Markets

Markets took a slow start to the new trading week. An empty eco calendar facilitated the status quo. Cleveland Fed Mester said that inflation risks moved up in Q1 while the economy was a little bit stronger than anticipated. Given that she wasn’t on the median path (3 rate cuts) in March, she might back only one at the June meeting. The relevance is low though given that she’ll retire at the end of June. Core bond yields moved a little further away from last week’s tested support levels, but the move lacked momentum. US Treasuries slightly underperformed German Bunds with daily yield increases varying up to +2.5 bps in the US and +1.5 bps in Europe. Similar story for the dollar which closed marginally stronger at 104.56 (DXY) and 1.0857 (EUR/USD). US stock markets showed a diverging pattern near all-time highs with the Dow Jones correcting 0.5%, S&P 500 unchanged and Nasdaq still gaining 0.65%.

Eco releases remain second tier today, but the number of central bank speakers increases with especially Fed Waller discussing the US economy. Waller was one of the first and most prominent (rumoured candidate as next Fed chair) Fed-members to talk out in favour of keeping rates higher for longer. His February “what’s the rush” and March “there’s still no rush” speeches are testament to his views and together with hotter CPI prints kick-started this year’s Treasury sell-off. His views are a good indication (and potential market mover) on how the dots might shift at the June policy meeting given his standing a “leader” of the large minority camp (9/19) which suggested only a maximum of two policy rate cuts in 2024 at the March meeting. Bank of England Chair Bailey speaks as well which could influence the probability of a first rate cut at the next, June, meeting (currently 50% probability).

The eco calendar heats up later this week with May UK CPI data and FOMC Minutes tomorrow, global PMI surveys (May) and the outcome of Q1 negotiated wage data (EMU) on Thursday and finally UK retail sales (May) and US durable goods orders (April) on Friday.

News & Views

Czech National Bank (CNB) MPC member Tomas Holub indicated that he still considers it too early to already decide whether the pace of CNB rate cuts should be slowed from 50 bps at the previous three meetings to 25 bps at the June meeting. Holub first wants to see the May inflation data that are published before the June 27 meeting. Inflation unexpectedly jumped from 2% to 2.9% in April, but this was mainly due to a rise in volatile food prices. Aside from the development in headline in inflation, Holub also said he keeps a close eye on the development of Czech krone. Regarding domestic developments, he mentions wages as a key variable. Faster than expected wage rises could be an argument to slow the pace of rate cuts. Looking forward, Holub indicated that a Czech policy rate of 4.5% or slightly lower is realistic for end this year (currently 5.25%).

Minutes of the May 6-7 meeting of the Reserve Bank of Australia learnt that the RBA kept its policy rate unchanged at 4.35% as it wanted to avoid excessive fine tuning. The central bank’s economic scenario still sees inflation returning to the 2-3% target by late 2025 as consumption is expected to moderate. Even so, the RBA acknowledged, while still balanced currently, recent information showed that risks around inflation had risen somewhat. In this context, it is difficult for the RBA to either rule in or rule out a future change in the cash target rate. At the same time, the board showed limited tolerance for inflation to return to the 2-3% target later than 2026. If assumptions on the pace of the deceleration in inflation risk to be overly optimistic, a rate hike still can be considered again. Amongst others, a scenario of consumer spending picking up somewhat more rapidly due to strength in the labour market and better growth in public demand and business investment might all cause inflation to return to the target later than currently hoped for. Markets currently only see about a 50% chance of a first inaugural rate cut at the end of this year. AUD/USD eases slightly this morning to 0.666.

Graphs

GE 10y yield

ECB President Lagarde clearly hinted at a summer (June) rate cut which has broad backing. EMU disinflation continued in April and brought headline CPI closer to the 2% target. Together with weak growth momentum, this gives backing to deliver a first 25 bps rate cut. A more bumpy inflation path in H2 2024 and the Fed’s higher for longer strategy make follow-up moves difficult. Markets have come to terms with that.

US 10y yield

The Fed in May acknowledged the lack of progress towards the 2% inflation objective, but Fed’s Powell left the door open for rate cuts later this year. Soft US ISM’s and weaker than expected payrolls supported markets’ hope on a first cut post summer, triggering a correction off YTD peak levels. Sticky inflation suggests any rate cut will be a tough balancing act. 4.37% (38% retracement Dec/April) already might prove strong support for the US 10-y yield.

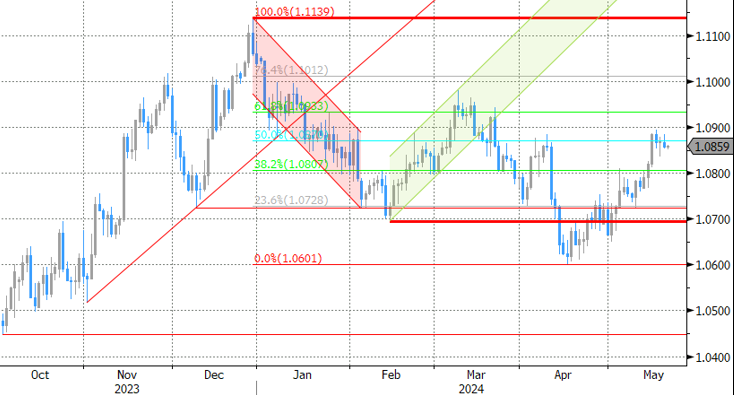

EUR/USD

Economic divergence, a likely desynchronized rate cut cycle with the ECB exceptionally taking the lead and higher than expected US CPI data pushed EUR/USD to the 1.06 area. From there, better EMU data gave the euro some breathing space. The dollar lost further momentum on softer than expected early May US data. Some further consolidation in the 1.07/1.09 are might be on the cards short-term.

EUR/GBP

Debate at the Bank of England is focused at the timing of rate cuts. Most BoE members align with the ECB rather than with Fed view, suggesting that the disinflation process provides a window of opportunity to make policy less restrictive (in the near term). Sterling’s downside turned more vulnerable with the topside of the sideways EUR/GBP 0.8493 – 0.8768 trading range serving as the first real technical reference.

Fed-members to talk out in favour of keeping rates higher for longer.){kind=link}