U.S. Highlights

- Treasury yields shot higher this week, as expectations for a June rate cut fell.

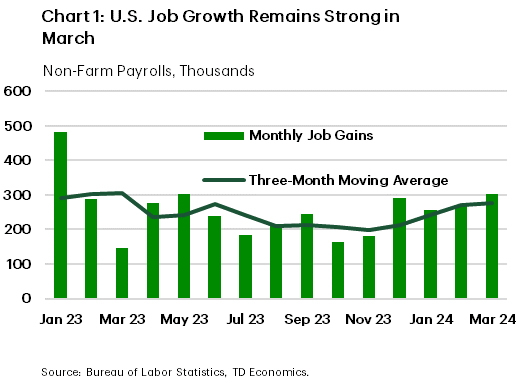

- The U.S. economy had another strong month of hiring in March – adding 303k jobs – while the unemployment rate ticked down to 3.8%.

- Seven voting FOMC members were out speaking this week and the messaging was consistent: policymakers are in no rush to cut rates.

Canadian Highlights

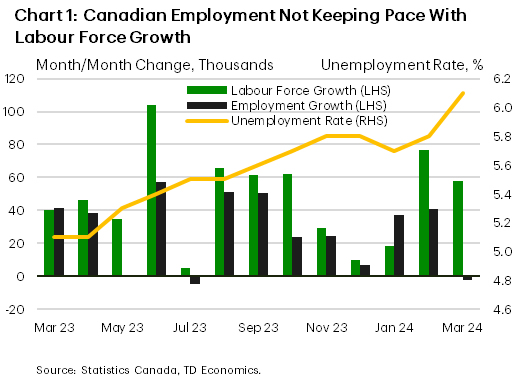

- Canada’s labour market lost some more steam in March, with the unemployment rate on the rise again. However, wages continue to show signs of stickiness.

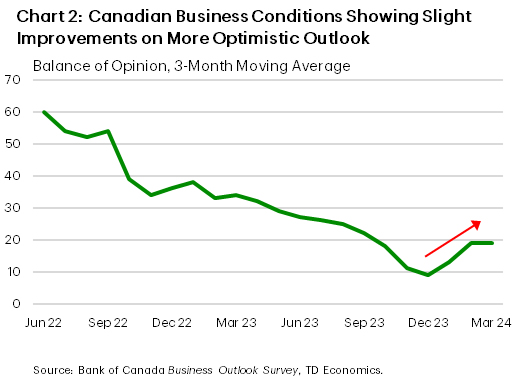

- In contrast, international trade data as well as business and consumer sentiment are pointing to an improved economic backdrop after months of stall-speed growth.

- Interest rate relief is on the horizon, but the Bank of Canada is unlikely to move off its current policy stance at next week’s meeting.

U.S. – Don’t Bet on June

The first trading week of the second quarter saw Treasury yields push higher as market participants continued to dial back expectations on the timing of the first-rate cut. According to CME Fed futures, a June cut is only 53% priced, and expectations are now for a total of 60 basis points (bps) of cuts by year-end – a far cry from the 150-bps priced at the beginning of the year. Higher readings on inflation, a resilient economy, and a cautious FOMC have all been factors reinforcing the recent recalibration of expectations. At the time of writing, the 10-year Treasury yield is up 15 bps for the week (to 4.35%) and has risen nearly 50 bps since the beginning of the year.

It was a very busy week on the economic data calendar, but the headline release was Friday’s employment report. The U.S. economy added 303k jobs in March, well ahead of the consensus forecast. Meanwhile, the household survey showed strong gains in both the labor force and civilian employment, with the net effect being the unemployment rate ticking down to 3.8%.

On aggregate, the labor market remains healthy and has yet to show any meaningful signs of cooling. Over the past three months, job gains have averaged 276k – slightly stronger than the 251k averaged in 2023 (Chart 1). With job openings still elevated, and increased immigration alleviating some of the pressure on labor supply, job growth could conceivably run in the 150k-200k range for the rest of the year. This would go a long way in rebalancing the labor market, without necessitating any meaningful increase in the unemployment rate.

