Summary

- A moderation in economic activity since the FOMC last met in January is unlikely to shift the Committee out of wait-and-see mode at its upcoming meeting on March 19. We look for the Committee to maintain its target for the fed funds rate at its current range of 4.25%-4.50%.

- Concerns over the growth outlook have intensified in recent weeks amid the swirl of policy uncertainty related to U.S. trade and federal spending. Yet the labor market’s cooling has continued to be gradual on trend, while inflation remains frustratingly high. With Chair Powell reiterating ahead of the blackout period that the FOMC does “not need to be in a hurry” to adjust policy, we expect the FOMC will continue to await greater clarity on how policy changes affect its employment and inflation mandates.

- We expect the post-meeting statement to make a nod to the recent moderation in growth and labor market conditions, but to otherwise be little changed. The Committee likely will state that risks to its employment and inflation goals are “roughly in balance.” That said, we would not be surprised for Chair Powell to make a dovish comment or two at the press conference that reveal a slight easing bias by acknowledging that the downside risks to the labor market have increased somewhat.

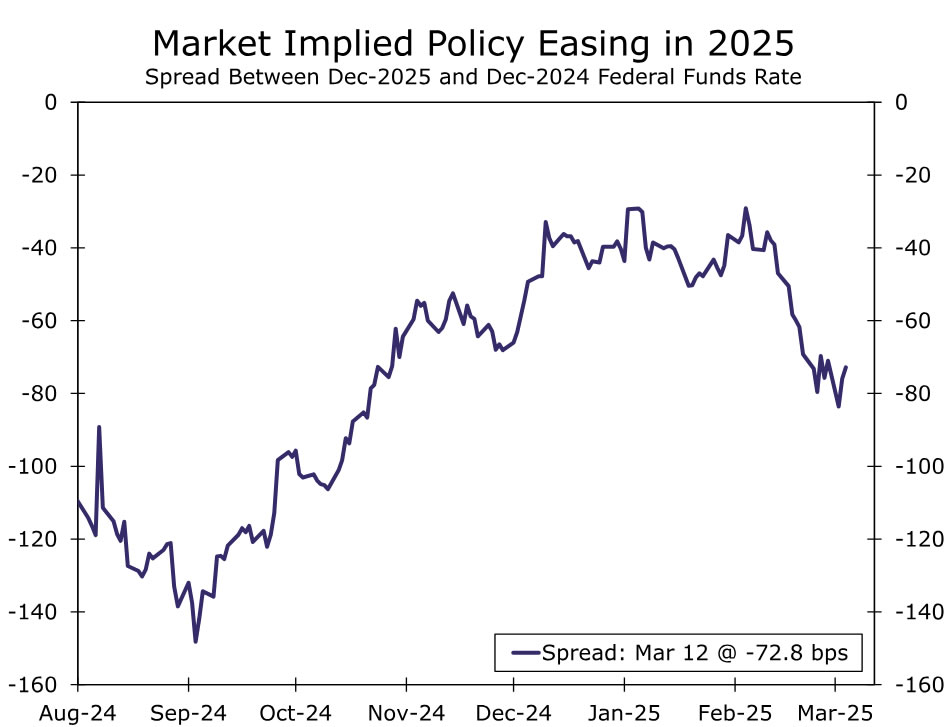

- The updated Summary of Economic Projections likely will show the median participant continues to expect 50 bps of easing this year. With markets currently pricing in 73 bps of cuts by the end of the year, a shift to one cut could further tighten financial conditions. Yet, as inflation remains roughly 50 bps above target and officials are cognizant of keeping inflation expectations anchored, three or more cuts might be too much for the Committee’s hawks. If the median dot for 2025 does change, we think it is more likely to signal 75 bps of easing rather than only 25 bps of rate cuts.

- Elsewhere in the SEP, we expect to see a modest downgrade to GDP growth for 2025, with the median estimate dipping a touch below 2.0%. At 4.3%, the median estimate for the unemployment rate at year-end still looks about right, although an increase to 4.4% would not surprise us. Estimates for inflation are likely to edge up further; we look for the median estimate for core PCE inflation at the end of the year to rise from 2.5% to 2.7%.

