- Latest Chinese data offer signs of stabilization

- Inflation and trade numbers may corroborate that view

- But the slump in property market continues to cast a shadow

- The releases are scheduled for Friday, during Asian trading

Is the Chinese economy bottoming out?

Following a temporary boost just after the removal of COVID-related ultra-restrictive policies, the Chinese economy faced a steep economic slowdown, with the property sector being the biggest drag as major developers are struggling with mountains of debt and missing payments to lenders, which brought an end to a long-running building boom that propelled China’s growth.

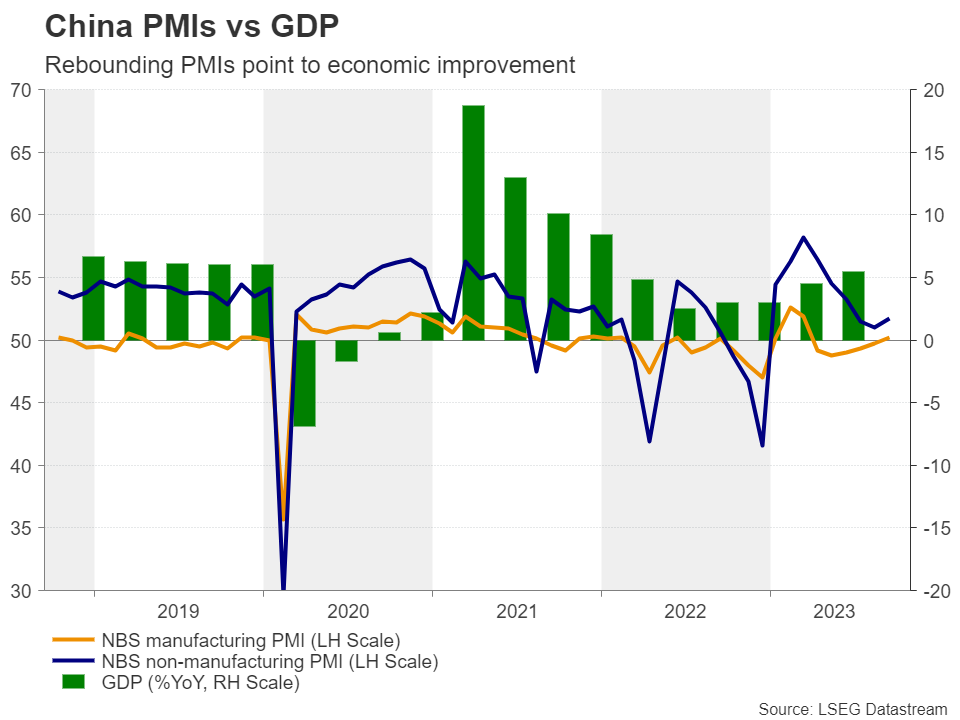

However, a streak of recent economic indicators is suggesting that the world’s second-largest economy may have begun bottoming out, with the manufacturing PMI pointing to expanding activity in September for the first time in six months, and the composite index rising to 52.0 from 51.3. Earlier signs of improvement had emerged in August, with factory output and retail sales accelerating, imports and exports falling at a slower pace than in July and deflationary pressures easing. On top of that, industrial profits unexpectedly surged 17.2%, more than reversing July’s 6.7% slump.

