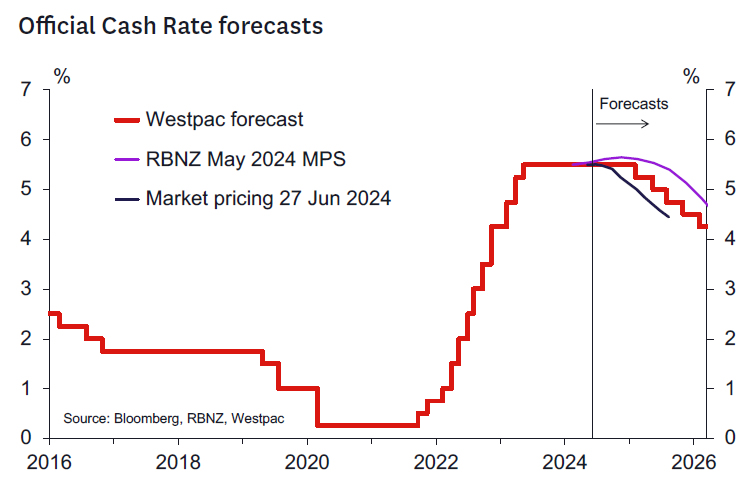

- We expect the RBNZ to leave the OCR at 5.5%.

- We expect a short statement as with the April Review.

- The RBNZ will emphasise the upside risks to consumer spending and inflation emanating from the less contractionary than expected Budget 2024.

- But they will balance this with some dovish messages associated with potential downside risks to growth as the economy continues to stall and the labour market eases.

- We don’t see any net dovish tilt that might bring an easing in 2024 into play – if that’s coming it would be at the August Monetary Policy Statement.

OCR to remain on hold awaiting definite signs of inflation returning sustainably to the target range.

The RBNZ presented an unexpectedly hawkish tone at its May Statement by revising up its forward OCR profile. The new profile indicated both an increased probability of a further increase in the OCR (at the November 2024 Statement) and a delay in the timing of an eventual reduction in the OCR to August 2025. The RBNZ tended to de-emphasise the tightening risk in its post-Statement communications but leaned heavily into the message that the OCR needed to remain at 5.5% for “a sustained period” to ensure annual CPI inflation returns to the 1 to 3% range.

The RBNZ noted that some upside risks potentially could come from the fiscal outlook and noted a full assessment would need to await the release of Budget 2024. This Review is the RBNZ’s first opportunity to update its view now the Budget is public. We anticipate the RBNZ will continue to retain a hawkish perspective with respect to fiscal risks as Budget 2024 ended up being less contractionary than the HYEFU projections the RBNZ’s forecasts were based on. We doubt they will be drawing definitive conclusions as no forecasts will be presented at this Review and it is too early to judge the impact that tax cuts (timed to begin at the end of July) will have on consumer spending and inflation.

Economic activity assessment.

What will be interesting is the RBNZ’s take on the (sparse) data on economic growth that has emerged since the May Statement. High on the RBNZ’s mind was the uncertainty of how the economy would perform during the year ahead now that we are in the period where monetary policy is at “peak transmission” from the interest rate rises that finished in May 2023. The RBNZ also raised the possibility that labour “hoarding” which had prevented firms from adjusting to tighter monetary conditions might suddenly reverse and cause a more rapid adjustment in the labour market in the period ahead. These concerns, if crystalised, could lead to a faster decline in non-tradables inflation and an earlier return of inflation to the middle of the 1 to 3% target range and an earlier easing profile. In this regard we note that since the May Statement:

- Q1 GDP was in line with the RBNZ’s forecasts and hence won’t lead to much of a starting point difference (although consumption was stronger which might be a hawkish indicator at the margin).

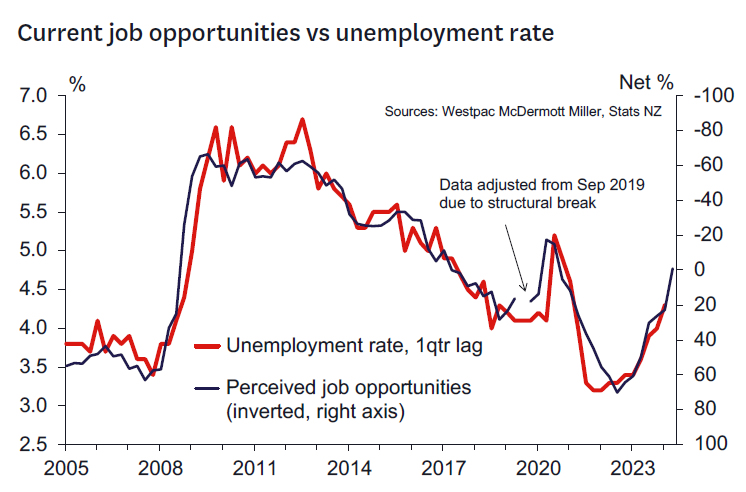

- Labour market indicators have been weak, but not weaker than expected (monthly filled jobs were down 0.1% net in April and May – and may be further revised down – while Westpac’s Employment Confidence survey seems consistent with the 4.6% unemployment rate forecast by the RBNZ for the June quarter).