- The March meeting likely will include a discussion about whether a shift in balance sheet policy is warranted. This marks the next step toward an eventual end to runoff. We do not expect any changes to balance sheet runoff until the May 7 meeting when we expect the Committee to announce the end of quantitative tightening.

On Hold For Now

The economy entered 2025 with solid momentum, prompting the FOMC to leave the fed funds rate unchanged at its January 29 meeting after having cut its target range by 100 bps over the three previous meetings. While the Committee did not update its economic projections, there was little in the statement or press conference to indicate the FOMC was contemplating another rate cut in the near future. Indeed, Chair Powell noted multiple times in the press conference that the FOMC did not need to be in a “hurry” to adjust its policy stance. Rather, the Committee could afford to wait to see how potential policy changes under the new administration affected the Fed’s employment and inflation mandates.

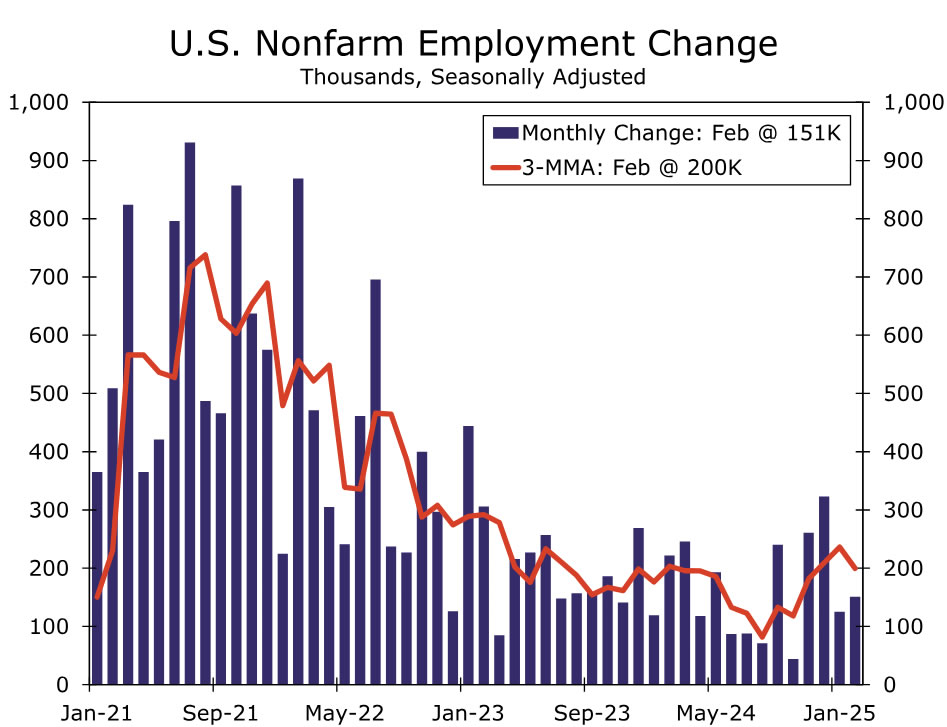

Since then, data have pointed to the economy losing a bit of steam. Monthly growth in nonfarm payrolls averaged 138K in the first two months of the year compared to 209K in the fourth quarter (Figure 1). Further signs of a cooler jobs market were evident in the headline unemployment rate and broader U-6 measure of under-employment moving up in February. Consumer spending also declined in January which, along with a widening trade balance, point to a slowing in Q1 GDP growth.

