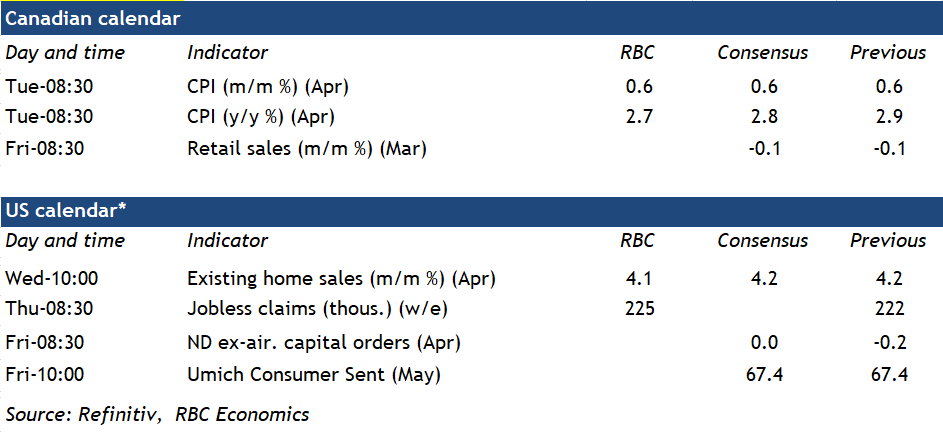

Next week’s Canadian April inflation report will be the last major data release before the Bank of Canada’s next interest rate decision on June 5th. Absent an upside surprise, we think the soft conditions in the economy and labour markets should warrant a 25-bps interest rate cut from the BoC in June.

In April, we expect year-over-year CPI growth will tick down to 2.7%, from 2.9% in March, edging further towards the BoC’s 2% inflation target despite higher energy prices. Gasoline prices were up 7.6% in April from March, and with roughly a third of the increase coming from the annual increase in the federal carbon tax. But food price growth has been slowing and we look for year-over-year price growth for “core” CPI excluding food and energy products to edge down to 2.6% in April from 2.9% in March. Surging mortgage interest costs (+25% year-over-year in March) are a lagged result of earlier interest rate increases and have been accounting for more than a quarter of total price growth, but the pace of increase is gradually slowing.

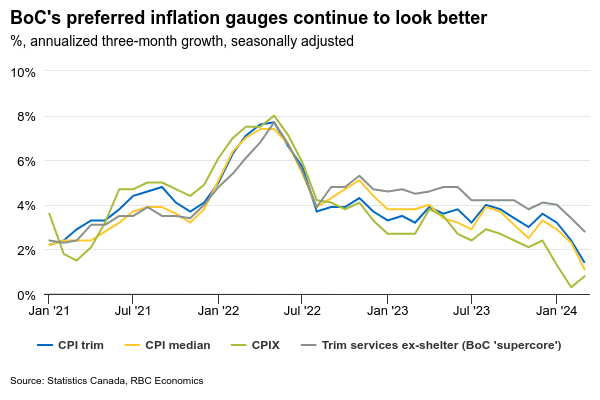

BoC policymakers will be more focused on the central bank’s own preferred core measures of inflation (designed to be a better gauge of broader inflation pressures) for further signs of easing. The CPI ‘median’ and ‘trim’ measures averaged 3.0% on a year-over-year basis in March – dropping back to the top end of the BoC’s 1% to 3% inflation target range for the first time since 2021. Very recent trends have been softer with the closely watched 3-month rolling average of month-over-month increases in those measures below the 2% inflation target rate as of March. This cooling has been broad-based, as more items in the CPI basket are seeing lower inflation this year.

Week ahead data watch

StatCan’s advanced indicator suggests retail sales were flat in March, in-line with our own RBC cardholder tracking . Sales at gas stations likely increased by 1.2% as gas prices were up during the month. But unit auto sales were down 3% on a seasonally adjusted basis. Excluding autos and gas stations, core retail sales should have edged higher, but sales volumes (adjusted for inflation) are expected to be lower in March. Our own RBC Consumer Tracker points to stronger spending on essentials in March and weaker discretionary goods sector spending.

{kind=link}