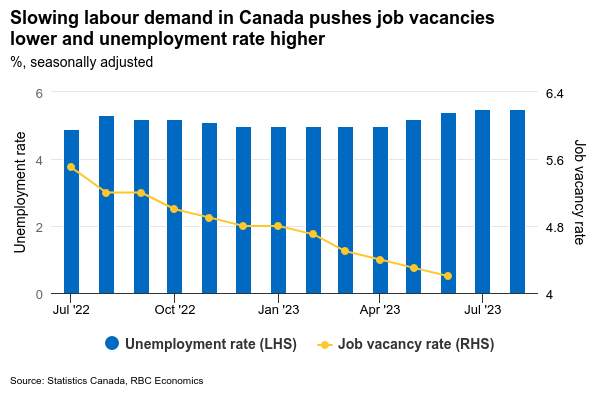

There was a surprise contraction in Canada’s economy in Q2. Despite estimates for a 1% increase, GDP fell by 0.2% (at an annualized rate) and with most of the decline coming from a 0.2% drop in June. And an early estimate for July suggests GDP was ‘essentially unchanged’ from the month before. Data releases have been broadly consistent with that estimate. Employment edged lower in July (down 6,000 positions) and the unemployment rate ticked higher amid a broader pullback in labour demand. Next week’s Survey of Employment, Payrolls and Hours should continue to show a slowdown in the number of job vacancies in July. Manufacturing sales rose 0.9% (excluding price impacts) in July, but that increase was drawn from existing inventories rather than new production. Wholesale sales volumes were little changed (+0.2%) outside of a surge in the large (and volatile) petroleum component. And retail sales continued to soften, with volumes declining by 0.2% after posting an already-large 3.3% annualized drop in Q2.

Part of the weakness in Q2 output can be attributed to ‘transitory’ factors, including the federal government workers’ strike in April and wildfire-related disruptions to mining sector output. But the softening momentum looks to have been extended into Q3, where a flat reading in July GDP would leave output running at roughly 0.4% (annualized) below the Q2 average. That’s broadly in line with our forecast for output to decline by 0.5% in Q3. Notably, the unemployment rate (which is much less affected by those transitory disruptions) has increased by half a percentage point over the last four months. To be sure, the preliminary estimate for August output (also to be released next week) could read better—given both employment and hours worked bounced back in that month. But housing markets also cooled further as resales declined outright for a second consecutive month in August. And spending on discretionary items also continued to flag, with motor vehicle sales continuing on its downward trend in August.

Meantime, our own tracking of RBC debit and credit spending data flagged less spending on hotels and restaurants, as the busy summer travel season comes to an end. Overall, we believe elevated interest rates are putting a tighter squeeze on households’ buying power. That will drive inflation pressures lower still, despite the upside surprise in August.

Week ahead data watch

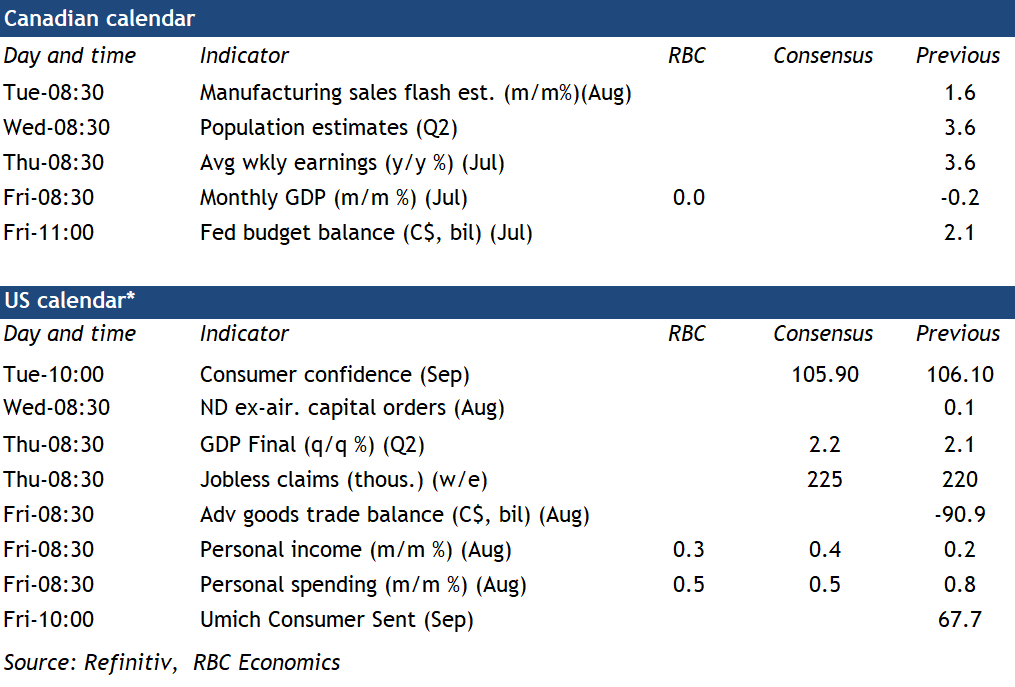

U.S. personal consumption expenditure is likely to edge up 0.5% in August, supported by strong retail sales data (+0.6%). Personal income is likely to rise by 0.3%, supported by slower but still elevated wage gain in the same month (+0.2%).

The July job vacancy and employment growth numbers (from SEPH) are out next week. The former will likely confirm a further slowdown in labour demand. The latter will be watched for any divergence in employment accounts from the earlier-reported 6,000 position drop in July in the more timely Labour Force Survey.

Q2 Canadian population estimates will be watched closely after Q1 saw the strongest year-over-year increase since the 1950s. The release could, reportedly, include new details on the composition of non-permanent resident arrivals, that have driven much of the upward surprise in population growth in recent quarters, and potentially also revisions to prior total population counts.

Canadian auto producers may have avoided a strike. But U.S. strikes (currently targeting a small number of motor vehicle production facilities) will still impact Canadian motor vehicle production—particularly if those disruptions escalate. Auto trade is exceptionally integrated across the border. Auto production and retail combined to account for 1.5% of Canadian GDP in 2022.

and with most of the decline coming from a 0.2% drop in June. And an early estimate for July suggests GDP was ‘essentially unchanged’ from the month before. Data releases have been broadly consistent with that estimate. Employment edged lower in July (down 6,000 positions) and the unemployment rate ticked higher amid a broader pullback in labour demand. Next week’s Survey of Employment, Payrolls and Hours should continue to show a slowdown in the number of job vacancies in July. Manufacturing sales rose 0.9% (excluding price impacts) in July, but that increase was drawn from existing inventories rather than new production. Wholesale sales volumes were little changed (+0.2%) outside of a surge in the large (and volatile) petroleum component. And retail sales continued to soften, with volumes declining by 0.2% after posting an already-large 3.3% annualized drop in Q2.){kind=link}