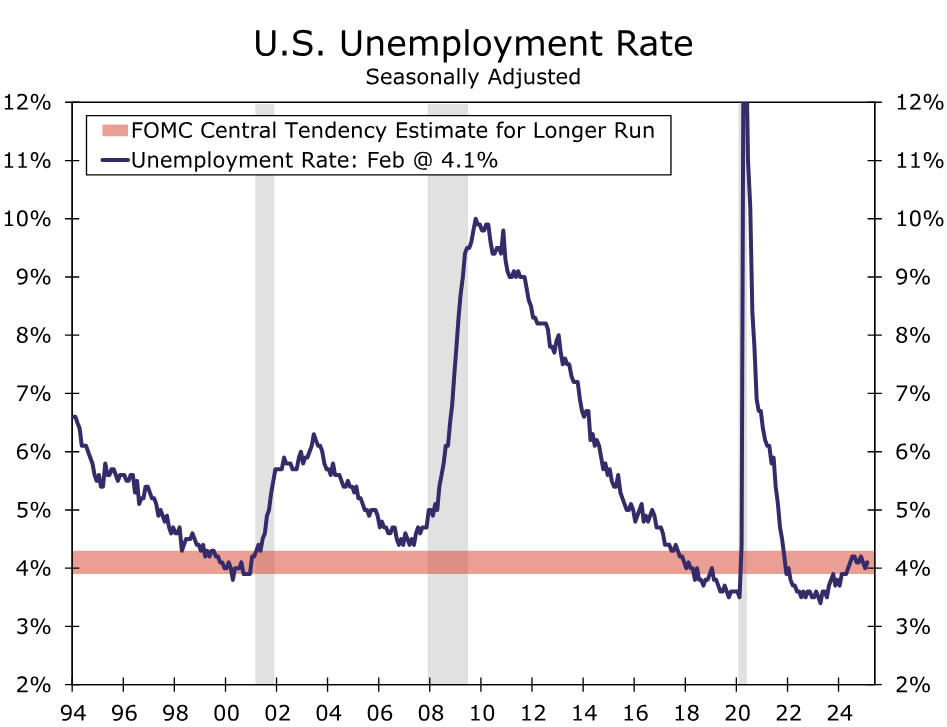

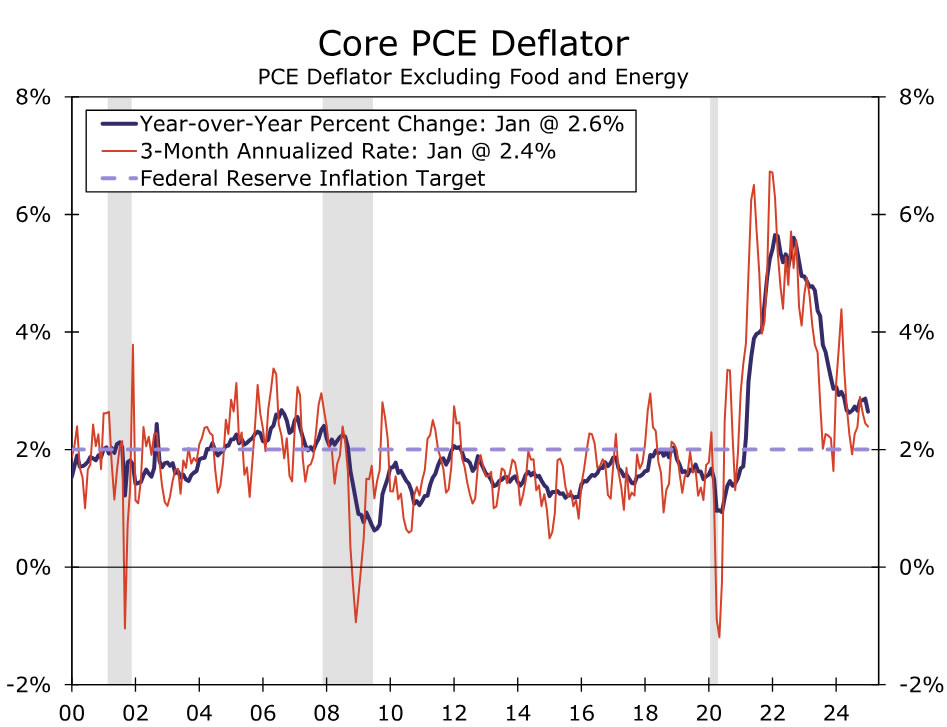

In our view, however, the recent moderation in activity is unlikely to shift the FOMC out of a wait-and-see mode at its upcoming meeting on March 19. The labor market’s cooling has continued to be gradual on trend, and the unemployment rate remains comfortably within the FOMC’s estimate of full employment (Figure 2). At the same time, inflation remains frustratingly high. Despite easing slightly in February, core CPI inflation is up 3.6% on both a three- and six-month annualized basis. Inflation as measured by the core PCE index looks somewhat closer to the Fed’s target, having slowed to a 2.4% annualized pace in the three months through January (Figure 3). Yet, that still leaves it running above the FOMC’s target, with the implementation of higher tariffs likely to stymie additional progress in lowering inflation in the months ahead. As a result, we expect the FOMC will keep the fed funds rate unchanged at 4.25%-4.50% at its March meeting. In Chair Powell’s last speaking engagement on March 7, he reiterated that the Committee does not need to be in a hurry to react to recent policy changes.