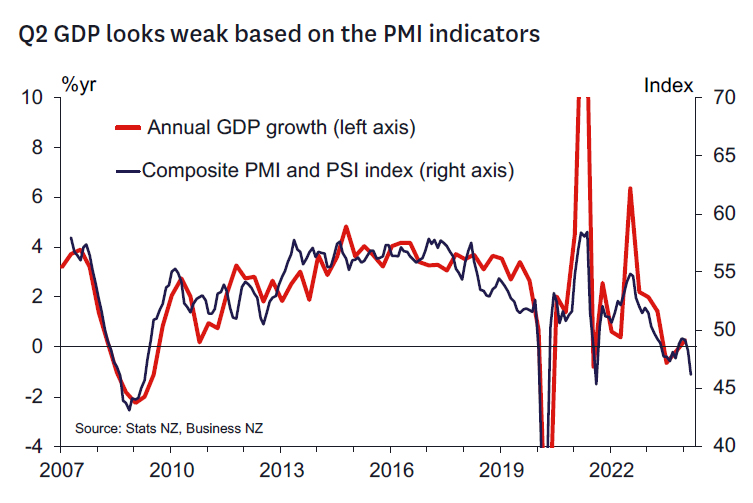

- Forward activity indicators (consumer and business confidence, PMIs) have remained weak in April, May and June and might suggest some downside risks to the RBNZ’s 0.1% GDP forecast for Q2 and 0.3-0.4% forecasts for Q3 and Q4 this year.

- The recently released NZIER QSBO confirmed that economic activity remains weak – particularly in the interest-sensitive construction sector. The outlook for investment looks weak. The labour market indicators confirm that the uptrend in the unemployment rate remains firmly in place and the RBNZ might be thinking they have some upside risks to their unemployment rate projections (which are 0.2% lower than Westpac’s by end 2024).

Inflation assessment.

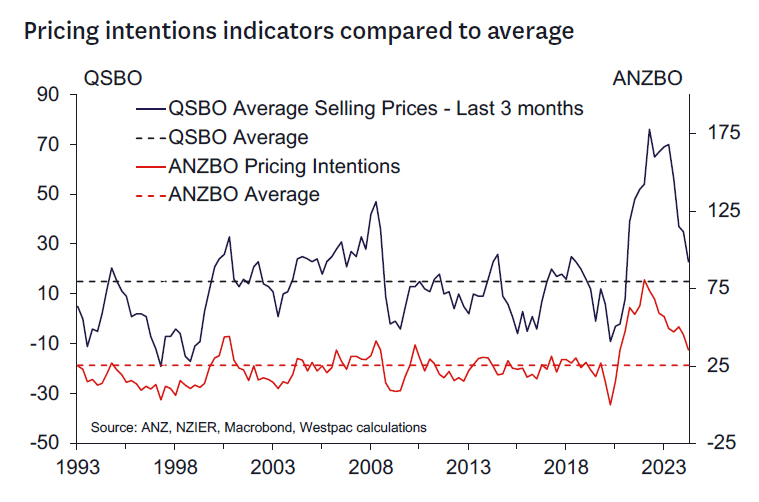

On the pricing side of the ledger, we don’t see very much to have moved the RBNZ’s short term inflation forecasts. The monthly Selected Price Indices suggest the Q2 CPI will be in line with the RBNZ and our forecast of 0.6%. House prices have been flat recently and might have some modest downside risks in the RBNZ’s forecasts given recent trends. Pricing indicators in recent business surveys and the QSBO suggest that inflation pressures are receding but remain somewhat elevated. Businesses still report that cost pressures are elevated. We don’t think on balance that there will have been much to change the RBNZ’s view that they need additional confidence that inflation is reverting sustainably within the 1-3% target range. The most recent pricing intentions data will have added to the RBNZ’s confidence, but future hard data in the form of the next couple of quarterly CPI prints will be most important in that regard.

Communication issues.

The RBNZ likely has no change in message to communicate. This is a similar situation to the April Review and resulted in a very short statement. We see something similar here. The objective would be to punt any reassessments of the outlook to the August Statement where full forecasts can be presented and key data (the Q2 CPI and labour market data especially) will be available.

The short statement will likely:

- Reiterate the core message that conditions need to be restrictive for a sustained period.

- Note that little has come to light to change their assessment of the near-term inflation outlook.

- Note that Budget 2024 was less contractionary than previously assumed with the ultimate impact on the economic outlook yet to be seen.

- Note that Q1 GDP printed in line with expectations but acknowledge recent indicators pointing to risks of a weaker economy and labour market further out.

We don’t think the markets will get a dovish tilt that supports recent market pricing (around a 50% chance of an easing in the October Review and around 35bps priced in by end 2024). If anything like that is coming, we will see it at the August Statement.

will be available.){kind=link}