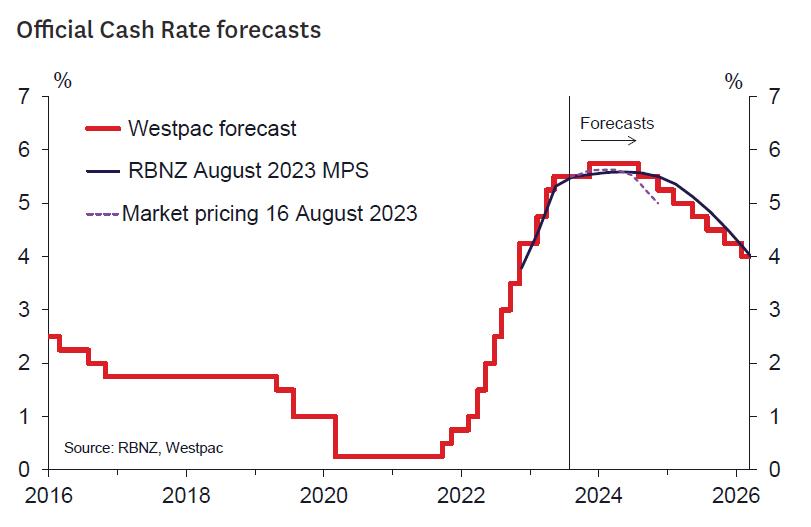

- OCR remained at 5.5% as Westpac and the market had expected.

- The RBNZ’s forecasts for near term growth have been revised up, and its OCR profile revised higher to 5.6% between December 2023 and June 2024, implying around a 40% chance of a further rate hike to 5.75%.

- The RBNZ has revised up its assumption for the neutral OCR by 25bps to 2.25%, lifting the OCR profile.

- The RBNZ’s medium term CPI profile remained unchanged although with higher interest rates. CPI inflation still gets back inside the range September 2024, with risks seen as ‘balanced’.

- Westpac retains its call for a 25bps increase in the OCR in November.

What happened?

The RBNZ left the OCR at 5.5% as widely expected. The overall tone of the Statement is a touch more hawkish than in the May Statement. In many respects the RBNZ’s view on the balance of risks for inflation and interest rates is converging towards our own. That said, during the press conference, Governor Orr indicated that he remained “very comfortable” with the current OCR setting, suggesting that the MPC still has some ground to travel before they decide to implement the 25-basis point hike in the OCR that we continue to expect in November.

The OCR profile has been revised upwards. To some extent this has been driven by changes in technical assumptions around the longer-run “neutral OCR” which has been revised up by 25bps to 2.25%. This essentially means the RBNZ now sees the currently 5.5% level of the OCR as being slightly less restrictive than it previously thought. As a result, a higher forecast OCR track is now needed to keep forecast inflation heading back to target expeditiously.

Recent developments have also pushed the forecast for the OCR higher in the near term. The RBNZ now recognizes that house prices have bottomed out earlier than expected and that they will rise from here (the RBNZ retains a more conservative view on house prices than Westpac – they see price growth of 3% over 2024 versus our view of an almost 8% increase). The higher June quarter out-turn for non-tradables inflation also played a role, as has an upward revision in near term growth and labour market forecasts. All of this was foreshadowed in recent weeks by our MPS preview and Economic Overview.

The factors pushing up inflation pressures have been balanced by the weaker external outlook. Commodity prices have fallen significantly recently which is weighing on incomes and growth over the forecast horizon.

The risks.

The RBNZ importantly has emphasized there are risks in both directions for the economy, inflation, and the OCR. The RBNZ has now moved to a more data-dependent approach – once again as we foreshadowed in our MPS preview. This is sensible and appropriate given the uncertainties out there. The Bank sees upside risks to growth and inflation in the near-term, with the unemployment rate now forecast to rise more slowly than in May. Looking towards the medium-term, the Bank emphasises downside risks to the growth and inflation outlook from the weaker external outlook, especially as regards China. This is unsurprisingly given recent negative trends in dairy prices. Indeed, following last night’s auction, current dairy prices appear about 10% weaker than the Bank’s assumed cycle low point. Overall, the RBNZ assessed that “the risks around the inflation projection remain balanced”.