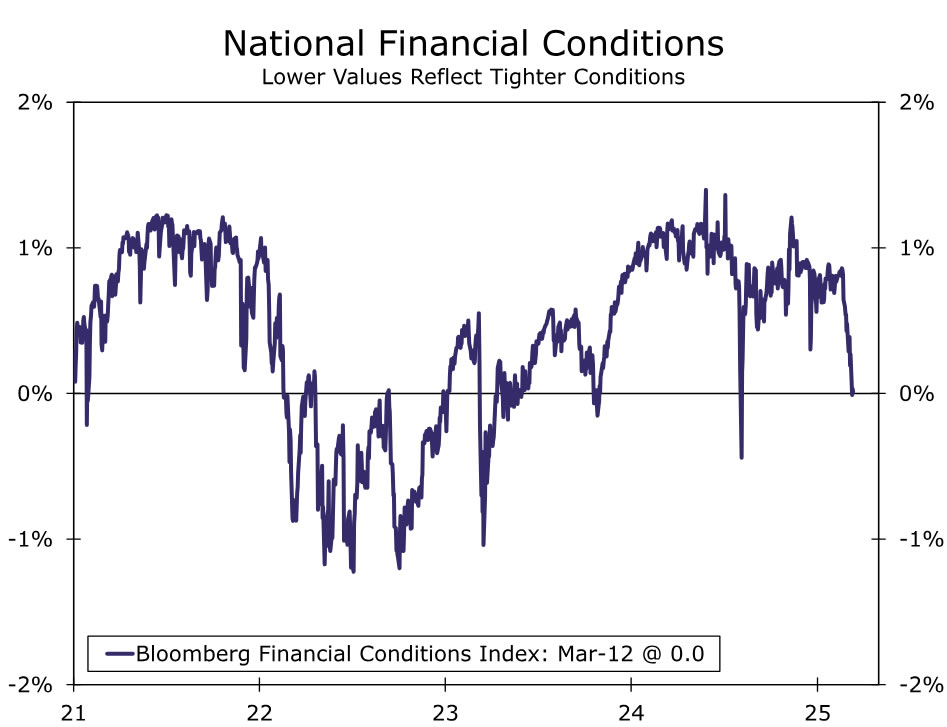

That said, concerns about an economic slowdown have extended beyond the mild softening in recent data as consumers, businesses and market participants grapple with policy uncertainty at levels unseen since the spring of 2020. Trade tensions have ratcheted higher, with an additional 20% tariff levied on Chinese imports and only a partial reprieve on 25% tariffs with Canada and Mexico. Efforts to curtail federal spending have also renewed concerns over the path of hiring ahead. As the growth-dampening effects of higher tariffs and fiscal tightening have come front-and-center, equity markets have neared correction territory and financial conditions have tightened (Figure 4).

We expect the post-meeting statement will nod to the recent moderation in growth and labor market conditions, but otherwise we expect the statement will be little changed. While risks to the employment side of the Fed’s mandate have edged up over the inter-meeting period, so too have the risks to inflation. We suspect the statement will thus continue to characterize the risks to the FOMC’s mandates as “roughly in balance”. That said, we would not be surprised if, when answering reporters’ questions in the post-meeting press conference, Chair Powell makes a dovish comment or two that acknowledge downside risks to the labor market and growth have increased in light of the recent policy environment.

SEP: Dots To Be Left Unchanged?

