U.S. Highlights

- The risk of a government shutdown has returned as Congress has one week left before the continuing resolution passed on September 30th expires.

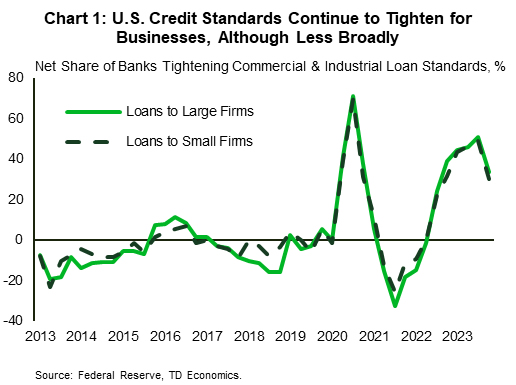

- The Federal Reserve’s Senior Loan Officer Opinion Survey showed that banks continued to tighten credit standards in the third quarter, as credit demand weakened further.

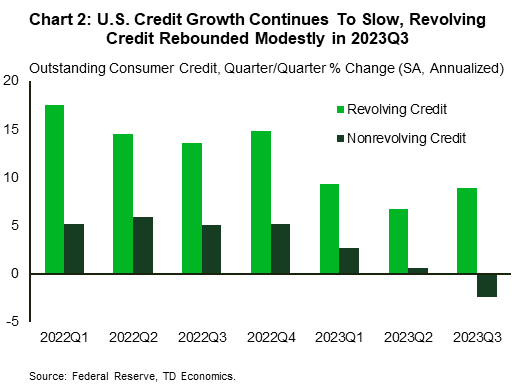

- Consumer credit growth eased in the third quarter as an acceleration in revolving credit growth (i.e. credit cards) was offset by a contraction in nonrevolving credit (i.e. student loans).

Canadian Highlights

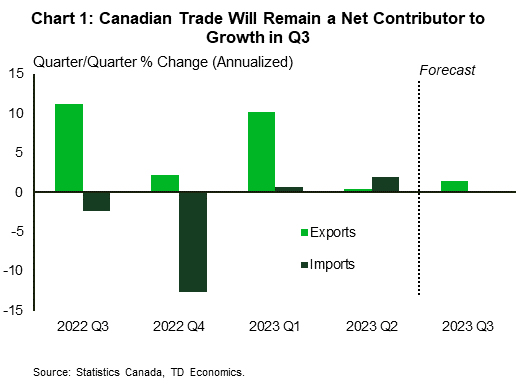

- Merchandise trade data out this week showed a further widening in Canada’s trade surplus in September, suggesting net trade will make a positive contribution to Q3 growth.

- The minutes from the Bank of Canada’s policy discussions showed that “lack of downward momentum” on the inflation front remained the top concern for policymakers and was behind the difference in opinion on whether more hikes are needed.

- The Senior Deputy Governor Carolyn Rogers delivered an update on the Financial Systems Review where she warned households and businesses to prepare for a “new normal”, where the cost of borrowing is likely to remain elevated over the medium-term.

U.S. – Government Shutdown Risk Redux

After last week’s busy slate markets took a breather to digest last week’s Federal Reserve policy decision and prepare for the risk of another potential government shutdown next Friday. On the data front, the Federal Reserve Senior Loan Officer Opinion Survey (SLOOS) and consumer credit report both showed credit conditions remained tight and demand continues to wane.

Monday’s release of the SLOOS showed that banks continued to tighten credit standards across loan categories in the third quarter and report weaker business and consumer demand for loans (see here). Although this came as little surprise considering Treasury yields rose by roughly 100 basis-points in Q3, the share of banks reporting tighter standards for commercial and industrial loans actually declined relative to the second quarter (Chart 1). This also held true for consumer credit cards and auto loans, although personal and mortgage loans each saw broader tightening relative to the second quarter. Despite the modest narrowing of credit tightening in the third quarter, the Federal Reserve’s continued signaling of rates staying higher for longer means a material loosening of credit standards likely remains a way off.

Easing consumer demand for loans was also evident in the Federal Reserve’s consumer credit data release on Tuesday which showed outstanding credit growth slowed notably relative to the second quarter. Outstanding revolving credit loans, which includes credit cards, saw accelerating growth in the third quarter of 8.6% while non-revolving credit growth, which includes student loans, declined by 2.4% (Chart 2). Under the weight of higher prices many consumers are increasingly relying on revolving credit to support spending, particularly as the moratorium on student loan repayment ends. Next week’s retail sales data will show whether the past six months of real sales growth, aided by consumer credit, continued into October despite the growing headwinds facing consumers.

