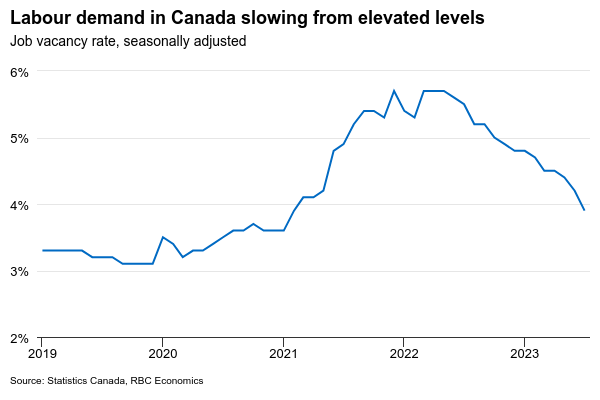

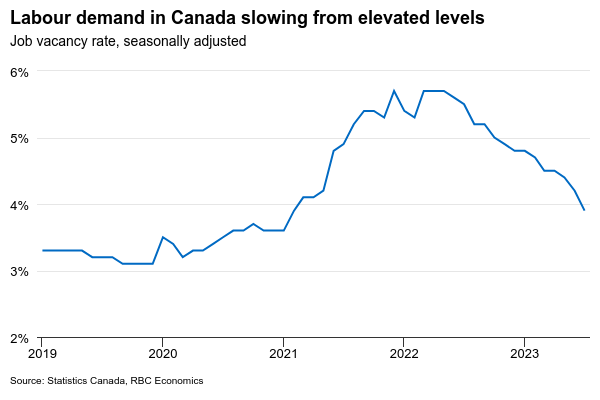

Surging Canadian population growth is helping to fill open positions, and will continue to boost the count of employed workers – we look for a 25k increase in employment in September to be reported next week. But the broader macroeconomic backdrop is continuing to soften. Controlling for population growth, GDP has contracted for four straight quarters on a per-person basis – including a 3.5% (annualized) per-capita decline in Q2. And labour markets have been absorbing new worker supply at a slower pace as demand slows. The number of job vacancies in Canada is still above pre-pandemic levels but has been declining for more than a year after peaking in May 2022. The unemployment rate has begun to rise, climbing to 5.5% over July and August from 5.0% in the spring. We look for another tick up to 5.6% in September with growth in the labour force growth again outpacing that of employment.

Evidence is building that earlier rapid and aggressive interest rate hikes from the Bank of Canada are finally having their intended impact on the broader economy, with consumers pulling back on spending while labour demand softens. The last Canadian inflation print showed some concerning reacceleration in broader measures of price growth – a concerning trend for the Bank of Canada as their only mandate is to get inflation back to a 2% rate. But inflation lags the economic cycle, and softening in labour markets should reassure the central bank that further easing in price pressures will follow. Wage growth has remained surprisingly firm – and will continue to see increases for unionized employees in particular, as contracts that were agreed to before the spike in prices are renegotiated. But we expect broader wage pressures will slow as the unemployment rate edges higher.

Week ahead data watch

The next round of U.S. payroll employment data will likely show the unemployment rate holding steady at 3.8%, and employment up by 177K, slightly below the 187K add in August. Labour market conditions remain tight with initial jobless claims trending at low levels. But signs of slowing demand including falling job openings mean we can continue to expect conditions to slow.

A U.S. government shutdown is widely expected to start this weekend but is expected to have a limited broader impact on the economy. Shutdowns can impact economic data temporarily, but only a portion (a large chunk of U.S. federal government spending is from mandatory spending programs, like social security, and it is just discretionary spending subject to annual spending approvals that is impacted). A relevant point of comparison is the 2019 shutdown, which lasted for 34 days, and resulted in only a 0.02% reduction in GDP according to the CBO.

We expect the Canadian trade deficit to narrow in August, oil prices increased by 7% during that month, contributing to most of the export growth.

The U.S. Advance economic indicators report showed that the goods deficit shrunk by $6.6B in August, with exports increasing by 2.2%, and imports declining by 1.2%. Looking at category details, auto exports were down 8.1% from the prior month, and industrial supplies exports went up by 4.9% in August.

per-capita decline in Q2. And labour markets have been absorbing new worker supply at a slower pace as demand slows. The number of job vacancies in Canada is still above pre-pandemic levels but has been declining for more than a year after peaking in May 2022. The unemployment rate has begun to rise, climbing to 5.5% over July and August from 5.0% in the spring. We look for another tick up to 5.6% in September with growth in the labour force growth again outpacing that of employment.){kind=link}