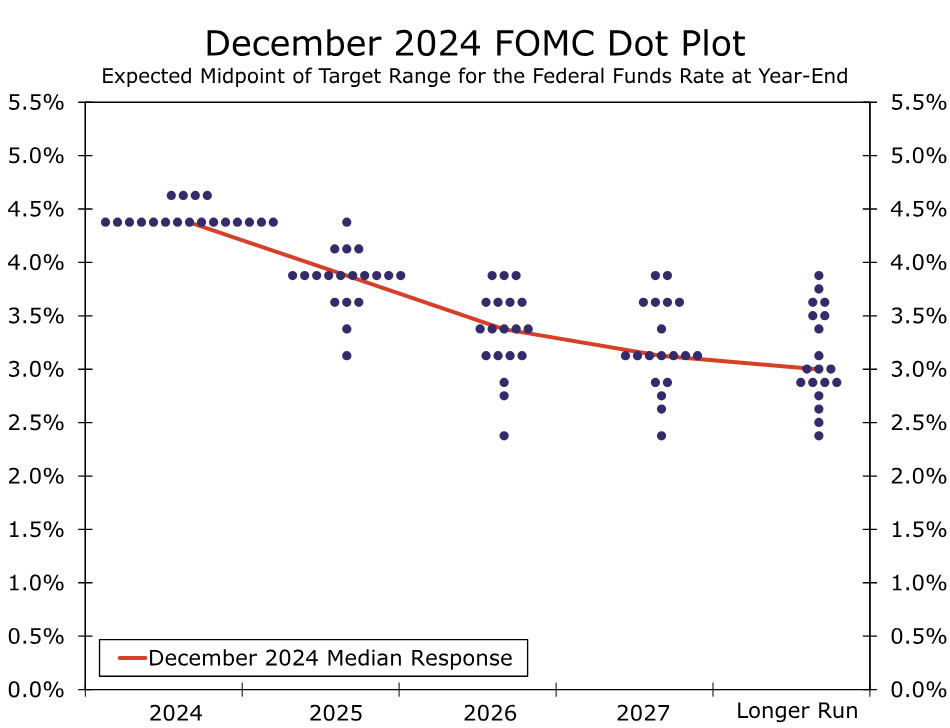

The uncertain and conflicting economic backdrop should make for an interesting Summary of Economic Projections (SEP). The Committee previously updated the SEP in December, and the median projection at that time looked for the fed funds rate to be reduced by 50 bps in 2025, 50 bps in 2026 and 25 bps in 2027 (Figure 5). Our expectation is that these projections will remain largely the same when updated next week. Given concerns about escalating trade tensions and the impact on economic growth, we doubt the Committee will want to send a hawkish message via a 2025 median dot that signals just one or zero cuts. Financial markets are priced for 73 bps of easing this year (Figure 6), so a signal from the FOMC that the base case forecast is one cut likely would lead to a tightening in financial conditions, an outcome we doubt the Committee is seeking.

Similarly, we believe the FOMC will be cautious about coming across as overly dovish. Inflation is still roughly 50 bps above the central bank’s target, and tariffs threaten to raise spot inflation and inflation expectations. While the FOMC generally seems inclined to “look through” a one-time increase in inflation from higher tariffs, various Committee members have expressed concerns about keeping inflation expectations anchored. A signal that three or more rate cuts are coming this year might worry the hawks who are concerned about the inflation outlook. Although individual dots may shift a little, we think that, on net, no change in the median dots is the most probable outcome. If the median dot for 2025 does change, we think it is more likely to signal 75 bps of easing than only 25 bps of rate cuts.

Elsewhere in the SEP, we expect to see a modest downgrade to economic projections for 2025. The median December projection looked for 2.1% real GDP growth in 2025. But, the initial tracking data suggest Q1 economic growth will be weak, while tariffs threaten the outlook for later in the year. We do not expect a major decline in the projections, but a dip below 2.0% seems to be in store. The previous projection for the unemployment rate was 4.3% each year from 2025-2027. This still looks about right for 2025, although it may rise by one-tenth of a percentage point to maintain consistency with the changes in real GDP growth.

We also expect the FOMC will revise upwardly its inflation projections. The current median projection for the core PCE deflator in 2025 is 2.5%. Changes to tariff rates since December probably argue for a slightly higher figure. Our own forecast for the core PCE deflator is 2.7%, and we expect the median Committee projection will be near this figure in next week’s SEP.

The End of QT Is Coming into View

The FOMC is getting closer to making a change to the Fed’s balance sheet runoff program, more commonly known as quantitative tightening (QT). QT has been ongoing since June 2022, when the Federal Reserve began reducing its holdings of Treasury securities and mortgage-backed securities (MBS) by up to $60 billion and $35 billion per month, respectively. These caps remained in place until June 2024, at which time the Committee reduced the monthly cap for Treasury securities to $25 billion in an effort to slow, but not stop, the pace of balance sheet runoff. Those monthly caps remain in place today.