The bottom line – higher for longer.

The core message remains the same though. The RBNZ still sees an OCR of around the current level of 5.5% as sufficiently restrictive to bring inflation down over time. The OCR will need to remain at around these levels for longer than previously thought as the first easing comes either at the end of 2024 or early 2025 (compared to the September quarter 2024 in the May Statement).

Our view.

We continue to see a hike in the OCR to 5.75% in the November 2023 Monetary Policy Statement. Key indicators to watch, in order of importance, include:

- the September quarter CPI (where the RBNZ will be hoping to see tangible signs of core inflation measures decelerating – especially in non-tradables inflation),

- the September quarter labour market report (where the RBNZ will be watching the unemployment rate, employment growth, and wages indicators closely)

- business and consumer confidence indicators (to assess the extent that weaker commodity prices and farm incomes will flow through to broader economic growth)

- monthly housing market indicators (to check on the extent to which population growth pressures are leading to increased pricing pressures).

The RBNZ’s economic projections.

Turning to the economic projections, following a weaker than expected March quarter, the RBNZ now estimates GDP growth of 0.5% in the June quarter – a sharp upgrade from the 0.2% contraction forecast in the May Statement. From that higher base, the RBNZ forecasts a slightly greater rate of contraction in the economy over the second half of this year. However, following the strong lift in employment reported in the June quarter, the RBNZ expects the unemployment rate to rise more slowly than in the May Statement, posing the risk that wage inflation may slow less quickly than projected previously. Specifically, the RBNZ now forecasts the unemployment rate to rise to 3.8% in the September quarter (previously 4.1%) and 4.4% in the December quarter (previously 4.6%). These revised forecasts address Westpac’s previous concern that the RBNZ was overestimating the likely near-term loosening of the labour market.

Beyond this year, the RBNZ’s projections point to a gradual pick-up in quarterly GDP growth but to rates that remain below the economy’s ‘potential’ until the first half of 2025. In the detail, starting from a firmer base, the RBNZ has become more pessimistic about the outlook for growth in exports. However, this is balanced by a slightly more upbeat outlook for private consumption and a downward revision to forecast growth in imports. Cumulative GDP growth over 2024 and 2025 is slightly higher than in the May Statement, while projected growth in potential GDP has also been raised slightly. The bottom line is that, on average, activity is expected to track 1.7% below the economy’s sustainable capacity, thus applying downward pressure on inflation. This is very similar (just 0.1% less) to what was projected in the May Statement. The unemployment rate is expected to reach a cyclical peak of 5.3% at the end of next year – 0.1% lower than forecast in May.

The RBNZ revised up its inflation forecasts – partly due to higher international oil prices although of more importance was the updated profile for non-tradables inflation. Nontradables inflation has been running hotter than the RBNZ had expected. In addition, measures of core inflation (which track the underlying trends in prices) indicate that price pressures have been easing only gradually two years after the OCR began rising. Consistent with those lingering domestic price pressures, the RBNZ has revised up its near-term forecast for non-tradables inflation.

The RBNZ has analysed the inflationary impact of migration and tentatively concluded that the inflationary impacts will be positive but lower than seen historically. More research is underway.

Looking at inflation two to three years ahead, which is the key focus for the RBNZ when setting monetary policy, the central bank’s forecasts for inflation are largely unchanged. However, that’s because the RBNZ has revised up its longer-term forecast for the OCR. In other words, the RBNZ now thinks that domestic inflation pressures are stronger than it previously assessed, and accordingly that higher interest rates are needed to get inflation back to target.

At those longer horizons, the RBNZ has also revised up its forecast for the long-run neutral OCR by 25bps. However, the longer term forecast for the actual OCR has been revised up by more than the neutral OCR has been (an additional 10 to 15bps). While that’s not a big change, it helps to highlight the RBNZ thinks the risks for inflation have tilted upwards in recent months. Inflation still returns to the 1-3% target range in September 2024.

Reinforcing the stronger outlook for inflation pressures, the RBNZ has revised up its forecast for house prices. While the RBNZ had previously expected house prices to continue falling through the back part of the year, prices have instead flattened off in recent months. The RBNZ now forecasts house prices to rise by around 3% next year, and that will help to support household spending.

{kind=link}