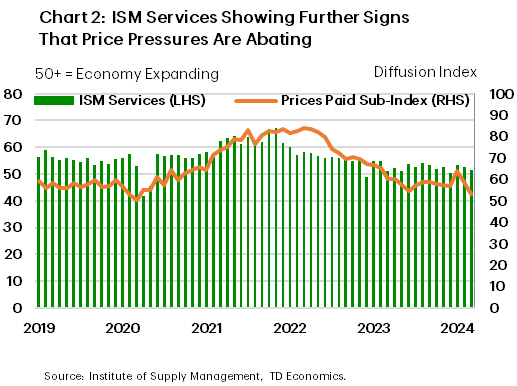

Other economic data out this week also brought encouraging news on the state of the economy. The ISM manufacturing index unexpectedly broke above the 50 mark – the threshold of expansion territory – for the first time in sixteen months. The release showed manufacturing activity is finding a firmer footing alongside an uptick in current production and a rebound in new orders. Meanwhile, the ISM services index slipped to a three-month low. The pullback reflected some softening in new-orders and a sharp decline in the prices paid sub-index, which fell to the lowest level since March 2020 (Chart 2). On the surface, this is an encouraging development for Fed officials who are struggling to rein in still elevated service inflation. However, the fact that 13 industries are still reporting an increase in prices suggests that even with some recent stabilization in the rate of price growth, elevated price pressures remain a concern.

This is why all seven voting FOMC officials out speaking this week maintained a cautious tone on the timing of rate cuts. In a speech delivered on Wednesday, Chair Powell stuck to the script, reiterating that he still believes, ‘rate cuts are likely to be appropriate at some point this year’ though decisions will be made on a ‘meeting by meeting’ basis. With the Fed waiting for further evidence of cooling inflationary pressures, next week’s CPI release will offer further insight on whether the recent uptick in inflation a speed bump, or perhaps something more meaningful.

Canada – Gearing Up For The Bank of Canada Decision

The Bank of Canada (BoC) had no shortage of new developments to digest this week. Labour market updates for the month of March highlighted the string of releases, though a pulse check on business and consumer sentiment as well as international trade data were also on watch. As the dust settles on the week’s data, markets have increased their bets that the BoC will pull the trigger in June. However, we think a July cut is more likely, which will allow the Bank a bit more time to compile evidence that inflation is moving durably back to 2%.

The Canadian economy lost a few jobs in March (-2.2k) against expectations for a trend-like gain. The details of the report were weak and consistent with a continued cooling in the labour market. The unemployment rate moved up sharply to 6.1% as employment struggles to keep pace with population-driven labour force growth (Chart 1). Meanwhile, hours worked fell slightly, suggesting economic activity for March moderated after a hot start to the year. However, wage growth remains a thorn in the BoC’s side, having been stuck above 5% y/y for the past year. More progress on this front is likely desired by the BoC, but there is clear evidence that current policy is doing its part in lowering the temperature on Canada’s job market.

However, on the growth side, February’s international trade data supported an acceleration in economic activity in the first quarter. Export and import volumes both surged after a weak prior month with current tracking suggesting trade will be another tailwind for Q1 growth. We do expect some give back in trade activity in March, especially in imports, as spending patterns weaken over the coming quarters.

Meanwhile, business and consumer sentiment of the economy has improved slightly per the BoC’s Business Outlook Survey (BOS) and the parallel Canadian Survey of Consumer Expectations (CSCE). While demand remains under pressure due to high inflation and interest rates, expectations for lower interest rates provide more confidence about the future economic outlook (Chart 2).

The focus now shifts to the April 10th interest rate announcement where the BoC will release a fresh set of forecasts in their Monetary Policy Report (MPR). These updates may start to lay the foundation for interest rate cuts. Notably, since the last MPR released in January, inflation for Q1-2024 is coming in a touch lower than projected (3.1% vs 3.2% y/y), while growth should see a significant upgrade from the current flat-GDP projection. The BoC has held the policy rate at 5.00% for the last nine months, which has helped inflation on its path back to 2%. Indeed, headline inflation has now been in the high-end of the Bank’s 1–3 percent inflation target range for two consecutive months. However, we expect that the Bank will need to see a few more constructive inflation prints to ensure their mandate is being met.

{kind=link}