The European Central Bank is headed for a crunch rate decision next week amid rising recession risks and the job on inflation not yet done. It’s going to be a big week for the US dollar as well, as the CPI and retail sales reports are due before the Fed’s September meeting. There’s a barrage of UK data that will keep the pound on its toes before the next Bank of England decision, while the market mood will also be swayed by some key economic indicators out of China, as fears about the health of the world’s second largest economy persist.

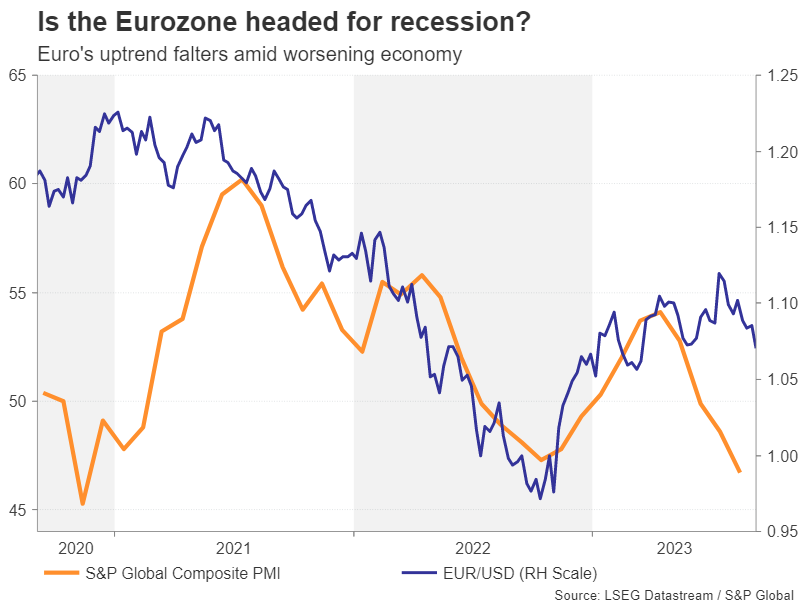

Recession fears come back to haunt the euro

After an impressive uptrend that stretched almost 10 months, the euro’s fortunes took a turn for the worst this summer. A massive rebound in the US dollar has been one of the thorns on the euro’s side. Another is the deteriorating outlook for the Eurozone economy. Following an aggressive tightening campaign that has taken everyone by surprise, borrowing costs in the euro area now stand at their highest since the single currency’s inception. Add to that the weakening demand in Europe’s key export markets, it’s no wonder that growth is faltering. Germany in particular has been hit hard by the sharp slowdown in China and the ZEW economic sentiment index out on Tuesday could underscore all the gloom.

Moreover, the bad news keeps getting worse. Second quarter GDP growth just got revised down to 0.1% from 0.3% q/q, reviving recession angst, while the latest PMI readings show the downturn deepened in August. There could be more negative news from July industrial production figures due on Wednesday.

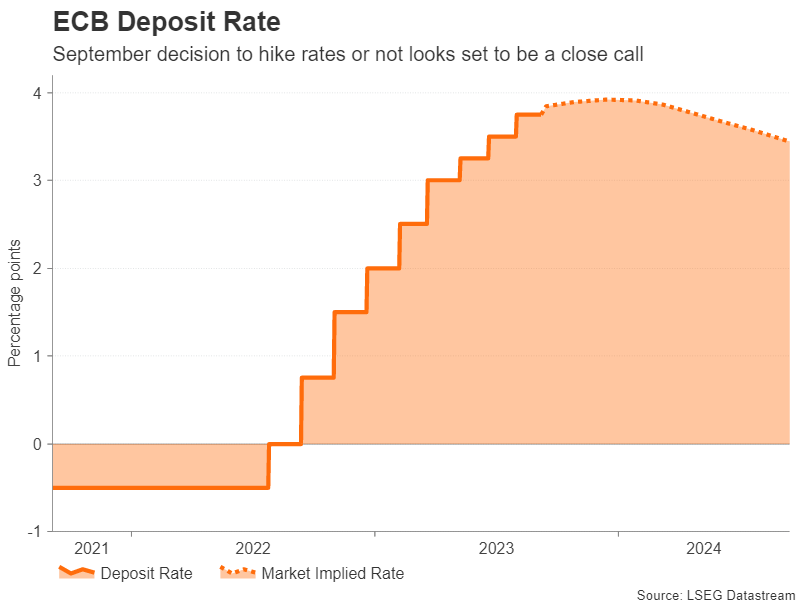

Will the ECB surprise with a 25-bps hike?