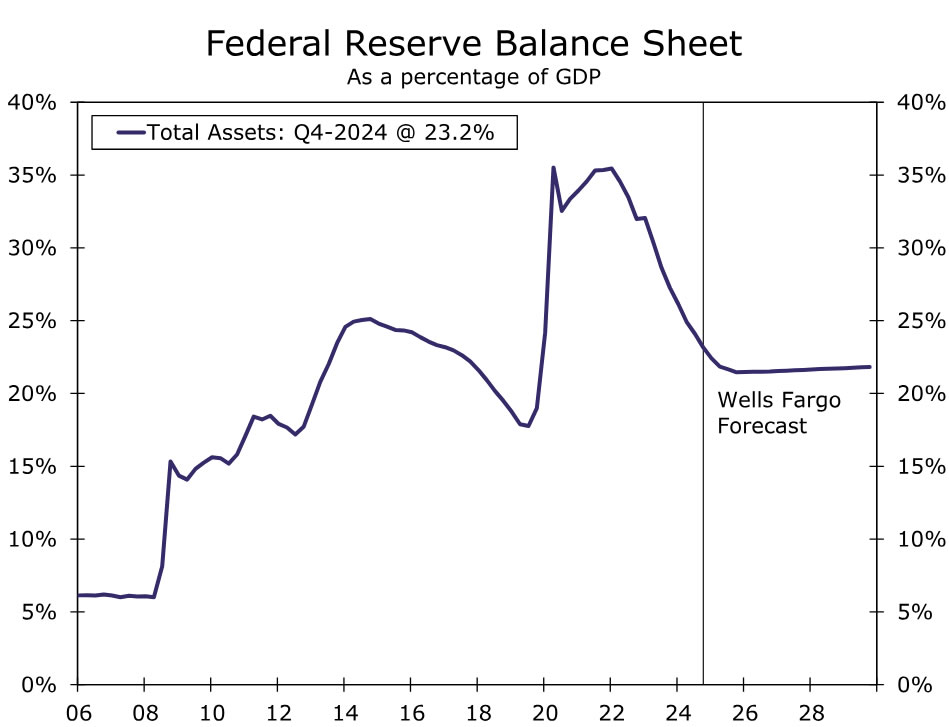

At present, the Federal Reserve’s security holdings total $6.4 trillion, a $2 trillion decline from the central bank’s peak holdings in 2022. The Federal Reserve’s balance sheet has fallen even more as a share of GDP, declining from 35% at the peak to 23% today (Figure 7). This passive balance sheet runoff has been a secondary form of monetary policy tightening and likely has contributed to some modest upward pressure on longer-term interest rates, perhaps on the order of 20-40 bps or so.