Spotlight turns to inflation and trade numbers

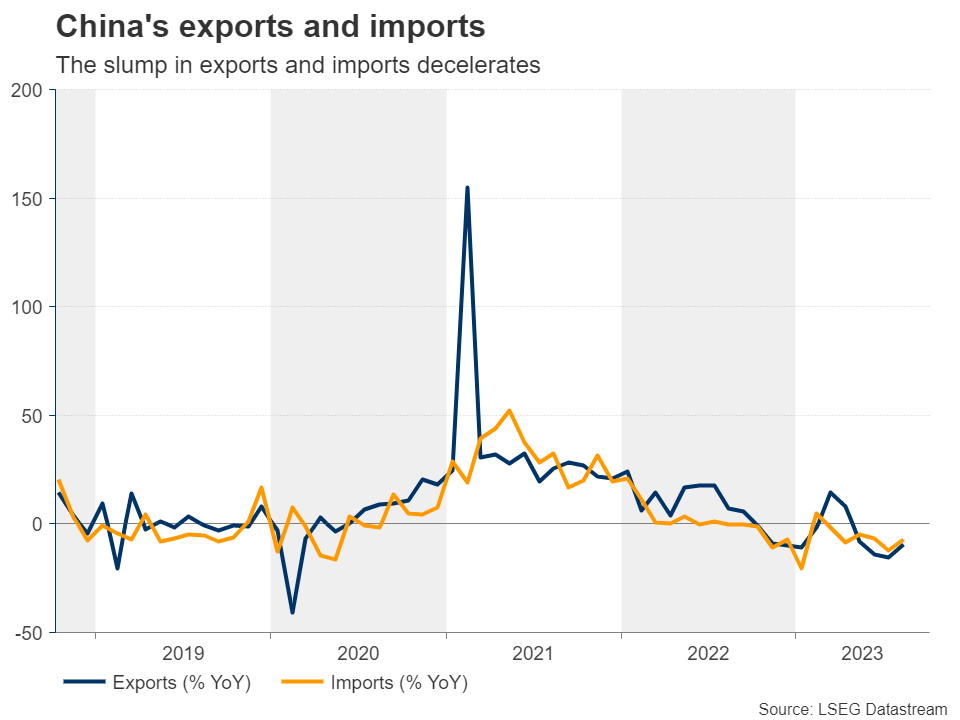

On Friday, the agenda includes the CPI and PPI numbers, as well as trade data for the month of September, with expectations confirming the stabilization narrative. The CPI is expected to have ticked up to 0.2% y/y from 0.1%, while the PPI rate is forecast to have risen to -2.4% from -3.0%. Both imports and exports are expected to have continued falling, but at an even slower pace than in August, resulting in a 2.4% increase in the nation’s trade surplus.

This, combined with a record number of Chinese choosing to travel home last week for the Golden Week holiday and thereby boosting domestic consumption, could further add to the case of a steadying Chinese economy. Ergo, given the close trading ties Australia and New Zealand have with China, the aussie and the kiwi may extend their latest recoveries.

The property sector continues to suffer

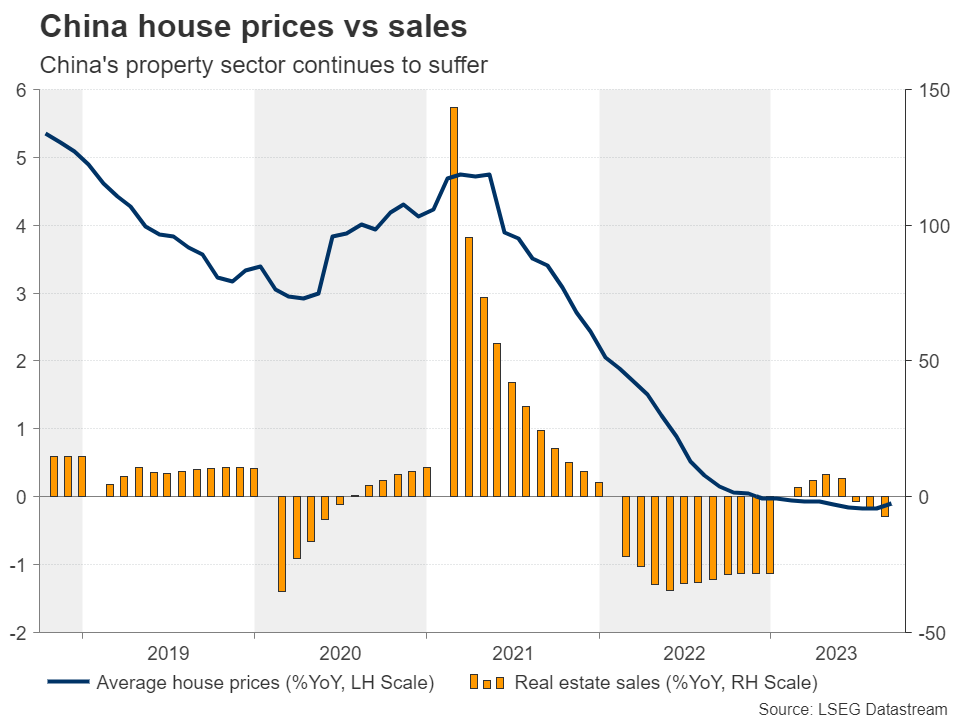

Nonetheless, assuming that the worst is over and that Chinese authorities can claim victory after announcing a series of measures to shore up activity may be unwise. The slump in the property sector worsened in August, with home prices, property investments and sales falling at steeper rates than in July. Home prices dipped at the fastest monthly pace in 10 months, while property investment and sales slumped for the 18th and 26th consecutive month respectively. In yearly terms, house prices were down 0.1%, the same rate as in July.

And as if the data is not enough, China’s Evergrande, the world’s most indebted developer said a couple of weeks ago that its founder was being investigated over “illegal crimes”, while just today, the nation’s largest private property developer Country Garden Holdings warned that it might not be able to meet all its offshore payment obligations within the relevant grace periods.

The trade tensions between the West and China, ranging from tit-for-tat trade tariffs to tech rivalry and spying allegations, are not helping either.

Recovery in aussie and kiwi may be limited

Therefore, even if the aussie and kiwi extend their gains for a while longer, a long-lasting uptrend is unlikely. Equity markets are also likely to continue feeling the heat of China’s slowdown, on top of any additional pressure due to speculation of ‘higher for longer’ interest rates in the US.

Ausse/dollar has been trading in a recovery mode since October 4, when it hit support at the 0.6280 zone. However, the pair is still trading below the key resistance barrier of 0.6490 and well below the lower bound of the sideways range that contained most of the price action between February and August. This suggests that the bears could claim control again soon and perhaps push for another test at around 0.6280. A break lower would confirm a lower low and may see scope for extensions towards the low of October 2022, at around 0.6170.

For the bearish outlook to be dismissed, aussie/dollar may need to climb all the way above the 0.6570 zone, a jump that would signal its return within the aforementioned sideways range.

{kind=link}