All this could give ECB policymakers enough cause for concern to pause interest rates for the first time since June 2022 when they meet on Thursday. The consensus among economists and in money markets is for the ECB to keep its deposit rate unchanged at 3.75%.

However, investors still see a sizeable probability of about 35% that the ECB will hike by 25 basis points in September. After all, core inflation that strips out food, energy, alcohol and tobacco has barely fallen this year, while CPI that excludes only food and energy remains fairly elevated at 6.2% y/y. Whilst there is very good reason to believe that inflation will moderate further over the coming months, the hawks among the Governing Council may push for one further hike for reassurance before agreeing to a pause.

If the ECB decides not to raise rates, a hawkish hold seems almost certain. Hence, there is scope for some limited upside correction in euro/dollar. However, no amount of hawkish rhetoric or even a positive spin on the economy by President Lagarde will be able to save the euro when there are stagflation clouds hanging over it.

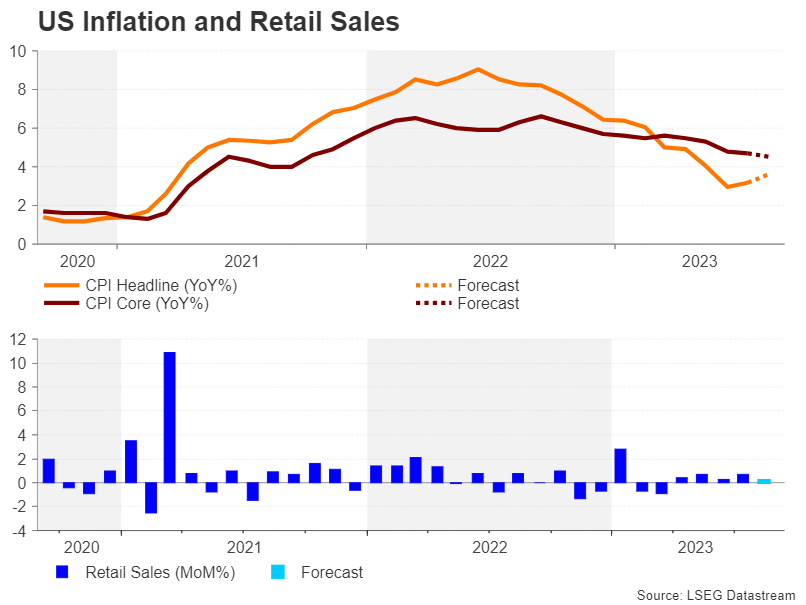

US CPI & retail sales could reinforce higher for longer bets

The Fed doesn’t meet until September 19-20 – that’s almost two months since the July FOMC – and after an uneventful Jackson Hole, markets are badly in need for some fresh policy guidance. Before then however, investors will be treated to the August CPI and retail sales prints.

First up is CPI inflation on Wednesday. The consumer price index inched up in July for the first time in more than a year, rising by 3.2% year-on-year. Expectations are for a further uptick in August to 3.6%. Core CPI on the other hand could edge slightly lower from 4.7%. So unless there’s a beat in both of those figures or a shock large miss, the reaction in the bond and equity markets might be muted.

If the CPI report turns out broadly neutral, attention will swiftly turn to Thursday’s producer price index and retail sales numbers. The unexpectedly strong consumer spending in the third quarter is possibly the single biggest factor that could prompt the Fed to press the hike button in September or November. The retail sales readings will therefore be watched carefully.

Following a 0.7% m/m rise in July, retail sales are forecast to have grown at a more moderate pace of 0.2% in August.