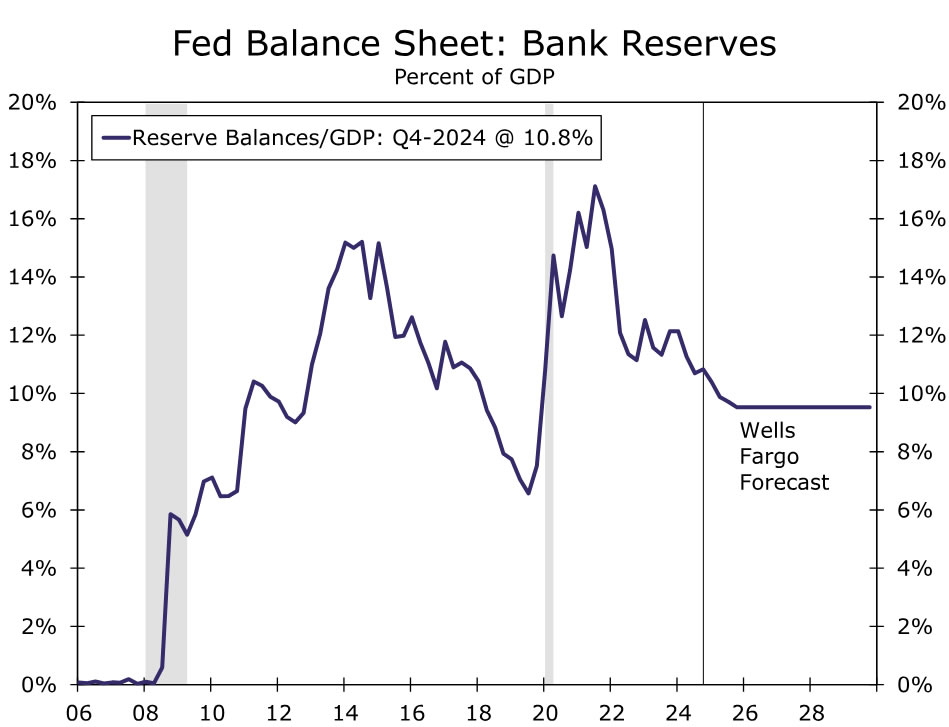

The upshot of the reduction in the Fed’s security holdings has been a reduction of the abundant liquidity in the financial system. Banks’ holdings of reserves at the Fed have declined considerably from their peak both in dollar terms and as a share of GDP (Figure 8). The Federal Reserve aims to maintain reserves that are “ample” enough such that the financial system operates smoothly but not so ample that the central bank’s balance sheet is larger than is necessary.

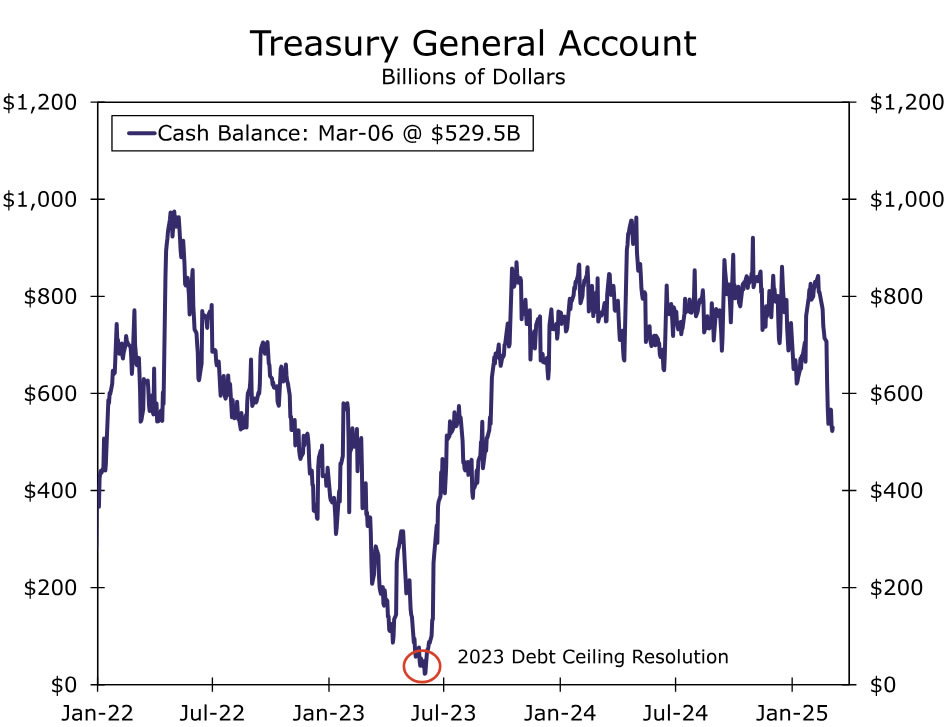

Identifying that Goldilocks zone of not-too-big and not-too-small is no easy task, and it has been made harder recently by the debt ceiling. The federal government’s borrowing capacity is currently constrained by the debt ceiling, which has been binding since it was reinstated at the start of the year. Because of the debt ceiling, the federal government has been financing itself less with new debt and more with its cash on hand (Figure 9). A reduction in the cash balance that the Treasury Department holds at the central bank (a liability on the Fed’s balance sheet) generally corresponds to an increase in bank reserves (another liability on the Fed’s balance sheet), all else equal.

Of course, once the debt ceiling is eventually lifted, the process will swing into reverse. The Treasury will issue new debt rapidly to rebuild the TGA, and this will reduce bank reserves sharply in a short period of time. These volatile swings in bank reserves make it even more difficult to get a read on how close the Federal Reserve is to the Goldilocks zone. The minutes from the January FOMC meeting signaled that “various participants” noted that it may be appropriate to consider pausing or slowing balance sheet runoff until the debt ceiling has been resolved.

