- China’s credit impulse has remained on a slow upward trajectory since July 2023.

- Key China’s central bank (PBoC) official has signalled a further accommodating monetary policy in 2024.

- Growth in China’s services activities expanded in December 2023.

- Watch the 16,100 key long-term secular support on the Hang Seng Index.

China and Hong Kong stock markets have been in the doldrums for the past four years since the pandemic crisis added by a heightened deflationary risk inflicted on China’s economy due to persistent weakness in the property market in the past two years.

Both have started the new year on a weak footing with China’s CSI 300 benchmark stock index slipping to a year-to-date loss of -4.2% at this time of the writing and hitting its lowest level since 2018. Similar dismal performances are seen in the Hong Kong stock market; Hang Seng Index (-4.2%), Hang Seng Tech Index (-7.3%), and Hang Seng China Enterprises Index (-4.6%) over a similar period.

Despite the lingering risk of the entrenched deflationary spiral, ongoing corruption, and regulatory clampdowns in China’s private and public sectors that spooked foreign investors, there has been some sign of “economic light shining in the dark tunnel”; the official NBS Non-Manufacturing PMI and Caixin Services PMI for December indicated a slight growth uptick in services activities for December with new orders grew the most in seven months in the report compiled by Caixin.

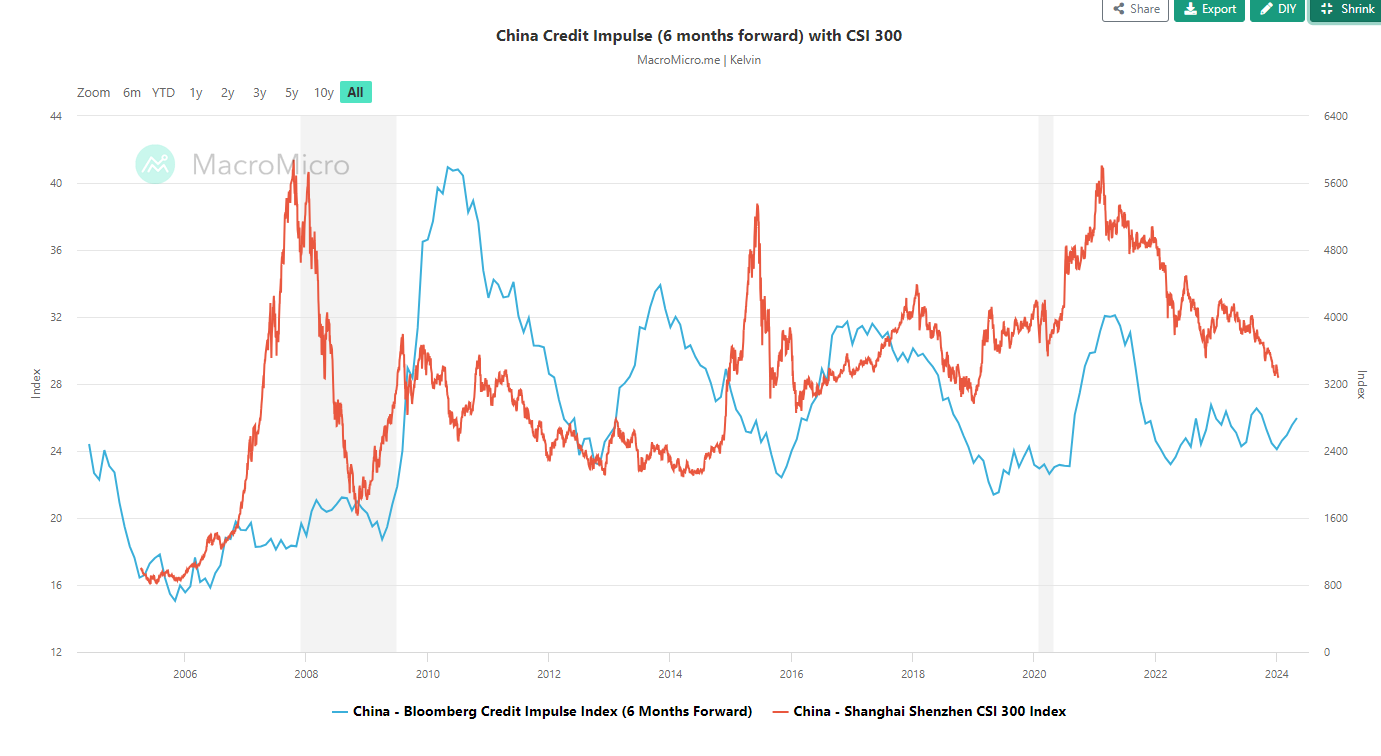

Secondly, the Bloomberg Credit Impulse Index for China, a measurement of credit/liquidity growth has been on a slow upward trajectory since July 2023 (24.10 in July to 25.97 printed on November 2023).

China’s credit impulse is on the rise

Fig 1: Bloomberg China Credit Impulse Index & CSI 300 as of 11 Jan 2024 (Source: Macro Micro, click to enlarge chart)

Interestingly, if we shift the Bloomberg Credit Impulse Index for China six months forward, its movement does exhibit a direct correlation with the CSI 300 Index which implies a continuation uptick in credit impulse may translate to a similar upward directional movement in the CSI 300 going forward (see Fig 1).

In addition, a key China’s central bank (PBoC) official signalled earlier this week that PBoC may lower the reverse ratio requirements for Chinese banks in 2024 which translates to a potential further accommodative monetary policy stance. Also, the downside pressure inflicted on the yuan via an accommodating monetary policy is likely to be reduced in 2024 as the US central bank, the Fed may start to embark on a dovish pivot path for interest rate cuts in the US.

Hence, it may lead to a further rebound in credit impulse which in turn stokes potential bullish short-term animal spirits back into the China and Hong Kong stock markets.

16,100 remains the key long-term secular support on the Hang Seng Index

Fig 2: Hang Seng Index long-term secular trend as of 11 Jan 2024 (Source: TradingView, click to enlarge chart)

The ongoing weakness seen in the Hang Seng Index (HSI) has managed to be contained above the 16,100 key long-term secular pivot support which is defined by its ascending trendline that led to a prior significant recovery after every major bearish correction since August 1998, the onslaught inflicted by the Asian Financial Crisis.

To see a much more potentially heightened bullish animal spirits feedback loop in the Hong Kong stock market, the HSI needs to clear above its major resistance at 18,460 which is the descending trendline in place since the February 2021 major swing high where the two important events took shaped around that period; the strict business practices regulations imposed on China Big Tech firms and a series of Covid related lock-down measures enacted in China.

{kind=link}