- The BoE today decided to keep the policy rate unchanged at 5.25% with forward guidance remaining broadly unchanged.

- We think that this marks the peak in the Bank Rate of 5.25%, although wage growth and service inflation remain a joker.

- We stay negative on GBP and continue to see relative rates as a moderate positive for EUR/GBP from here.

The Bank of England (BoE) decided to keep the the Bank Rate (key policy rate) unchanged at 5.25%. Five members voted for an unchanged decision while four members voted for an increase of 25bp. On gilt stock reduction, the BoE set a target of a reduction of GBP 100bn for the next 12 months (up from 80bn the past 12 months).

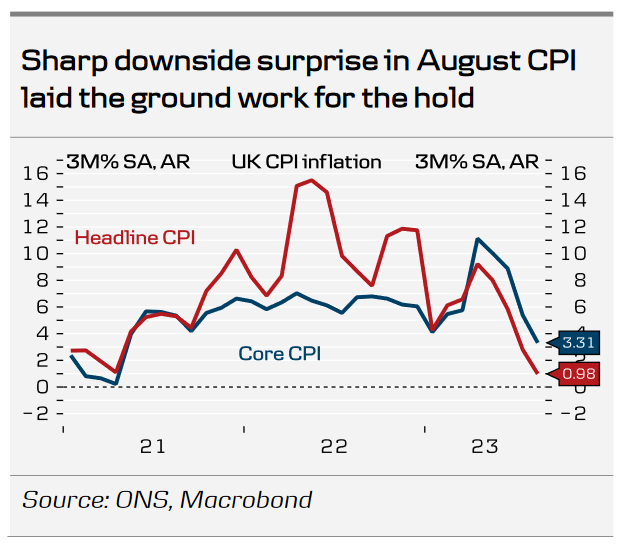

The majority of the Monetary Policy Committee (MPC) voted to keep the Bank Rate unchanged, citing the recent downside surprise to august inflation and further signs that the labour market was loosening. The BoE now expects GDP to rise only slightly in 2023 Q3 and underlying growth in the second half of 2023 also likely to be weaker than expected. Likewise, the BoE expects CPI inflation to “fall significantly further” while noting that service inflation is projected to remain elevated in the near-term. The BoE reiterated that “the current monetary policy stance is restrictive” and that “Monetary policy will need to be sufficiently restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term, in line with its remit“. The BoE retained its forward guidance repeating that “further tightening in monetary policy would be required if there were evidence of more persistent inflationary pressures“. While there is potential for a hike further out, only further amplified by the tight vote split, we do not believe that data will prove sufficiently strong for this to be the case. We expect the UK economy to show further signs of weakness, inflation to level off and a peak in private sector wage growth. Likewise, data releases are rather limited before the next meeting on 2 November, where we only get one job market report and inflation data for September.

Rates. Overall, the reaction in rates markets was relatively muted. Initially, rates markets rallied on the decision and statement and sent 2Y Gilt yields lower, but largely retraced the move during the afternoon. Markets are pricing in 10bp for the November meeting and a peak in the Bank Rate of 5.45%.

FX. EUR/GBP initially moved higher but partly retraced the move later on. On balance, we continue to see relative rates as a moderate positive for EUR/GBP, although GBP has been largely decoupled from moves in relative rates the past month. We expect the relative performance of the euro area and UK economy to be a driver, targeting a moderate rise in EUR/GBP to 0.88 the next year.

Our call. We expect the peak in the Bank Rate to have been reached. In order for BoE to opt for a 25bp instead of an unchanged decision at the next meeting we believe that we would have to see data releases, most notably wage growth and core inflation, prove considerably better than what we currently pencil in. Our call is less than current market pricing (20bp until March 2024). We still believe that the first rate cuts will not be delivered before Q2 2024.

decided to keep the the Bank Rate (key policy rate) unchanged at 5.25%. Five members voted for an unchanged decision while four members voted for an increase of 25bp. On gilt stock reduction, the BoE set a target of a reduction of GBP 100bn for the next 12 months (up from 80bn the past 12 months).){kind=link}