In addition, updated CPI data out next week is expected to show continued easing in aggregate price pressures, supported by cooling energy prices. While this would undoubtedly be positive news, core inflation, which excludes food and energy prices, is expected to persist well above the Federal Reserve’s 2% target. A majority of FOMC members have noted that their current pause is conditional on sustained disinflation progress, with Chair Powell stating on Thursday that “if it becomes appropriate to tighten policy further, we will not hesitate to do so”.

Rounding out the coming week is the return of the risk of a potential government shutdown (see here) as the continuing resolution passed on September 30th expires on Friday, November 17th. Of the twelve appropriation bills that need to be passed to fund the federal government, the House has passed seven and the Senate has passed three with no consolidated bill managing to pass both chambers of Congress. This means that another continuing resolution may be used as a stopgap once again, but markets are likely to become increasingly apprehensive as Friday’s deadline approaches.

Canada – ‘Higher for Longer’ is the BoC’s Winning Strategy

This week was sparse on economic data but rich on remarks from the Central Bank. Neither had a significant impact on the markets, with the TSX largely building on the dynamics across global equity markets, and finishing the week slightly lower. Volatility in the bond market returned by Thursday, reflecting the anxiety south of the border where weak demand in the 30-year auction helped to push the term premium higher. The only sigh of relief came from oil prices, although the decline in crude was driven largely by expectations for slowing global demand rather than peace in the Middle East.

On the macro front, Statistics Canada reported September’s data on merchandise trade, which recorded a second consecutive month of trade surplus, with exports gaining slightly more than imports. This offset the negative impact from the B.C. port strike and Nova Scotia floods, observed earlier in the quarter. Exports also outperformed imports in volume terms, which means trade will be a net contributor to Q3 growth.

Looking ahead, the minutes from the Bank of Canada’s policy discussions indicated an anticipated slowdown in exports, attributed to a decrease in global demand. But it was concerns of the disinflationary process stalling that remained the top concern for the Governing Council. Higher global oil prices, rising cost of rent and other housing-related costs, driven by demand-supply imbalances, have been the primary factors leading to the recent stalling in disinflationary dynamics. Moreover, despite the ongoing easing in the labour market, wage growth remains in a range that’s higher than is needed to help push inflation down towards the BoC’s target. This ‘lack of downward momentum’ was behind the difference in opinion on whether more hikes are needed.

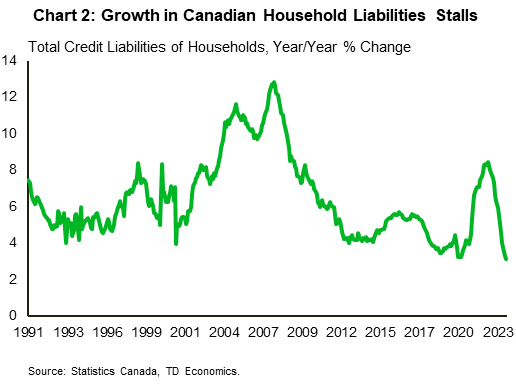

Despite these concerns, members observed that the 475 basis points in rate hikes have helped to rebalance the economy. Consumer spending and household credit growth are both showing signs of slowing, as households continue to adjust to higher borrowing costs (Chart 2). This message was echoed by the Senior Deputy Governor Carolyn Rogers who delivered an update on the Financial Systems Review. She reiterated that servicing debt is getting harder for some households, which can be observed through higher consumer delinquency rates and a rising share of accounts with utilization rates above 90%.

Rogers also pushed back on the expectations for lower rates and advised households and businesses to prepare for a ‘new normal’, where the cost of borrowing is likely to remain elevated. ‘Higher for longer’ rhetoric remains the winning strategy for the Bank as it keeps financial conditions tight without adjusting the policy rate. With little hard data to mull over, markets are likely to remain in ‘wait and see’ mode until the CPI report on November 21st. Next week, we’ll get the most recent reading on existing home sales, which will provide an update on whether recent weakness gained more traction in October alongside the sharp uptick in yields. Stay tuned!

{kind=link}