Markets

Marine Le Pen’s Rassemblement National scored broadly as expected in the first round of French parliamentary elections. They won the ballot with around 33% of the vote, ahead of the left front (28%) and Macron’s alliance (21%). In 485 out of 577 districts, the RN and its allies won outright or made it to next week’s second round. In more than half of the districts, it could be a 3-way race in theory though the likes of PM Attal already called for tactical redraws to keep the far right from power. The deadline for eligible candidates is tomorrow at 6pm after which ballot polls will become more precise. A hung parliament with a large, but no absolute, majority for RN remains the most likely outcome but the power-sharing cohabitation scenario is still at play as well. It explains today’s “muted” relief move. EUR/USD moved up from 1.07 to currently 1.0760. French assets outperform with the 10-yr OAT/swap spread currently trading around 46 bps compared to last week’s high of 50 bps. Ahead of the European elections, this was only 25 bps. European stock markets add 0.75%-1.25% with the French CAC40 rising 1.85%. German Bund yields rise around 8-9 bps across the curve with Bunds underperforming US Treasuries. US yields add 3-4 bps, extending the move that started in the run-up to and after last week’s presidential election debate which triggered a significant change in polling results in favour of former president Trump.

Today’s eco calendar only contained German inflation data. Prices rose by 0.2% on a monthly basis, the same pace as in May and exactly in line with forecasts. The Y/Y-figure slowed as expected from 2.8% to 2.5%. Regional data suggest that the drop was mainly due to a negative contribution from road-fuel prices. Lower price gains for package holidays and miscellaneous goods and services also dragged inflation slightly down. Spanish and French CPI data were last week in line with forecasts as well suggesting that tomorrow’s EMU number could be a non-event. Consensus stands at 0.2% M/M and 2.5% Y/Y (from 2.6%) for headline CPI and 2.8% (from 2.9%) for core CPI. Today’s data had no impact. After European close, attention will turn to ECB Lagarde’s opening speech at the ECB forum on central banking in Sintra. Tomorrow and on Wednesday, an avalanche of central bankers will discuss topics like drivers of equilibrium interest rates, productivity in the short and long run, geopolitical shocks and inflation,…

News & Views

The Polish minister for development and technology Paszyk informed the Polish financial website Money.pl about a plan that would subsidize up to 175000 mortgages over the next five years. The minister said that high loan costs are both hampering Polish home purchases. His interest-trimming proposal marks a sharp U-turn with the Tusk-led coalition government as recently as mid-May. Cautiousness back then ruled, saying that additional mortgage support could overstimulate a housing market that was already benefitting from support under the previous government. Prices as a result rose at the EU’s sharpest pace last year. New mortgages in Poland are the most expensive in the EU, driven in part by a central bank that’s refraining from cutting rates. The National Bank of Poland is meeting this Wednesday and is widely anticipated to keep the policy rate at 5.75% for a ninth time straight. There’s a broad consensus within the MPC not to cut rates before 2025 given high (fiscal) policy uncertainty and its impact on inflation for the second half of this year.

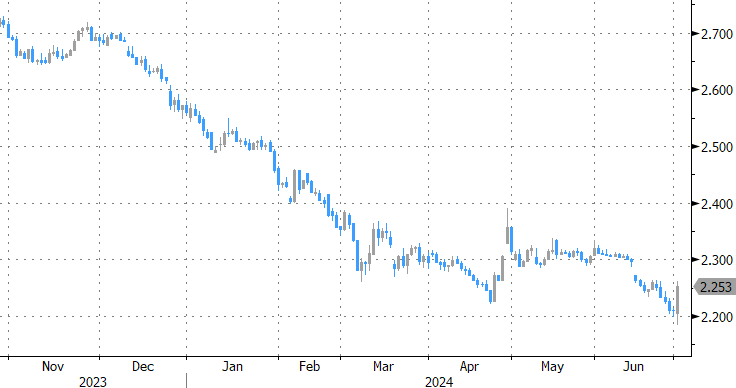

China’s central bank said it will borrow government bonds from primary dealers “in order to maintain the steady operation of the bond market”. The announcement came after China’s 10-yr yield dipped to the lowest level since data collection began in 2002. Chinese authorities have become wary of the bond bull rally, driven by investors looking for safe haven assets against the backdrop of a weak economy and expectations for ongoing (or increasingly) supportive monetary policy. The likes of the PBOC fear for the interest-rate risk implications. A market reversal could saddle up large bondholders (e.g. banks) with significant losses, posing financial stability risks. One of the ways the PBOC could operate is to borrow the bonds and sell them into the market. It is unlikely to significantly and permanently push up government bond yields though it may offer a bottom. China’s 10-yr yield rebounded intraday after the word got out, going from as low as 2.18% to 2.25% in the close.

Graphs

10yr OAT/swap spread: muted relief after first round of French elections

EUR/USD: similar ray of hope

Chinese 10-y bond yield rises from all-time low after PBOC announces programme to borrow bonds from primary dealers

Eurostoxx 50: again more firmly within the sideways trading range of the past months

and Macron’s alliance (21%). In 485 out of 577 districts, the RN and its allies won outright or made it to next week’s second round. In more than half of the districts, it could be a 3-way race in theory though the likes of PM Attal already called for tactical redraws to keep the far right from power.){kind=link}