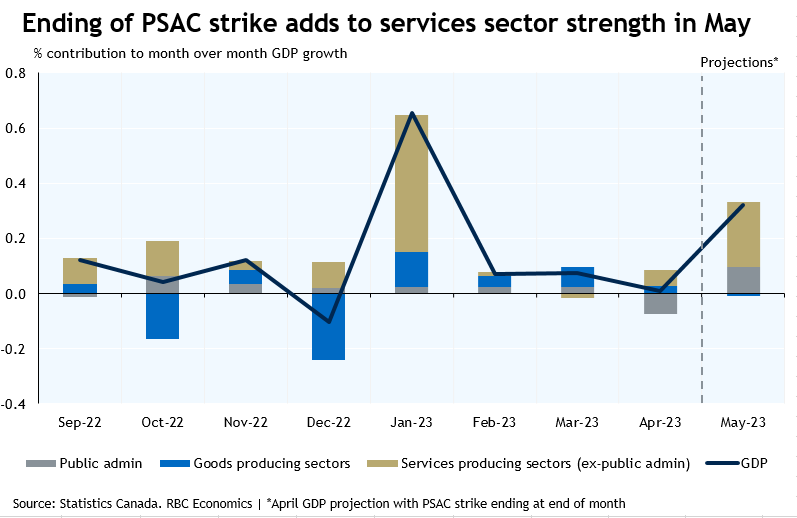

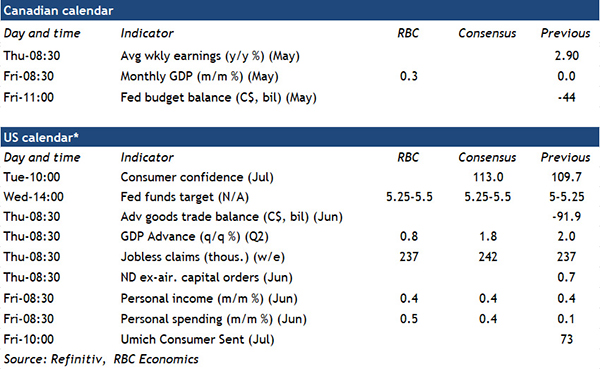

Canadian GDP is likely to have stayed strong May. Statistics Canada’s advance estimate pointed to a 0.4% month over month increase in output—a hair off of our own estimate for a 0.3% increase. With wildfires disrupting production in Alberta, oil and gas extraction was very likely a weak spot. But stronger manufacturing production suggests output from goods producing sectors likely remained at April’s level. And the end of the federal workers strike—which lowered output in April—will have brought arebound in public administration, boosting services output. We expect that factor alone to account for about a third of expected GDP growth in the month. Wholesale and retail sales also both posted sizable gains—rising 3.3% and 0.1%, in real terms respectively in May. Real estate and rental activities improved too on stronger home resales. Hours worked were little changed in June, suggesting a softer print for GDP in that month. But that still leaves GDP growth tracking up one per cent at an annualized basis (slightly above our own 0.5% forecast, but close to the BoC’s current 1.5% forecast.)

With growth also resilient south of the border, the U.S. Federal Reserve is grappling with how much more to tap the brakes. In line with markets, we think the Fed will raise the fed funds range by 25 basis points, to 5.25% – 5.50% next week. That’s after skipping a hike at its last meeting on June 14th. U.S. Inflation data for June surprised to the downside, with the Fed’s ‘super core’ (core services CPI ex-shelter) measure dropping to 1.4% on a three-month annualized basis. For context, the pre-pandemic trend rate of increase for that measure was around 2.5%.

But policymakers will be concerned that the economic backdrop and consumer spending remain too firm for lower inflation pressures to last. Labour market conditions are still tight and wage growth is stuck at elevated levels above what would be consistent with a long-run 2% inflation objective. Beyond the widely expected hike in rates next week however, the path for interest rates is uncertain. Similar to prior statements, the Fed is likely to keep its options open. Our view remains that more weaknesses to domestic demand will emerge over the second half of 2023 as households are strained by elevated borrowing costs and slowing labour markets. That should in turn keep inflation low—and the Fed on the sidelines for the remainder of this year.

Next week’s job vacancy data from the May SEPH release will be closely watched. According to the latest Business Outlook Survey, labour shortages are already easing due as immigration add to labour supply. Job vacancies have been falling on a seasonally adjusted basis in recent months, and we expect that trend to continue.

Our call is for the U.S. GDP to have risen by an annualized 0.8% in Q2 of 2023, down from 2% in the prior quarter. Stronger consumer fundamentals continue to support personal consumption expenditure in Q2. Alongside that there will be a series of data releases for June, including personal income, personal spending, and the advance trade report, all for the U.S.

){kind=link}