Markets

US trading hours were only a little more entertaining than dull European ones yesterday. Minneapolis Fed Kashkari (non-voter this year) gave us some flavor on how a slightly more hawkish shift at last week’s policy meeting could have looked like. His guidance sounded familiar: “the most likely scenario is we sit here for an extended period of time”. In its official statement, the onus remained on a policy rate cut though the bar to implement one was raised given little progress on inflation. We assume FOMC Minutes to highlight a split between two camps. Kashkari said that the bar for raising rates is quite high, but he doesn’t rule it out. He made the case of a higher neutral interest rate especially given persistent housing inflation, questioning how restrictive monetary policy really was/is. It would also help explaining why the labour market has proven resilient and why inflation moved sideways in recent quarters. Kashkari said that he penciled in two rate cuts for this year when Fed officials met in March and that he’ll forecast anywhere from two to zero cuts for 2024 when officials meet next on June 12. The Kashkari comments didn’t bring life into mostly sideways dealings. German Bundesbank Nagel sounded somewhat more hawkish than most of his colleagues by stressing that a range of potential factors could lead to higher inflationary pressure in the future (eg demographic trends pushing up wages). The ECB shouldn’t allow an accommodation to higher levels trigger a de-anchoring of inflation expectations. Longer term, he doesn’t eye a return to the sort of weak inflation rates (and easy monetary policy) we’ve had in the run-up to the pandemic. Apart from these central comments, the US Treasury kicked off its mid-month refinancing operation with a solid $58bn 3-yr Note auction. Tonight’s $42bn 10-yr Note sale and Thursday’s $25bn 30-yr Bond auction will likely prove more tricky.

UK gilts outperformed returning from May Day holiday and in the run-up to tomorrow’s BoE meeting. Risks are asymmetric with markets likely positioned too hawkish. Sterling already feels the pressure with EUR/GBP returning to 0.86. We eye a sustained return higher for the pair.

News & Views

The US Commerce Department has revoked export licenses that allowed major chip companies Intel and Qualcomm to do business with China’s Huawei. The move, confirmed to and reported by the Financial Times, comes amid evidence that China is able to develop advanced chips using US technology despite sweeping export controls that are already in place since 2022. “We continuously assess how our controls can best protect our national security and foreign policy interests”, the agency said. US national security officials note that these cutting edge chips have helped China engage in cyber espionage. Washington has also pushed allies/kings of the semiconductor industry in Europe and Asia, including the Netherlands & South Korea, to implement tough(er) export controls.

The Turkish government has been holding talks recently about easing restrictions on offshore currency swaps, Bloomberg reported citing people familiar with the matter. Any loosening would be gradually and could focus in a first step on longer-maturity contracts but is expected to be welcomed by foreign investors. Local banks are currently limited in the amount of liras they can lend (in the form of FX swaps, options, futures etc.) to counterparties abroad. This, however, makes it difficult for investors to hedge the currency risk they take when investing in lira assets, despite the demand being there. International optimism on Turkey has increased sharply in recent months thanks to more orthodox policies, including in monetary policy. This high demand abroad also caused a widening gap between offshore and onshore rates with the former earlier this month at some point being about half of the domestic ones (26% vs >50%), denting the currency’s carry appeal. The Turkish lira reacted stoic (USD/TRY 32 area) on the news for the time being but other Turkish assets including equities and CDS did rally.

Graphs

GE 10y yield

ECB President Lagarde clearly hinted at a summer (June) rate cut which has broad backing. EMU disinflation continued in April and brought headline CPI closer to the 2% target. Together with weak growth momentum, this gives backing to deliver a first 25 bps rate cut. A more bumpy inflation path in H2 2024 and the Fed’s higher for longer strategy make follow-up moves difficult. Markets have come to terms with that.

US 10y yield

The Fed in May acknowledged the lack of progress towards the 2% inflation objective, but Fed’s Powell left the door open for rate cuts later this year. Soft US ISM’s and weaker than expected payrolls supported markets’ hope on a first cut post summer, triggering a correction off YTD peak levels. Sticky inflation suggests any rate cut will be a tough balancing act. 4.37% (38% retracement Dec/April) already might prove strong support for the US 10-y yield.

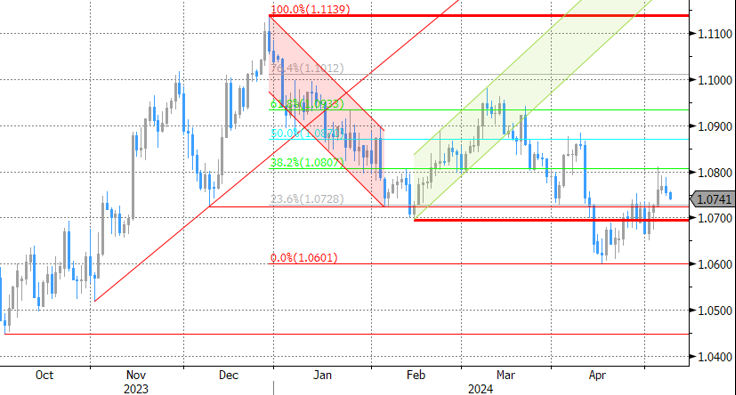

EUR/USD

Economic divergence, a likely desynchronized rate cut cycle with the ECB exceptionally taking the lead and higher than expected US CPI data pushed EUR/USD to the 1.06 area. From there, better EMU data gave the euro some breathing space. The dollar lost further momentum on softer than expected early May US data. Some further consolidation in the 1.07/1.09 are might be on the cards short-term.

EUR/GBP

Debate at the Bank of England is focused at the timing of rate cuts. Most BoE members align with the ECB rather than with Fed view, suggesting that the disinflation process provides a window of opportunity to make policy less restrictive (in the near term). Sterling’s downside turned more vulnerable with the topside of the sideways EUR/GBP 0.8493 – 0.8768 trading range serving as the first real technical reference.

gave us some flavor on how a slightly more hawkish shift at last week’s policy meeting could have looked like. His guidance sounded familiar: “the most likely scenario is we sit here for an extended period of time”. In its official statement, the onus remained on a policy rate cut though the bar to implement one was raised given little progress on inflation.){kind=link}