Other releases will include the Empire State manufacturing index, industrial output and the University of Michigan’s preliminary consumer sentiment survey, all on Friday.

The odds for a 25-bps rate increase by November were boosted after the upbeat ISM services PMI and they could firm further if the upcoming week’s data is overall solid. The dollar is already trading at six-month highs so if the US economy continues to shine the brightest among its peers, there could be more gains in store.

Will UK jobs and GDP data come to the pound’s aid?

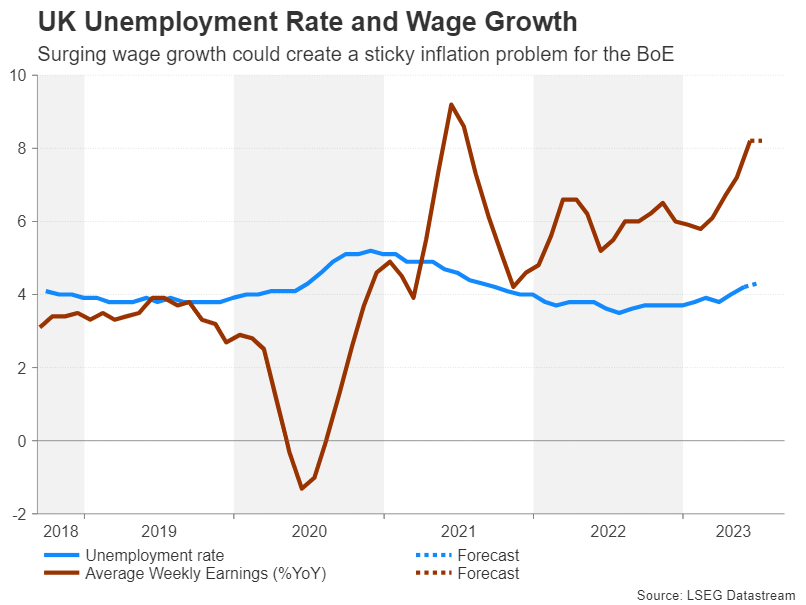

Out of all the major central banks, the Bank of England is widely seen as having the furthest to go in interest rate hikes. That’s been the key driver for sterling this year when, until recently, it topped the FX league for best performers before being toppled by the Swiss franc. The reason why the pound lost its crown is because the ‘further to go’ distance has suddenly shrunk and the BoE may only raise rates a couple more times.

This repricing quickened after Governor Andrew Bailey hinted that policymakers are “much nearer” the end of the tightening cycles. A deepening slump in the UK housing market might explain why Bailey is becoming more jittery about overtightening.

Nevertheless, the British economy has proven to be somewhat more resilient than the Eurozone’s and next week’s data could further support this view. Employment numbers for July are due on Tuesday, which will include a vital update on wage growth. UK pay growth accelerated to an astoundingly high 8.2% y/y in the three months to June. At the very least, high wage growth looks set to prevent the Bank from cutting rates anytime soon even if it decides to go on pause early.

On Wednesday, the focus will be on the July GDP estimate, with industrial production and trade figures also on cue.

Sterling could recoup some of its recent losses should the incoming data ease concerns about stagflation or a recession.

Aussie weighed by Chinese and domestic woes

Down under, another battered currency will be looking for a data boost. The Australian dollar has had a rough ride lately amid a stalling economic recovery in China and the Reserve Bank of Australia not committing to any further rate hikes.

Domestic employment numbers will be important for the aussie on Tuesday after stronger-than-expected GDP growth in the second quarter cast doubt on the RBA’s overcaution on the economy. Any rebound in jobs growth in August could thus provide the aussie a bit of a lift.

However, traders might pay more attention to China’s monthly releases on industrial output, retail sales and investment due on Friday. Although growth momentum is expected to have remained sluggish in August by China’s standards, the forecasts point to some improvement. Should that turn out to be the case, risk sentiment is likely to be buoyed, helping the aussie to bounce back from 10-month lows.

{kind=link}