Thus, we expect the March meeting to be a “live” meeting when it comes to the balance sheet, meaning we expect Committee members to actively debate whether a policy shift is warranted. Our expectation is that the Committee will maintain the current pace of QT for one more meeting and then announce the end of balance sheet runoff at the May 7 meeting. Starting June 1, we expect the Federal Reserve to keep its balance sheet flat through at least the end of the year.

Note that even if aggregate balance sheet runoff ceases, that does not mean that balance sheet policy has shifted to neutral. If the Fed’s balance sheet is held flat for an extended period of time, then it will still be shrinking as a share of GDP. Furthermore, the composition of the balance sheet can continue to evolve such that policy accommodation is still being removed. We look for MBS runoff to continue past June indefinitely as the Federal Reserve strives to reduce its mortgage holdings and slowly return to holding primarily Treasury securities. In order to keep the total balance sheet unchanged amid ongoing MBS runoff, we look for the Federal Reserve to start buying Treasury securities such that they replace MBS paydowns one-for-one. Returning to a primarily Treasury security portfolio would reduce the support that the central bank lends to the mortgage market.

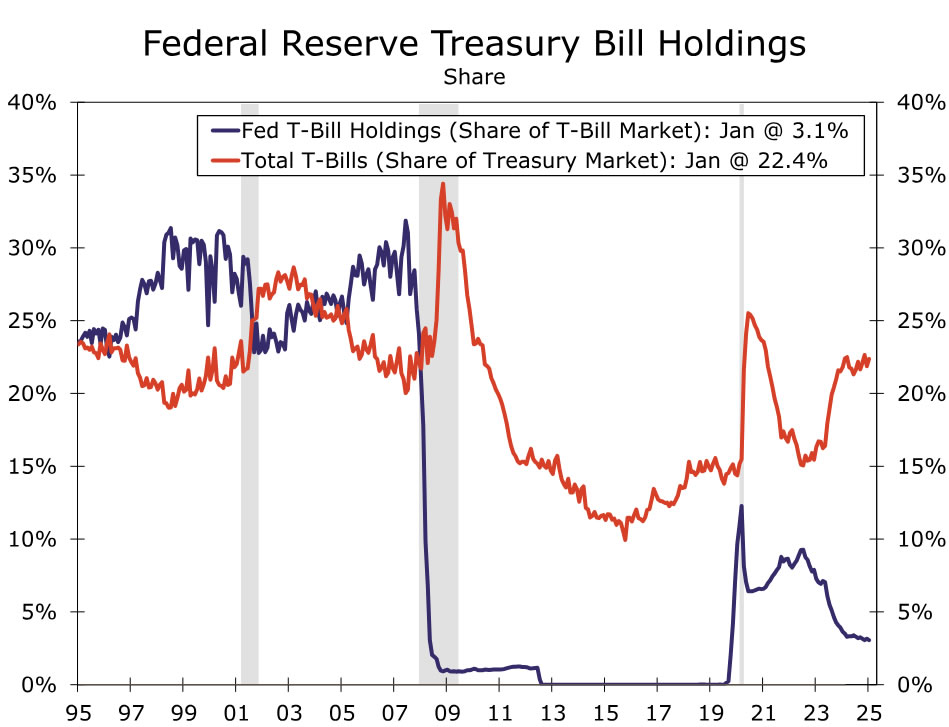

Another factor to consider is the weighted-average maturity of the central bank’s Treasury security holdings. At present, the Federal Reserve’s security holdings generally skew longer-dated than the overall market. For example, the Federal Reserve currently holds just 3% of T-bills outstanding despite T-bills accounting for roughly 22% of the overall Treasury market (Figure 10). Slowly replacing MBS with shorter-dated Treasury securities, such as Treasury bills, would re-weight the Fed’s balance sheet away from longer-dated securities and toward shorter-dated securities, putting some very modest upward pressure on longer-term yields, all else equal. Over time, if the Federal Reserve’s Treasury security portfolio broadly reflects the overall market, the central bank’s balance sheet should exert a more market neutral impact on yields. The end of QT may be coming soon, but the balance sheet’s role as the secondary policy tool will continue for the foreseeable future.

{kind=link}