Canada’s January inflation data will continue to be distorted by the temporary GST/HST tax holiday running from mid-December to mid-February. The drop in taxes lowered price growth by about 0.4% in December, slowing to 1.8% year-over-year in December from 1.9% in November. It would have ticked up to 2.2% without the temporary tax reduction.

We expect annual price growth (including the tax change) to edge down to 1.7% in January, with the slowing again entirely due to the change in taxes. The tax holiday will continue to muddy inflation readings until March when we can get a cleaner read of the consumer price index that are clear of distortions.

Still, the Bank of Canada will be focused on their preferred “core” CPI measures, which exclude the impact of indirect taxes, for clues on how underlying inflation trends are shaping up. Recent readings have surprised to the upside. In December, the CPI trim and median measures grew by an average 0.3% month-over-month—matching the rate in the previous two months, but with a monthly pace still above the 2% target on an annual basis.

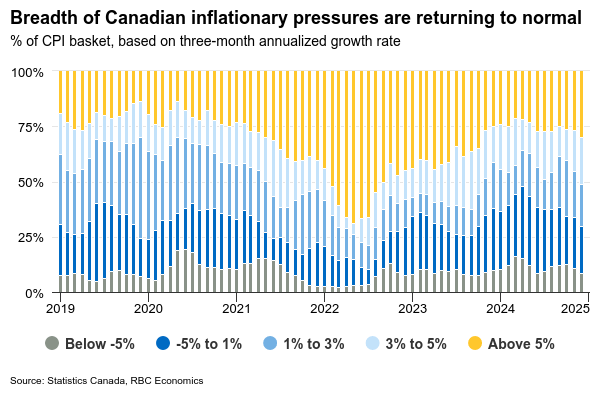

Annual rates for the median and trim measures are likely to move higher again in January, we expect to 2.6% from 2.5% in December. The better news is the scope of inflation pressures has not widened significantly. By our count, the share of consumer goods and services (outside of shelter) seeing elevated price growth at the end of 2024 was not meaningfully different from where it was at the start of the year.

Overall price growth continues to be disproportionately impacted by high growth in mortgage interest costs (accounting for 30% of annual CPI growth in December), which will continue to slow as the lagged impact of BoC interest rate cuts filters through to mortgage renewals. The core measures are, by design, less impacted by unusual movements in any one subcomponent, but still would have been running right around the BoC’s 2% inflation target if mortgage interest costs were not included in the calculations.

Moving forward, we continue to expect a soft domestic demand backdrop will allow for more unwinding in inflation this year. The labour markets have shown signs of stabilization, but lower job openings combined with a higher unemployment rate have started to push wage growth significantly lower. Trade uncertainties are clouding that outlook. But given announced targeted measures , we continue to look for an overall muted impact on growth and inflation, and expect past interest rate cuts will help with a turnaround in activity as soon as the second half of this year.

Week ahead data watch

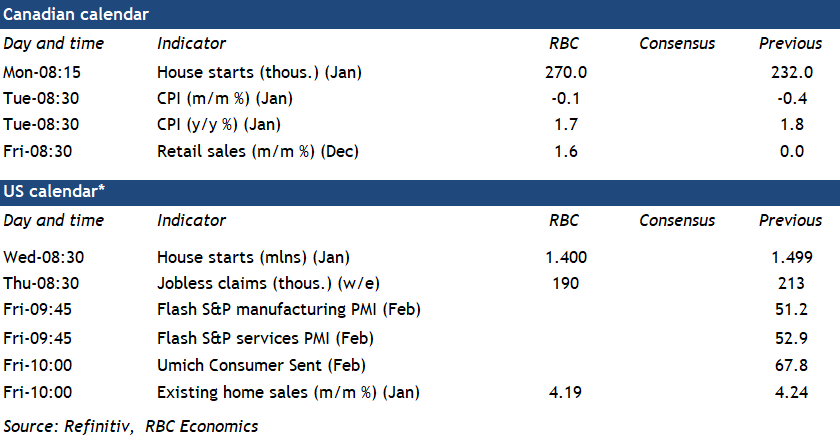

In line with StatCan’s prelim estimate, we expect Canadian retail sales rose by 1.6% in December as holiday spending got a boost from the Federal tax holiday. In January, there were signs that spending was pared back. Unit auto sales were also weaker in the same month – we expect the advance estimate will show slower spending at the start of 2025.

{kind=link}